A chart shows that the Baltic Dry Index is under pressure and declining, with Capesize and Panamax shipping sectors remaining weak.

2026-06-03 23:09:21

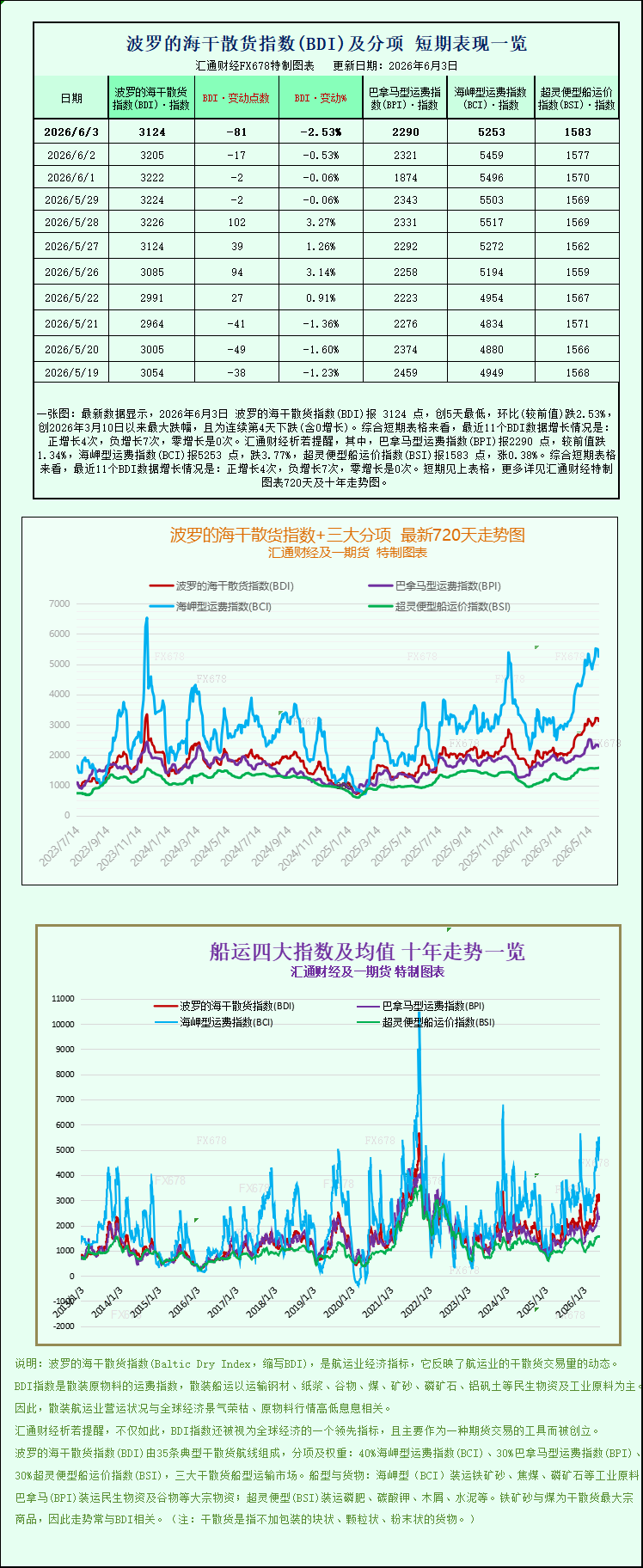

Latest data shows that the Baltic Dry Index (BDI) closed at 3124 points on June 3, 2026, a five-day low, down 2.53% from the previous day, marking the largest drop since March 10, 2026, and the fourth consecutive day of decline (including zero growth). Looking at the short-term charts, the recent 11 BDI data points show: 4 positive increases, 7 negative increases, and 0 zero increases. Specifically, the Panamax Freight Index (BPI) closed at 2290 points, down 1.34% from the previous day; the Capesize Freight Index (BCI) closed at 5253 points, down 3.77%; and the Supramax Freight Index (BSI) closed at 1583 points, up 0.38%. For detailed 720-day and 10-year trend charts of the Baltic Dry Index and its three main sub-indices, please refer to the specially designed charts.

The international dry bulk shipping market weakened overall on Wednesday, with the Baltic Dry Index (BDI) falling sharply, putting pressure on prices for most major vessel types. The decline was primarily driven by lower freight rates for both Capesize and Panamax bulk carriers. Weak demand and declining rates for these two main vessel types directly dragged down the overall dry bulk shipping market performance. Only the smaller bulk carrier segment saw a slight increase against the trend, highlighting a significant market divergence.

Data shows that the Baltic Dry Index, which tracks freight rates for the three major dry bulk carriers—Capesize, Panamax, and Supramax—fell sharply by 81 points, or 2.5%, to 3124 points, ending its short-term fluctuations and returning to a downward trend. This reflects a cooling of activity in the overall dry bulk shipping market and a contraction in freight profit margins.

As a core component of the large dry bulk carrier market, the Capesize vessel market saw the most significant decline. The Baltic Capesize Index plummeted 206 points in a single day, a drop of 3.8%, closing at 5253 points, becoming the primary factor dragging down the overall market. It is understood that this vessel type mainly carries 150,000 tons of bulk industrial raw materials, with core cargoes including iron ore, thermal coal, and other essential industrial commodities. Corresponding profit data shows that the average daily operating revenue of Capesize vessels decreased by $1870 compared to the previous period, with the latest average daily revenue falling to $44138, indicating a significant reduction in the profitability of large dry bulk carrier transportation.

Industry analysts indicate that the weakening of the Capesize vessel market is primarily driven by the sluggish performance of the upstream commodity market. On Wednesday, international iron ore prices declined in tandem, influenced by the continued narrowing profits in the downstream steel industry. Steel companies' willingness to purchase raw materials was weak, coupled with China, the world's largest iron ore consumer, entering its traditional off-season, resulting in weak restocking demand from end-users. This led to a significant reduction in upstream raw material transportation orders, directly putting downward pressure on freight rates for large ore carriers. This supply-demand imbalance dragged down the sector's overall performance.

The medium-sized vessel market also failed to maintain its recovery momentum, with the Panamax sector weakening in tandem. The Baltic Panamax Index fell 31 points to close at 2290, indicating a continued slump in the sector. This vessel type primarily transports 60,000 to 70,000 tons of commodities such as coal and grain, and is a mainstay of global energy and food maritime trade. Profitability data shows that Panamax vessels' average daily revenue decreased by $282, with the latest average daily revenue at $20,607. Profit margins for medium-sized bulk carriers continue to narrow, and demand for energy and food maritime transport has not yet provided effective support.

The overall market exhibited a clear divergence, with the small bulk carrier sector bucking the trend and showing a slight rebound amid widespread declines in major vessel types. The Supramax index rose slightly by 6 points, holding steady above 1583 points, becoming the only sub-sector of bulk carriers to close higher that day. Compared to large and medium-sized vessels, Supramax vessels offer more flexible routes and are better suited for small- to medium-volume freight orders. They are less affected by weak demand for bulk industrial raw materials, thus demonstrating greater resilience and partially offsetting the downward pressure on the broader market, but failing to reverse the overall market's weak trend.

Market analysts point out that the dry bulk shipping market will continue to face demand-side pressure in the short term, with the off-season effect on industrial raw material shipping demand persisting. Freight rates for major vessel types may continue to fluctuate and trend weakly. Going forward, it is necessary to focus on the progress of the resumption of work and production in the downstream steel industry, the pace of bulk commodity restocking, and changes in global grain shipping orders to determine the subsequent recovery momentum of the shipping market.

The international dry bulk shipping market weakened overall on Wednesday, with the Baltic Dry Index (BDI) falling sharply, putting pressure on prices for most major vessel types. The decline was primarily driven by lower freight rates for both Capesize and Panamax bulk carriers. Weak demand and declining rates for these two main vessel types directly dragged down the overall dry bulk shipping market performance. Only the smaller bulk carrier segment saw a slight increase against the trend, highlighting a significant market divergence.

Data shows that the Baltic Dry Index, which tracks freight rates for the three major dry bulk carriers—Capesize, Panamax, and Supramax—fell sharply by 81 points, or 2.5%, to 3124 points, ending its short-term fluctuations and returning to a downward trend. This reflects a cooling of activity in the overall dry bulk shipping market and a contraction in freight profit margins.

As a core component of the large dry bulk carrier market, the Capesize vessel market saw the most significant decline. The Baltic Capesize Index plummeted 206 points in a single day, a drop of 3.8%, closing at 5253 points, becoming the primary factor dragging down the overall market. It is understood that this vessel type mainly carries 150,000 tons of bulk industrial raw materials, with core cargoes including iron ore, thermal coal, and other essential industrial commodities. Corresponding profit data shows that the average daily operating revenue of Capesize vessels decreased by $1870 compared to the previous period, with the latest average daily revenue falling to $44138, indicating a significant reduction in the profitability of large dry bulk carrier transportation.

Industry analysts indicate that the weakening of the Capesize vessel market is primarily driven by the sluggish performance of the upstream commodity market. On Wednesday, international iron ore prices declined in tandem, influenced by the continued narrowing profits in the downstream steel industry. Steel companies' willingness to purchase raw materials was weak, coupled with China, the world's largest iron ore consumer, entering its traditional off-season, resulting in weak restocking demand from end-users. This led to a significant reduction in upstream raw material transportation orders, directly putting downward pressure on freight rates for large ore carriers. This supply-demand imbalance dragged down the sector's overall performance.

The medium-sized vessel market also failed to maintain its recovery momentum, with the Panamax sector weakening in tandem. The Baltic Panamax Index fell 31 points to close at 2290, indicating a continued slump in the sector. This vessel type primarily transports 60,000 to 70,000 tons of commodities such as coal and grain, and is a mainstay of global energy and food maritime trade. Profitability data shows that Panamax vessels' average daily revenue decreased by $282, with the latest average daily revenue at $20,607. Profit margins for medium-sized bulk carriers continue to narrow, and demand for energy and food maritime transport has not yet provided effective support.

The overall market exhibited a clear divergence, with the small bulk carrier sector bucking the trend and showing a slight rebound amid widespread declines in major vessel types. The Supramax index rose slightly by 6 points, holding steady above 1583 points, becoming the only sub-sector of bulk carriers to close higher that day. Compared to large and medium-sized vessels, Supramax vessels offer more flexible routes and are better suited for small- to medium-volume freight orders. They are less affected by weak demand for bulk industrial raw materials, thus demonstrating greater resilience and partially offsetting the downward pressure on the broader market, but failing to reverse the overall market's weak trend.

Market analysts point out that the dry bulk shipping market will continue to face demand-side pressure in the short term, with the off-season effect on industrial raw material shipping demand persisting. Freight rates for major vessel types may continue to fluctuate and trend weakly. Going forward, it is necessary to focus on the progress of the resumption of work and production in the downstream steel industry, the pace of bulk commodity restocking, and changes in global grain shipping orders to determine the subsequent recovery momentum of the shipping market.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.