A chart: The Baltic Dry Index softens due to lower Capesize freight rates.

2026-06-15 23:09:08

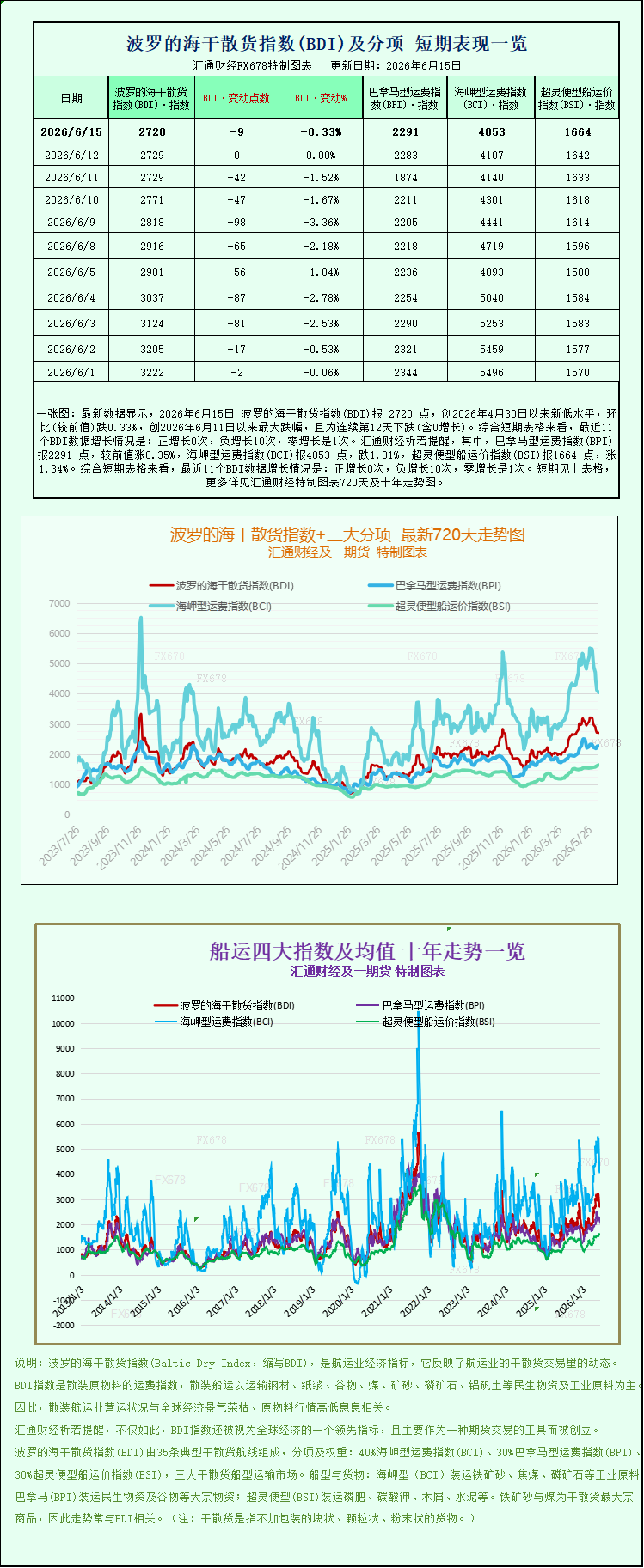

Latest data shows that on June 15, 2026, the Baltic Dry Index (BDI) stood at 2720 points, a new low since April 30, 2026, down 0.33% month-on-month, marking the largest drop since June 11, 2026, and the 12th consecutive day of decline (including zero growth). Looking at the short-term charts, the recent 11 BDI data points show: 0 positive growths, 10 negative growths, and 1 zero growth. Specifically, the Panamax Freight Index (BPI) was at 2291 points, up 0.35% from the previous value; the Capesize Freight Index (BCI) was at 4053 points, down 1.31%; and the Supramax Freight Index (BSI) was at 1664 points, up 1.34%. For detailed 720-day and 10-year trend charts of the Baltic Dry Index and its three main sub-indices, please refer to the specially designed charts.

The Baltic Dry Index (BDI), a key indicator of the international shipping market, saw a slight decline on Monday, with overall market sentiment weakening. This drop was primarily driven by a significant correction in Capesize (Good Hope) freight rates, which offset the gains in freight rates for smaller vessels, halting the overall upward trend in the dry bulk market. As a core benchmark for global dry bulk shipping trade, the BDI tracks freight rates for ocean-going vessels carrying bulk commodities such as iron ore, coal, and grain, directly reflecting changes in global commodity shipping demand and the supply-demand dynamics of the shipping market.

Data shows that the Baltic Dry Index (BDI), which tracks freight rates for the three major bulk carrier types—Capesize, Panamax, and Supramax—fell by 9 points, or 0.3%, to close at 2720 points, ending its previous period of steady upward movement. Among these, Capesize vessels, the largest in size and primarily carrying industrial raw materials, became the main drag on the market. The Capesize-specific index fell sharply by 54 points, or 1.32%, to close at 4053 points, making it the category with the most significant decline among all vessel types that day.

In terms of specific profitability data, Capesize bulk carriers, primarily operating at 150,000-ton ultra-large deadweights and mainly transporting industrial bulk raw materials such as iron ore and thermal coal, saw their average daily earnings on core routes decrease by $495 compared to the previous day, with the latest average daily revenue falling back to $33,253. The weakening demand for large industrial raw material shipping in the short term directly dragged down the overall profitability of the Capesize market. However, there are potential positive factors supporting the market fundamentals. Workers at BHP's Port Hedland in Western Australia are planning a strike this week, with the core demands being higher wages and improved working conditions. This event is likely to disrupt the pace of Australian iron ore exports, leading to a short-term tightening of Australian iron ore shipping supply, potentially paving the way for a subsequent stabilization and recovery in large bulk carrier freight rates.

In stark contrast to the sluggish performance of Capesize vessels, the medium-sized Panamax bulk carrier market maintained a steady upward trend. The Panamax index rose 8 points, or 0.4%, to close at 2291 points. Correspondingly, the average daily earnings for Panamax vessels increased by $72, reaching a new average of $20,617 per day. This vessel type, with a deadweight tonnage concentrated between 60,000 and 70,000 tons, is primarily suited for the transoceanic transport of global coal, grains, soybeans, and other food and energy commodities. The recent steady release of global demand for food trade transportation has supported the counter-trend rise in medium-sized bulk carrier freight rates.

Regarding the situation in the Middle East shipping market, Maria Bertzeletou, Senior Market Analyst at Signal Group, provided her latest market forecast. She stated that, based on current market expectations, the relevant shipping agreements will be formally signed this Friday, at which point the congestion and navigation restrictions in the Strait of Hormuz will gradually ease. However, the recovery of the shipping market will be a gradual process; ship traffic, route scheduling, and cargo transportation will not immediately return to full normalcy, and market capacity supply and freight rates will steadily return to normal.

Previously, the Strait of Hormuz, a key global energy transport route, was disrupted due to geopolitical conflicts and localized wars in the Middle East. As the world's most important chokepoint for oil and energy transportation, the temporary restriction on this waterway directly led to a shortage of shipping capacity in the global shipping market, driving up international shipping freight rates and providing significant support for the transportation costs of global energy and commodity trade. As the situation gradually eased and market tensions cooled, the upward momentum of shipping rates weakened accordingly.

The small bulk carrier market also continued its recovery trend, with the Supramax index recording a significant increase of 22 points, or 1.3%, to 1664 points. Smaller vessels, with their advantages of flexible routes and suitability for transporting small to medium-sized cargoes, have performed strongly, supported by global regional demand for short- and medium-haul general cargo and grain shipping. This performance contrasts with the sluggish performance of larger Capesize vessels, resulting in a clear structural trend in the overall dry bulk shipping market.

The Baltic Dry Index (BDI), a key indicator of the international shipping market, saw a slight decline on Monday, with overall market sentiment weakening. This drop was primarily driven by a significant correction in Capesize (Good Hope) freight rates, which offset the gains in freight rates for smaller vessels, halting the overall upward trend in the dry bulk market. As a core benchmark for global dry bulk shipping trade, the BDI tracks freight rates for ocean-going vessels carrying bulk commodities such as iron ore, coal, and grain, directly reflecting changes in global commodity shipping demand and the supply-demand dynamics of the shipping market.

Data shows that the Baltic Dry Index (BDI), which tracks freight rates for the three major bulk carrier types—Capesize, Panamax, and Supramax—fell by 9 points, or 0.3%, to close at 2720 points, ending its previous period of steady upward movement. Among these, Capesize vessels, the largest in size and primarily carrying industrial raw materials, became the main drag on the market. The Capesize-specific index fell sharply by 54 points, or 1.32%, to close at 4053 points, making it the category with the most significant decline among all vessel types that day.

In terms of specific profitability data, Capesize bulk carriers, primarily operating at 150,000-ton ultra-large deadweights and mainly transporting industrial bulk raw materials such as iron ore and thermal coal, saw their average daily earnings on core routes decrease by $495 compared to the previous day, with the latest average daily revenue falling back to $33,253. The weakening demand for large industrial raw material shipping in the short term directly dragged down the overall profitability of the Capesize market. However, there are potential positive factors supporting the market fundamentals. Workers at BHP's Port Hedland in Western Australia are planning a strike this week, with the core demands being higher wages and improved working conditions. This event is likely to disrupt the pace of Australian iron ore exports, leading to a short-term tightening of Australian iron ore shipping supply, potentially paving the way for a subsequent stabilization and recovery in large bulk carrier freight rates.

In stark contrast to the sluggish performance of Capesize vessels, the medium-sized Panamax bulk carrier market maintained a steady upward trend. The Panamax index rose 8 points, or 0.4%, to close at 2291 points. Correspondingly, the average daily earnings for Panamax vessels increased by $72, reaching a new average of $20,617 per day. This vessel type, with a deadweight tonnage concentrated between 60,000 and 70,000 tons, is primarily suited for the transoceanic transport of global coal, grains, soybeans, and other food and energy commodities. The recent steady release of global demand for food trade transportation has supported the counter-trend rise in medium-sized bulk carrier freight rates.

Regarding the situation in the Middle East shipping market, Maria Bertzeletou, Senior Market Analyst at Signal Group, provided her latest market forecast. She stated that, based on current market expectations, the relevant shipping agreements will be formally signed this Friday, at which point the congestion and navigation restrictions in the Strait of Hormuz will gradually ease. However, the recovery of the shipping market will be a gradual process; ship traffic, route scheduling, and cargo transportation will not immediately return to full normalcy, and market capacity supply and freight rates will steadily return to normal.

Previously, the Strait of Hormuz, a key global energy transport route, was disrupted due to geopolitical conflicts and localized wars in the Middle East. As the world's most important chokepoint for oil and energy transportation, the temporary restriction on this waterway directly led to a shortage of shipping capacity in the global shipping market, driving up international shipping freight rates and providing significant support for the transportation costs of global energy and commodity trade. As the situation gradually eased and market tensions cooled, the upward momentum of shipping rates weakened accordingly.

The small bulk carrier market also continued its recovery trend, with the Supramax index recording a significant increase of 22 points, or 1.3%, to 1664 points. Smaller vessels, with their advantages of flexible routes and suitability for transporting small to medium-sized cargoes, have performed strongly, supported by global regional demand for short- and medium-haul general cargo and grain shipping. This performance contrasts with the sluggish performance of larger Capesize vessels, resulting in a clear structural trend in the overall dry bulk shipping market.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.