A chart shows that the Baltic Dry Index has bottomed out and risen slightly, with a rebound in Capesize freight rates driving a market recovery.

2026-06-19 01:44:53

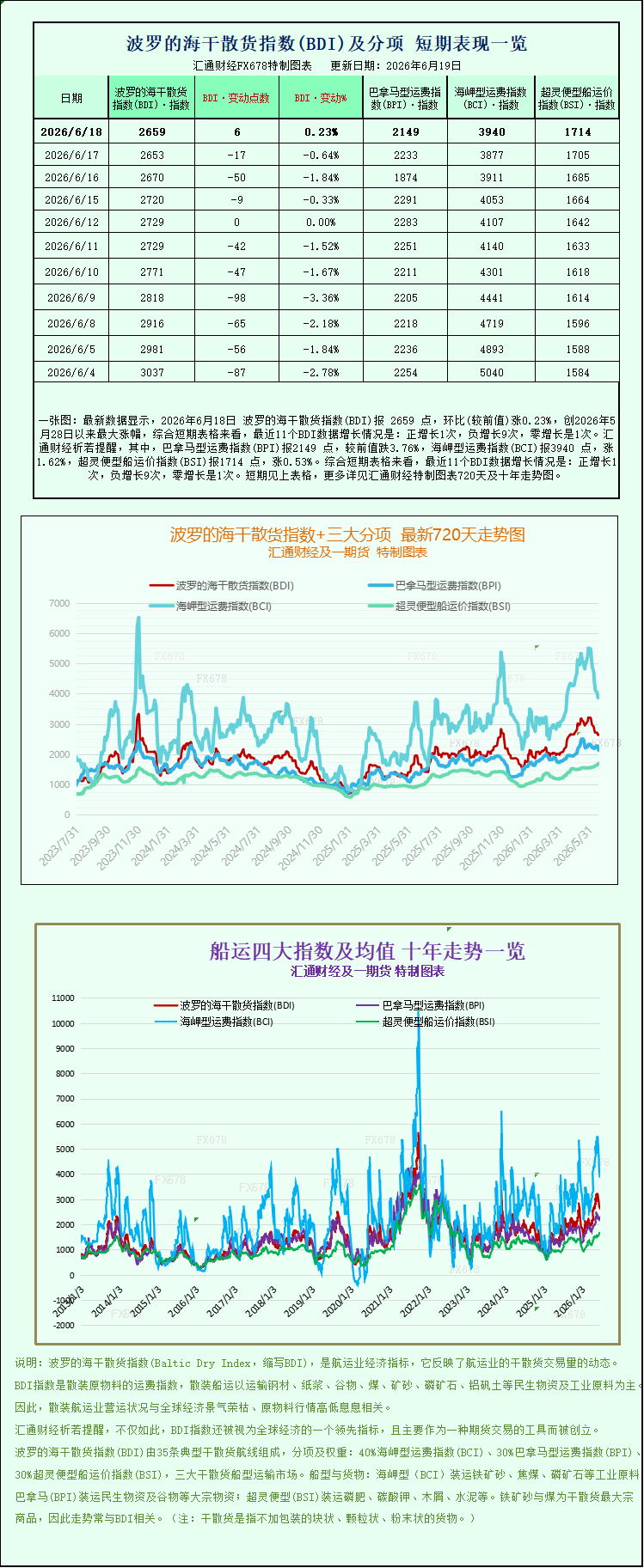

The latest data shows that the Baltic Dry Index (BDI) was 2659 points on June 18, 2026, up 0.23% from the previous week, marking the largest increase since May 28, 2026. Looking at the short-term charts, the recent 11 BDI data points show: one positive increase, nine negative increases, and one zero increase. Specifically, the Panamax Freight Index (BPI) was 2149 points, down 3.76% from the previous week; the Capesize Freight Index (BCI) was 3940 points, up 1.62%; and the Supramax Freight Index (BSI) was 1714 points, up 0.53%. For detailed 720-day and 10-year trend charts of the Baltic Dry Index and its three main sub-indices, please refer to the specially designed charts.

On June 18, 2026, the international dry bulk shipping market showed signs of stabilization. The Baltic Dry Index (BADI) rebounded slightly after hitting a near two-month low, ending its previous continuous downward trend. This market recovery was mainly driven by a significant increase in Capesize freight rates. However, the market performance of different vessel types diverged significantly, with Panamax freight rates continuing to decline. Overall, the industry is showing a pattern of structural repair and cautious recovery.

Data shows that the Baltic Dry Index (BDI), which tracks freight rates for the three major dry bulk carrier types—Capesize, Panamax, and Supramax—rose 6 points, or 0.2%, to close at 2659 points. The previous trading day, the index fell to 2653 points, its lowest level in two months since April 21st. The continued market downturn has made the industry cautious about short-term shipping trends, and this slight rebound has injected some confidence into the sluggish dry bulk market. From a market cycle perspective, the global dry bulk shipping market remained under pressure from April to early June. Affected by fluctuations in commodity demand and adjustments in regional freight schedules, freight rate indices fluctuated downwards. This rebound indicates that the short-term downward pressure on the market has eased somewhat.

As the core driver of the market rebound, the Capesize bulk carrier market has seen a significant recovery, with related data showing strong performance. The Baltic Capesize Index surged 63 points, or 1.6%, to 3940 points, reversing the two-month low reached in the previous trading day. In terms of revenue, Capesize vessels with a deadweight tonnage of 150,000 tons, primarily engaged in the transportation of bulk industrial raw materials such as iron ore and coal, saw their average daily earnings increase by $569 to $32,228. Capesize vessels mainly serve the cross-border transportation of global industrial raw materials, and their freight rate fluctuations are highly correlated with industrial production and commodity trade activity. This rebound indicates a phased recovery in global demand for bulk raw material shipping.

It is noteworthy that the recovery in the Capesize vessel market is showing a divergent trend in relation to the domestic commodity market. Affected by weak demand from the domestic steel industry, the iron ore market, a raw material for steel, continues to weaken, with Dalian iron ore futures closing lower for the third consecutive trading day. Currently, the pace of steel production in the domestic industry is slowing, and the recovery in demand from downstream construction and manufacturing sectors is weaker than expected, leading to a contraction in iron ore procurement demand. The cost support from the raw material side continues to weaken, and the decline in energy and transportation costs has further suppressed iron ore prices. This divergence between domestic and international markets also makes the sustainability of the Capesize freight rate rebound somewhat uncertain; the pace of recovery in domestic industrial demand still needs to be observed.

Unlike the strong rebound of Capesize vessels, the Panamax market continued its downward trend, showing relatively weak performance. Data shows that the Panamax index fell 74 points, or 3.3%, to 2149 points, the most significant drop among the three major vessel types. Revenue for the corresponding vessel type also declined. Panamax vessels, primarily engaged in the transportation of 60,000 to 70,000 tons of coal, grain, and other cargo, saw their average daily revenue decrease by $670 to $19,339. Looking back at the year's trend, the Panamax market reached a near four-year high in freight rates on May 15th, driven by active global grain trade and strong energy transportation demand. However, the recent rapid cooling of market activity is mainly due to a decline in short-term grain transportation orders and a slowdown in regional coal transportation, with the previously overdrawn market activity gradually returning to normal.

The small vessel market remained relatively stable, offsetting some of the downward pressure. The Supramax index rose slightly by 9 points, or 0.5%, to close at 1714 points, achieving a slight stabilization and rebound. Philippe Guvia, shipping analysis manager at the Baltic International Maritime Council (BIMCO), interpreted the market's divergent trend, stating that the Supramax market is currently facing structural pressures, with weak fertilizer transport demand significantly impacting it. In terms of demand structure, fertilizer accounts for only about 5% of total global dry bulk shipping demand, but it accounts for as much as 11% of the transportation demand for Supramax vessels. The decline in fertilizer freight volume directly dragged down the market performance of small vessels.

Meanwhile, Felipe Guvia pointed out that although there are negative factors affecting Supramax vessels, the steady increase in global grain seaborne volume, coupled with the phased improvement in the Capesize and Panamax markets, has jointly supported the bottoming out and rebound of the dry bulk composite index, preventing the overall market from remaining sluggish. Currently, global grain trade remains resilient, and the approaching peak harvest and transportation season in the Northern Hemisphere provides fundamental support for the small and medium-sized bulk carrier transportation market, becoming an important source of stability for the industry.

Furthermore, recent developments in the international geopolitical situation have also brought long-term positive expectations to the shipping market. The United States and Iran reached a memorandum of understanding agreeing to immediately open the Strait of Hormuz and lift the relevant US blockade against Iran. As a core choke point for global energy and commodity shipping, the Strait of Hormuz carries a large number of global oil, coal, and ore transport routes. Its unimpeded navigation will effectively alleviate international shipping logistics bottlenecks, reduce geopolitical risks and cost pressures in cross-border transportation, and lay a solid geopolitical foundation for the subsequent recovery of the dry bulk shipping market.

Overall, the global dry bulk shipping market is currently in a structural recovery phase, with significant divergence in performance across different vessel types. While the short-term rebound in Capesize vessels has stabilized the market, issues such as weak domestic demand for industrial raw materials and declining demand for Panamax vessels remain unresolved. Coupled with uneven market demand recovery, the industry as a whole has not yet entered a full recovery cycle. Future market trends will primarily depend on the recovery of domestic industrial demand, the pace of global food and energy trade, and the continued improvement in the geopolitical and navigation environment. Dry bulk freight rates are likely to exhibit a fluctuating recovery trend, with a gradual rebound.

On June 18, 2026, the international dry bulk shipping market showed signs of stabilization. The Baltic Dry Index (BADI) rebounded slightly after hitting a near two-month low, ending its previous continuous downward trend. This market recovery was mainly driven by a significant increase in Capesize freight rates. However, the market performance of different vessel types diverged significantly, with Panamax freight rates continuing to decline. Overall, the industry is showing a pattern of structural repair and cautious recovery.

Data shows that the Baltic Dry Index (BDI), which tracks freight rates for the three major dry bulk carrier types—Capesize, Panamax, and Supramax—rose 6 points, or 0.2%, to close at 2659 points. The previous trading day, the index fell to 2653 points, its lowest level in two months since April 21st. The continued market downturn has made the industry cautious about short-term shipping trends, and this slight rebound has injected some confidence into the sluggish dry bulk market. From a market cycle perspective, the global dry bulk shipping market remained under pressure from April to early June. Affected by fluctuations in commodity demand and adjustments in regional freight schedules, freight rate indices fluctuated downwards. This rebound indicates that the short-term downward pressure on the market has eased somewhat.

As the core driver of the market rebound, the Capesize bulk carrier market has seen a significant recovery, with related data showing strong performance. The Baltic Capesize Index surged 63 points, or 1.6%, to 3940 points, reversing the two-month low reached in the previous trading day. In terms of revenue, Capesize vessels with a deadweight tonnage of 150,000 tons, primarily engaged in the transportation of bulk industrial raw materials such as iron ore and coal, saw their average daily earnings increase by $569 to $32,228. Capesize vessels mainly serve the cross-border transportation of global industrial raw materials, and their freight rate fluctuations are highly correlated with industrial production and commodity trade activity. This rebound indicates a phased recovery in global demand for bulk raw material shipping.

It is noteworthy that the recovery in the Capesize vessel market is showing a divergent trend in relation to the domestic commodity market. Affected by weak demand from the domestic steel industry, the iron ore market, a raw material for steel, continues to weaken, with Dalian iron ore futures closing lower for the third consecutive trading day. Currently, the pace of steel production in the domestic industry is slowing, and the recovery in demand from downstream construction and manufacturing sectors is weaker than expected, leading to a contraction in iron ore procurement demand. The cost support from the raw material side continues to weaken, and the decline in energy and transportation costs has further suppressed iron ore prices. This divergence between domestic and international markets also makes the sustainability of the Capesize freight rate rebound somewhat uncertain; the pace of recovery in domestic industrial demand still needs to be observed.

Unlike the strong rebound of Capesize vessels, the Panamax market continued its downward trend, showing relatively weak performance. Data shows that the Panamax index fell 74 points, or 3.3%, to 2149 points, the most significant drop among the three major vessel types. Revenue for the corresponding vessel type also declined. Panamax vessels, primarily engaged in the transportation of 60,000 to 70,000 tons of coal, grain, and other cargo, saw their average daily revenue decrease by $670 to $19,339. Looking back at the year's trend, the Panamax market reached a near four-year high in freight rates on May 15th, driven by active global grain trade and strong energy transportation demand. However, the recent rapid cooling of market activity is mainly due to a decline in short-term grain transportation orders and a slowdown in regional coal transportation, with the previously overdrawn market activity gradually returning to normal.

The small vessel market remained relatively stable, offsetting some of the downward pressure. The Supramax index rose slightly by 9 points, or 0.5%, to close at 1714 points, achieving a slight stabilization and rebound. Philippe Guvia, shipping analysis manager at the Baltic International Maritime Council (BIMCO), interpreted the market's divergent trend, stating that the Supramax market is currently facing structural pressures, with weak fertilizer transport demand significantly impacting it. In terms of demand structure, fertilizer accounts for only about 5% of total global dry bulk shipping demand, but it accounts for as much as 11% of the transportation demand for Supramax vessels. The decline in fertilizer freight volume directly dragged down the market performance of small vessels.

Meanwhile, Felipe Guvia pointed out that although there are negative factors affecting Supramax vessels, the steady increase in global grain seaborne volume, coupled with the phased improvement in the Capesize and Panamax markets, has jointly supported the bottoming out and rebound of the dry bulk composite index, preventing the overall market from remaining sluggish. Currently, global grain trade remains resilient, and the approaching peak harvest and transportation season in the Northern Hemisphere provides fundamental support for the small and medium-sized bulk carrier transportation market, becoming an important source of stability for the industry.

Furthermore, recent developments in the international geopolitical situation have also brought long-term positive expectations to the shipping market. The United States and Iran reached a memorandum of understanding agreeing to immediately open the Strait of Hormuz and lift the relevant US blockade against Iran. As a core choke point for global energy and commodity shipping, the Strait of Hormuz carries a large number of global oil, coal, and ore transport routes. Its unimpeded navigation will effectively alleviate international shipping logistics bottlenecks, reduce geopolitical risks and cost pressures in cross-border transportation, and lay a solid geopolitical foundation for the subsequent recovery of the dry bulk shipping market.

Overall, the global dry bulk shipping market is currently in a structural recovery phase, with significant divergence in performance across different vessel types. While the short-term rebound in Capesize vessels has stabilized the market, issues such as weak domestic demand for industrial raw materials and declining demand for Panamax vessels remain unresolved. Coupled with uneven market demand recovery, the industry as a whole has not yet entered a full recovery cycle. Future market trends will primarily depend on the recovery of domestic industrial demand, the pace of global food and energy trade, and the continued improvement in the geopolitical and navigation environment. Dry bulk freight rates are likely to exhibit a fluctuating recovery trend, with a gradual rebound.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.