A chart shows that Capesize and Sussex vessel freight rates weakened, and the Baltic Dry Index declined slightly.

2026-06-24 23:07:55

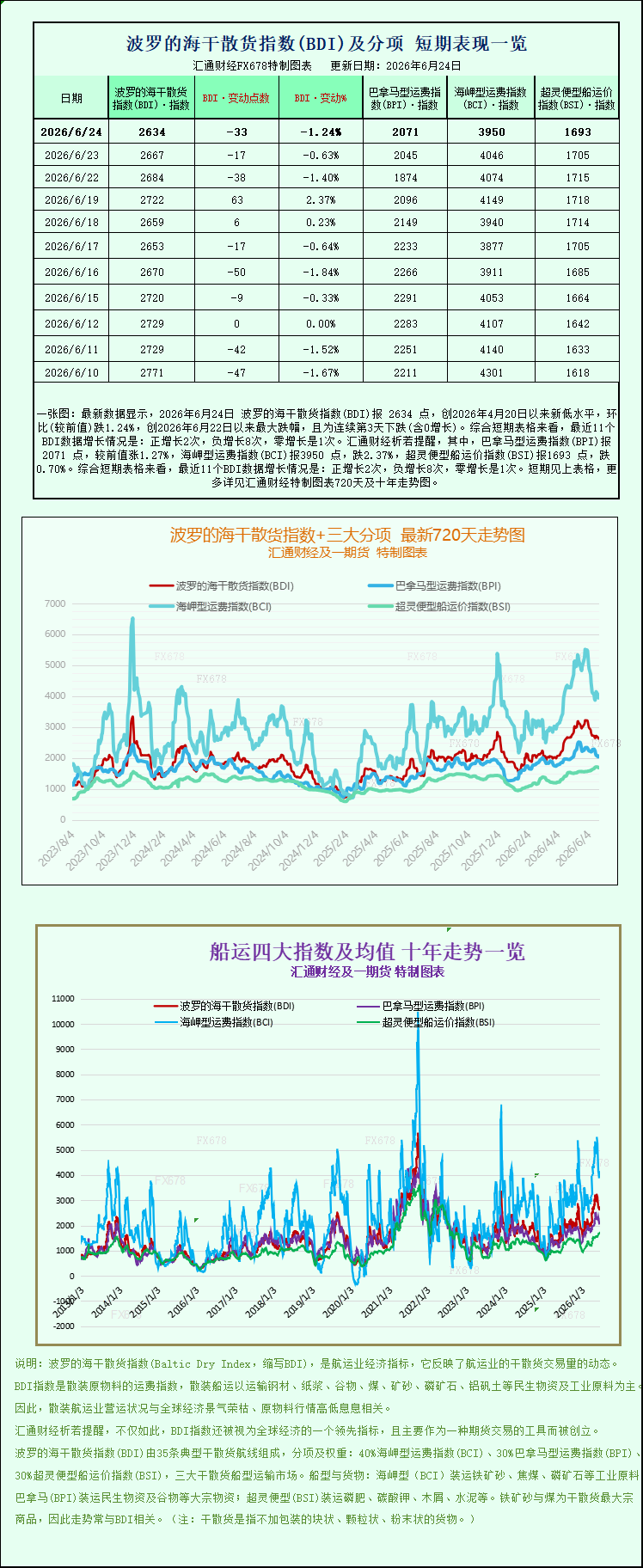

Latest data shows that the Baltic Dry Index (BDI) closed at 2634 points on June 24, 2026, a new low since April 20, 2026, down 1.24% month-on-month, the largest drop since June 22, 2026, and marking the third consecutive day of decline (including zero growth). Looking at the short-term charts, the recent 11 BDI data points show: 2 positive increases, 8 negative increases, and 1 zero increase. Specifically, the Panamax Freight Index (BPI) closed at 2071 points, up 1.27% from the previous value; the Capesize Freight Index (BCI) closed at 3950 points, down 2.37%; and the Supramax Freight Index (BSI) closed at 1693 points, down 0.70%. For detailed 720-day and 10-year trend charts of the Baltic Dry Index and its three main sub-indices, please refer to the specially designed charts.

On June 24th local time, the Baltic Dry Index (BADI) saw a slight pullback, dragged down by continued weakness in freight rates for Capesize and Supramax vessels. The core index closed lower overall, ending its previous period of steady recovery. As a key indicator of the global dry bulk shipping market, the BADI covers freight rate trends for the three major dry bulk vessel types: Capesize, Panamax, and Supramax. It directly reflects the global supply and demand dynamics of bulk commodities such as ore, coal, and grain. Its slight decline reflects the current divergent operating characteristics of the global bulk freight market.

Data shows that the Baltic Dry Index (BDI) fell 33 basis points, or 1.2%, to close at 2634 points. The sub-ship type indices showed a clear divergence, with a highly uneven market performance. Capesize vessels, the largest segment primarily used for long-haul bulk freight, were the main drag on the index, with the Capesize freight rate index (.BACI) falling sharply by 96 basis points, or 2.4%, to close at 3950 points, the lowest level since June 18th, indicating significant short-term market pressure.

Looking at vessel profitability data, the market profitability of Capesize vessels has declined accordingly. This vessel type primarily carries ultra-large bulk cargoes of 150,000 tons or more, with core transport categories including iron ore, thermal coal, and metallurgical coal—essential industrial raw materials—making it a core shipping capacity in the global industrial supply chain's maritime transport segment. On that day, the average daily earnings for Capesize vessels fell by $870, with the latest average daily profit dropping to $32,322. This decline in earnings is mainly due to a recent temporary cooling in demand for industrial raw material freight in the Asia-Pacific and Europe-US regions, resulting in a decrease in iron ore ocean shipping orders. Simultaneously, relatively ample short-term market capacity and a loose supply-demand relationship have suppressed the potential for freight rate increases.

In stark contrast to the sluggish performance of Capesize vessels, the Panamax market bucked the trend, becoming the only growth sector in the dry bulk market that day. Data shows that the Panamax freight rate index rose 26 basis points, or 1.3%, to close at 2071 points. This corresponds to an increase of $235 in average daily earnings per vessel, reaching $18,641. Panamax vessels, with a deadweight tonnage concentrated between 60,000 and 70,000 tons, are primarily suited to short-to-medium-haul, high-volume, and flexible freight demands for coal, grain, and cereals. They can navigate most major canals and small to medium-sized ports globally, making them more adaptable to various markets. The rise in freight rates was supported by demand during the peak season for global grain trade, coupled with the steady release of demand for agricultural exports from Europe and the United States and grain imports from Southeast Asia, offsetting the sluggishness in industrial raw material freight.

The market for small and medium-sized dry bulk carriers also continued its weak trend, with the Supramax freight rate index falling slightly by 12 basis points, or 0.7%, to close at 1693 points. As the mainstay of small and medium-sized dry bulk shipping, Supramax vessels cover a wide range of commodities and are suitable for regional and fragmented freight orders. The slight decline in their freight rates reflects the overall stable demand and lack of upward momentum in the small-volume bulk freight market, indicating that the market is in a phase of mild adjustment.

In its weekly industry report released on June 23, renowned shipbroker Allied offered a rational assessment of the current recovery trend in the dry bulk shipping market. The report points out that dry bulk shipping and product tankers are the two fastest-recovering and most significantly improving segments of the global shipping market. Against the backdrop of a slow global economic recovery and a gradual rebound in bulk commodity trade, these two sectors have been the first to emerge from their previous slump. However, the overall industry recovery is uneven and insufficient, with structural differentiation being particularly prominent.

Currently, the overall dry bulk shipping market's freight activity and route throughput have not yet returned to historical normal levels, and market participants remain cautious about the sustainability of the current industry recovery. On the one hand, the pace of global manufacturing recovery has slowed, making it difficult for demand for industrial raw material ocean shipping to continue to surge, thus limiting the upside potential for freight rates on large Capesize vessels. On the other hand, the global trade landscape continues to adjust, with regional trade replacing long-haul ocean trade becoming more prominent, further impacting the capacity utilization rate of traditional dry bulk routes, resulting in a weak overall market recovery.

Regarding geopolitical shipping routes, the recent stability of key shipping lanes has provided a fundamental guarantee for global dry bulk transportation. Vessel tracking data shows that in the past 12 hours, at least two dry bulk carriers and one cargo ship have successfully passed through the Strait of Hormuz thanks to relevant shipping support mechanisms. As a core choke point for global energy and bulk cargo shipping, the stable navigation of the Strait of Hormuz effectively avoids shipping disruptions caused by geopolitical risks, alleviating market concerns about capacity constraints and soaring freight rates. This is also a key reason for the recent overall stable adjustment and lack of drastic fluctuations in the dry bulk market.

In summary, the current global dry bulk shipping market exhibits a structurally differentiated pattern: large vessels are weakening, medium-sized vessels are strengthening, and small vessels are experiencing minor adjustments. In the short term, the decline in Capesize freight rates is likely to continue, primarily due to the off-season demand for industrial raw materials and ample shipping capacity. Meanwhile, the peak season for grain trade will continue to support Panamax vessel prices, becoming a core force for market stability. The overall industry recovery is still in the bottoming-out phase, and future market trends will highly depend on the progress of global manufacturing recovery, the pace of bulk raw material trade order releases, and the stability of key global shipping routes. A full market recovery still requires stronger demand-side support.

On June 24th local time, the Baltic Dry Index (BADI) saw a slight pullback, dragged down by continued weakness in freight rates for Capesize and Supramax vessels. The core index closed lower overall, ending its previous period of steady recovery. As a key indicator of the global dry bulk shipping market, the BADI covers freight rate trends for the three major dry bulk vessel types: Capesize, Panamax, and Supramax. It directly reflects the global supply and demand dynamics of bulk commodities such as ore, coal, and grain. Its slight decline reflects the current divergent operating characteristics of the global bulk freight market.

Data shows that the Baltic Dry Index (BDI) fell 33 basis points, or 1.2%, to close at 2634 points. The sub-ship type indices showed a clear divergence, with a highly uneven market performance. Capesize vessels, the largest segment primarily used for long-haul bulk freight, were the main drag on the index, with the Capesize freight rate index (.BACI) falling sharply by 96 basis points, or 2.4%, to close at 3950 points, the lowest level since June 18th, indicating significant short-term market pressure.

Looking at vessel profitability data, the market profitability of Capesize vessels has declined accordingly. This vessel type primarily carries ultra-large bulk cargoes of 150,000 tons or more, with core transport categories including iron ore, thermal coal, and metallurgical coal—essential industrial raw materials—making it a core shipping capacity in the global industrial supply chain's maritime transport segment. On that day, the average daily earnings for Capesize vessels fell by $870, with the latest average daily profit dropping to $32,322. This decline in earnings is mainly due to a recent temporary cooling in demand for industrial raw material freight in the Asia-Pacific and Europe-US regions, resulting in a decrease in iron ore ocean shipping orders. Simultaneously, relatively ample short-term market capacity and a loose supply-demand relationship have suppressed the potential for freight rate increases.

In stark contrast to the sluggish performance of Capesize vessels, the Panamax market bucked the trend, becoming the only growth sector in the dry bulk market that day. Data shows that the Panamax freight rate index rose 26 basis points, or 1.3%, to close at 2071 points. This corresponds to an increase of $235 in average daily earnings per vessel, reaching $18,641. Panamax vessels, with a deadweight tonnage concentrated between 60,000 and 70,000 tons, are primarily suited to short-to-medium-haul, high-volume, and flexible freight demands for coal, grain, and cereals. They can navigate most major canals and small to medium-sized ports globally, making them more adaptable to various markets. The rise in freight rates was supported by demand during the peak season for global grain trade, coupled with the steady release of demand for agricultural exports from Europe and the United States and grain imports from Southeast Asia, offsetting the sluggishness in industrial raw material freight.

The market for small and medium-sized dry bulk carriers also continued its weak trend, with the Supramax freight rate index falling slightly by 12 basis points, or 0.7%, to close at 1693 points. As the mainstay of small and medium-sized dry bulk shipping, Supramax vessels cover a wide range of commodities and are suitable for regional and fragmented freight orders. The slight decline in their freight rates reflects the overall stable demand and lack of upward momentum in the small-volume bulk freight market, indicating that the market is in a phase of mild adjustment.

In its weekly industry report released on June 23, renowned shipbroker Allied offered a rational assessment of the current recovery trend in the dry bulk shipping market. The report points out that dry bulk shipping and product tankers are the two fastest-recovering and most significantly improving segments of the global shipping market. Against the backdrop of a slow global economic recovery and a gradual rebound in bulk commodity trade, these two sectors have been the first to emerge from their previous slump. However, the overall industry recovery is uneven and insufficient, with structural differentiation being particularly prominent.

Currently, the overall dry bulk shipping market's freight activity and route throughput have not yet returned to historical normal levels, and market participants remain cautious about the sustainability of the current industry recovery. On the one hand, the pace of global manufacturing recovery has slowed, making it difficult for demand for industrial raw material ocean shipping to continue to surge, thus limiting the upside potential for freight rates on large Capesize vessels. On the other hand, the global trade landscape continues to adjust, with regional trade replacing long-haul ocean trade becoming more prominent, further impacting the capacity utilization rate of traditional dry bulk routes, resulting in a weak overall market recovery.

Regarding geopolitical shipping routes, the recent stability of key shipping lanes has provided a fundamental guarantee for global dry bulk transportation. Vessel tracking data shows that in the past 12 hours, at least two dry bulk carriers and one cargo ship have successfully passed through the Strait of Hormuz thanks to relevant shipping support mechanisms. As a core choke point for global energy and bulk cargo shipping, the stable navigation of the Strait of Hormuz effectively avoids shipping disruptions caused by geopolitical risks, alleviating market concerns about capacity constraints and soaring freight rates. This is also a key reason for the recent overall stable adjustment and lack of drastic fluctuations in the dry bulk market.

In summary, the current global dry bulk shipping market exhibits a structurally differentiated pattern: large vessels are weakening, medium-sized vessels are strengthening, and small vessels are experiencing minor adjustments. In the short term, the decline in Capesize freight rates is likely to continue, primarily due to the off-season demand for industrial raw materials and ample shipping capacity. Meanwhile, the peak season for grain trade will continue to support Panamax vessel prices, becoming a core force for market stability. The overall industry recovery is still in the bottoming-out phase, and future market trends will highly depend on the progress of global manufacturing recovery, the pace of bulk raw material trade order releases, and the stability of key global shipping routes. A full market recovery still requires stronger demand-side support.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.