A chart shows that the Baltic Dry Index has fallen, with both Capesize and Panamax bulk carrier prices declining.

2026-06-05 01:18:08

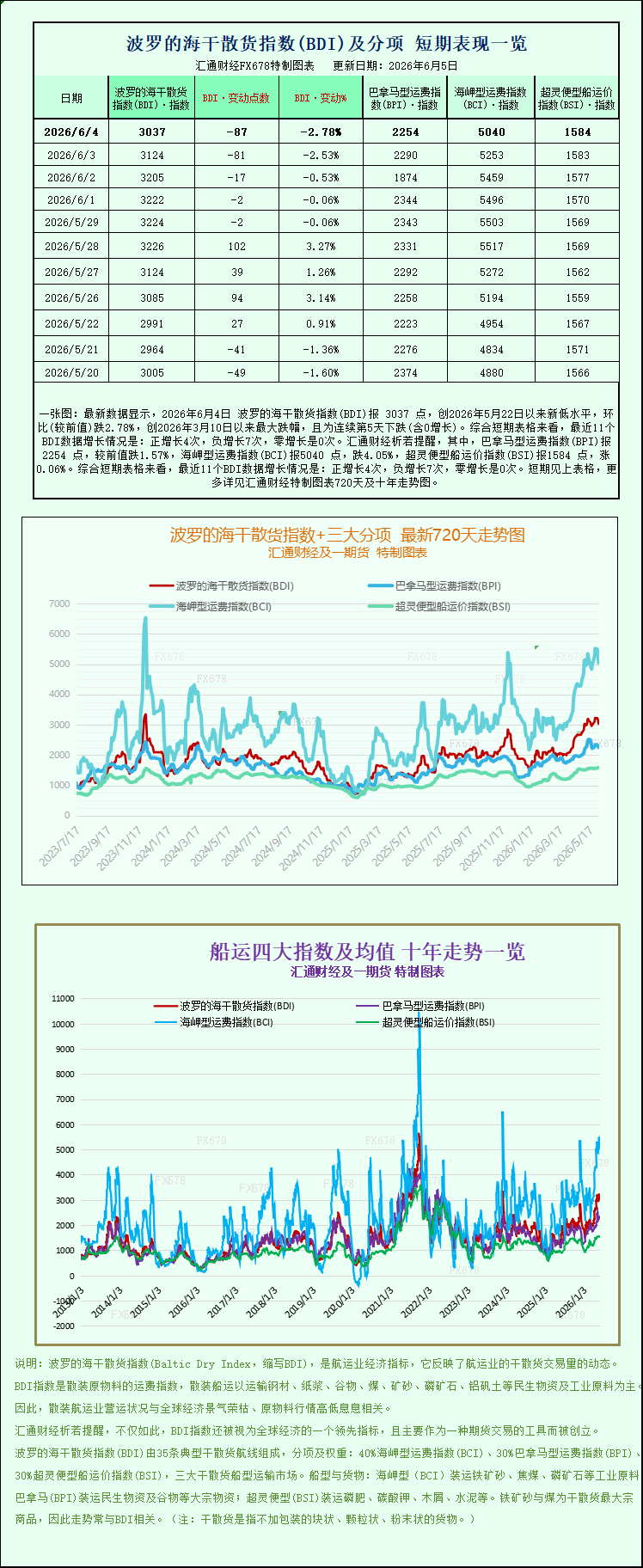

Latest data shows that the Baltic Dry Index (BDI) closed at 3037 points on June 4, 2026, a new low since May 22, 2026, down 2.78% month-on-month, the largest drop since March 10, 2026, and marking the fifth consecutive day of decline (including zero growth). Looking at the short-term charts, the BDI has seen positive growth 4 times, negative growth 7 times, and zero growth in the last 11 BDI data points. Specifically, the Panamax Freight Index (BPI) closed at 2254 points, down 1.57% from the previous value; the Capesize Freight Index (BCI) closed at 5040 points, down 4.05%; and the Supramax Freight Index (BSI) closed at 1584 points, up 0.06%. For detailed 720-day and 10-year trend charts of the Baltic Dry Index and its three main sub-indices, please refer to the specially designed charts.

On June 4, the international dry bulk shipping market was under pressure and weakened overall. The Baltic Dry Index closed lower on Thursday, with freight rates for the two main vessel types, Capesize and Panamax, falling in tandem. Only Handysize vessel freight rates saw a slight increase, indicating a significant divergence in market performance.

Data released by the Baltic Exchange shows that the Baltic Dry Index, which reflects the freight rates of the three major dry bulk carriers—Capesize, Panamax, and Supramax—fell sharply by 87 basis points in a single day, with an overall decline of 2.8%, closing at 3037 points. The downward pressure on the index was mainly driven by the collective decline in freight rates for large ocean-going bulk carriers.

The Capesize freight rate index, a bellwether for the dry bulk market, saw the most significant decline, plunging 213 points in a single day, a drop of 4.1%, closing at 5040 points. The average daily earnings on the main routes for this vessel type also shrank. Capesize standard vessels with a deadweight tonnage of approximately 150,000 tons, primarily engaged in the ocean transport of bulk raw materials such as iron ore and thermal coal, experienced a sharp decrease of $1934 in average daily earnings, ultimately falling to $42,204 per day. Industry analysts point out that this round of Capesize freight rate plunges is deeply linked to upstream iron ore spot market conditions. On Thursday, international iron ore spot prices experienced their largest single-day drop in nearly two months. The market generally held pessimistic expectations for end-user demand in China, the world's largest iron ore consumer. Domestic steel mills' smelting profits continued to narrow, coupled with persistently high upstream ore procurement costs, forcing steel mills to proactively reduce raw material stockpiles and decrease their ocean-going iron ore purchases, directly weakening the cargo support for ocean-going Capesize vessels.

In the medium-sized fleet, Panamax bulk carriers also suffered from a downward trend, with the Panamax Freight Index falling 36 points to close at 2254. Standard Panamax vessels, primarily handling 60,000 to 70,000 tonnes of coal and grain transported transoceanically, saw their average daily operating revenue decline by $322 to $20,285. Weak demand for coal shipments and a slowdown in global grain shipments are the core factors suppressing Panamax freight rates.

The small vessel sector showed independent performance, contrasting with the overall decline in large vessels. The Supramax bulk carrier freight rate index bucked the trend, rising slightly by 1 point to close firmly at 1584 points. Small and medium-sized vessels achieved a slight stabilization in freight rates by relying on regional short-haul cargo and small-batch general cargo turnover demand, becoming one of the few sectors in the dry bulk market to rise that day.

Overall, the current dry bulk shipping market presents a structural pattern of "weak large vessels and resilient small vessels." Changes in China's end-user demand for bulk commodities have become a key variable influencing the freight rate trend of large ocean-going bulk carriers. Subsequent supply and demand changes in iron ore, coal, and grain will continue to affect the freight rate trend of various vessel types.

On June 4, the international dry bulk shipping market was under pressure and weakened overall. The Baltic Dry Index closed lower on Thursday, with freight rates for the two main vessel types, Capesize and Panamax, falling in tandem. Only Handysize vessel freight rates saw a slight increase, indicating a significant divergence in market performance.

Data released by the Baltic Exchange shows that the Baltic Dry Index, which reflects the freight rates of the three major dry bulk carriers—Capesize, Panamax, and Supramax—fell sharply by 87 basis points in a single day, with an overall decline of 2.8%, closing at 3037 points. The downward pressure on the index was mainly driven by the collective decline in freight rates for large ocean-going bulk carriers.

The Capesize freight rate index, a bellwether for the dry bulk market, saw the most significant decline, plunging 213 points in a single day, a drop of 4.1%, closing at 5040 points. The average daily earnings on the main routes for this vessel type also shrank. Capesize standard vessels with a deadweight tonnage of approximately 150,000 tons, primarily engaged in the ocean transport of bulk raw materials such as iron ore and thermal coal, experienced a sharp decrease of $1934 in average daily earnings, ultimately falling to $42,204 per day. Industry analysts point out that this round of Capesize freight rate plunges is deeply linked to upstream iron ore spot market conditions. On Thursday, international iron ore spot prices experienced their largest single-day drop in nearly two months. The market generally held pessimistic expectations for end-user demand in China, the world's largest iron ore consumer. Domestic steel mills' smelting profits continued to narrow, coupled with persistently high upstream ore procurement costs, forcing steel mills to proactively reduce raw material stockpiles and decrease their ocean-going iron ore purchases, directly weakening the cargo support for ocean-going Capesize vessels.

In the medium-sized fleet, Panamax bulk carriers also suffered from a downward trend, with the Panamax Freight Index falling 36 points to close at 2254. Standard Panamax vessels, primarily handling 60,000 to 70,000 tonnes of coal and grain transported transoceanically, saw their average daily operating revenue decline by $322 to $20,285. Weak demand for coal shipments and a slowdown in global grain shipments are the core factors suppressing Panamax freight rates.

The small vessel sector showed independent performance, contrasting with the overall decline in large vessels. The Supramax bulk carrier freight rate index bucked the trend, rising slightly by 1 point to close firmly at 1584 points. Small and medium-sized vessels achieved a slight stabilization in freight rates by relying on regional short-haul cargo and small-batch general cargo turnover demand, becoming one of the few sectors in the dry bulk market to rise that day.

Overall, the current dry bulk shipping market presents a structural pattern of "weak large vessels and resilient small vessels." Changes in China's end-user demand for bulk commodities have become a key variable influencing the freight rate trend of large ocean-going bulk carriers. Subsequent supply and demand changes in iron ore, coal, and grain will continue to affect the freight rate trend of various vessel types.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.