Oil prices have fallen to post-war lows, but the Federal Reserve's interest rate path remains shrouded in uncertainty.

2026-06-25 20:14:48

On Thursday (June 25), WTI crude oil prices remained below $70 per barrel, hitting a low of $68.9 during the session, a new low since the outbreak of the Iraq War on February 28. This sharp drop in oil prices is expected to alleviate overall inflationary pressures in the coming months. However, the core question remains: will the bond market weaken in tandem and fully absorb the downward pressure on inflation? The pace of future interest rate hikes by the Federal Reserve remains uncertain.

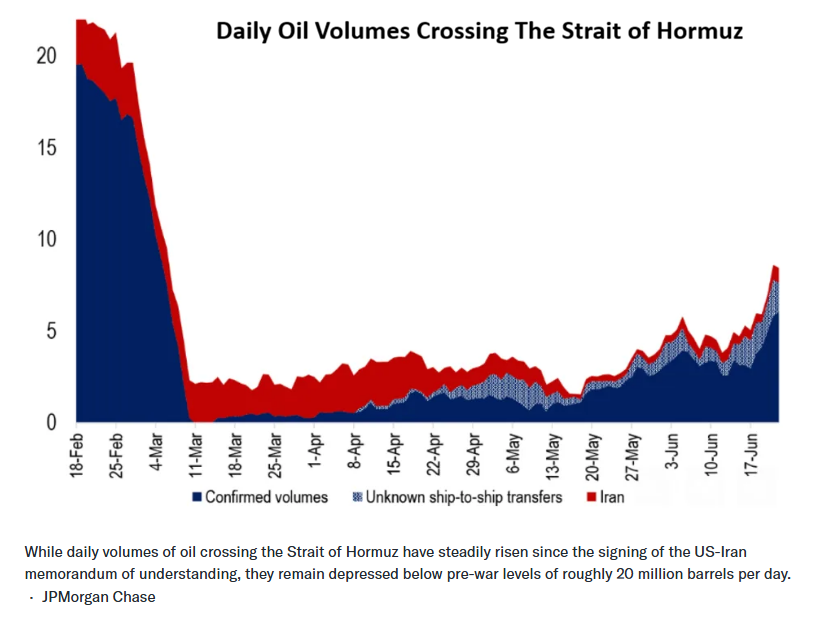

The core driver suppressing oil prices is a preliminary ceasefire agreement aimed at ending the Iraq War, and shipping through the Strait of Hormuz is gradually resuming, although the total volume of energy transport is still far from returning to pre-war levels. Matthew Wright, a freight analyst at global shipping analysis firm Kpler, said, "What shipping companies really value is a stable and unobstructed shipping environment for several days and weeks."

(Although daily oil shipments through the Strait of Hormuz have steadily increased since the signing of the memorandum of understanding between the United States and Iran, they are still below the pre-war level of approximately 20 million barrels per day.)

Current crude oil market pricing has already factored in expectations of a continued easing of tensions and a return to normal energy exports in the coming months. Francis Osborne, head of crude oil analysis at Argus Media, which tracks international oil prices, stated, "Traders have priced in a return to normalcy, but haven't considered the various potential risks that remain severe in the long term."

Despite lingering geopolitical risks in the Middle East, US Treasury yields have fallen, but the trends across different maturities have diverged significantly. The 30-year Treasury yield, which is most sensitive to inflation, fell sharply yesterday to 4.84% (and rebounded slightly today), hitting a multi-month low; the 10-year Treasury yield, the market benchmark, also declined, reversing the surge of the past month or so.

The only exception was the 2-year US Treasury yield, which is highly sensitive to monetary policy: although it fell slightly to 4.16%, it was only a step away from the high reached a few days ago. This signal sends a clear message: the market is not entirely convinced that inflation risks have subsided, nor does it believe that the Federal Reserve will stop raising interest rates.

Torsten Slok, chief economist at Apollo Global Management, has proposed a disruptive view: lower oil prices could actually push up inflation. He explains that the mainstream market logic is shifting from "lower oil prices = cooling inflation" to "lower oil prices will stimulate an already overheated economy to release more demand, ultimately raising inflation again." Influenced by the unexpectedly high Consumer Price Index (CPI) in April, the strong non-farm payroll data in May, and the Federal Reserve's consistently hawkish stance, the current mainstream market view is that the resumption of shipping in the Strait of Hormuz will further exacerbate the overheated economy, forcing the Federal Reserve to raise interest rates again in the short term.

With geopolitical conflicts and multiple macroeconomic uncertainties intertwined, it will take time to observe whether Slock's judgment holds true. However, in the short term, inflationary pressures are expected to ease to some extent.

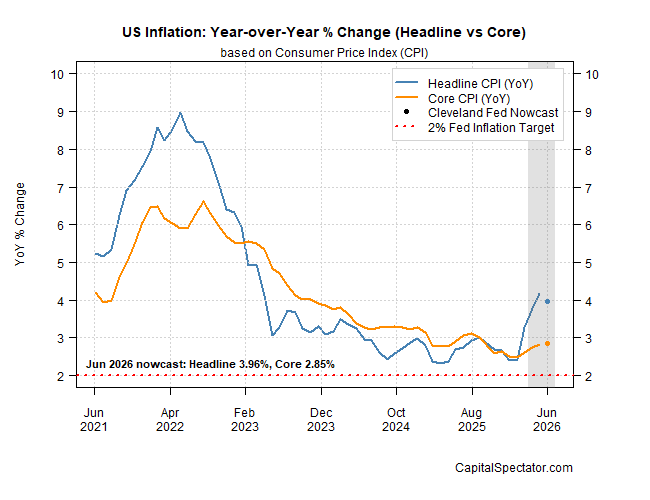

(The trend of US inflation as a percentage change year-on-year; inflation is expected to continue to decline slowly in 2026)

The Cleveland Federal Reserve's real-time CPI forecasting model indicates that after several consecutive months of inflation data exceeding expectations, the year-on-year growth rate of consumer prices will decline slightly. During the war, core CPI remained generally stable with only a slight increase; the model predicts that in this month's updated data, core CPI will rise by 2.9% year-on-year.

However, federal funds rate futures reflect the market's increased bet on a short-term rate hike: the probability of a 25 basis point rate hike at the next Federal Open Market Committee (FOMC) meeting on July 29 is 34%; by September, the market believes the probability of the Fed tightening monetary policy has risen to 67%.

Morningstar Investment Research predicts that the remaining short-term inflationary pressures will eventually subside: "We are optimistic about continued downward pressure on inflation over the next few years. The decline in energy prices will have a significant inflation-suppressing effect in 2027; the price shock from tariffs will also gradually disappear. In addition, wage growth has slowed significantly, which will help service inflation return to a reasonable range, and housing inflation will also continue its downward trend."

However, 2027 is still a long way off. While the market is currently welcoming the temporary benefits of cooling energy prices, the direction of the Federal Reserve's monetary policy remains uncertain, and this brief period of calm is likely to be short-lived.

The core driver suppressing oil prices is a preliminary ceasefire agreement aimed at ending the Iraq War, and shipping through the Strait of Hormuz is gradually resuming, although the total volume of energy transport is still far from returning to pre-war levels. Matthew Wright, a freight analyst at global shipping analysis firm Kpler, said, "What shipping companies really value is a stable and unobstructed shipping environment for several days and weeks."

(Although daily oil shipments through the Strait of Hormuz have steadily increased since the signing of the memorandum of understanding between the United States and Iran, they are still below the pre-war level of approximately 20 million barrels per day.)

Current crude oil market pricing has already factored in expectations of a continued easing of tensions and a return to normal energy exports in the coming months. Francis Osborne, head of crude oil analysis at Argus Media, which tracks international oil prices, stated, "Traders have priced in a return to normalcy, but haven't considered the various potential risks that remain severe in the long term."

Despite lingering geopolitical risks in the Middle East, US Treasury yields have fallen, but the trends across different maturities have diverged significantly. The 30-year Treasury yield, which is most sensitive to inflation, fell sharply yesterday to 4.84% (and rebounded slightly today), hitting a multi-month low; the 10-year Treasury yield, the market benchmark, also declined, reversing the surge of the past month or so.

The only exception was the 2-year US Treasury yield, which is highly sensitive to monetary policy: although it fell slightly to 4.16%, it was only a step away from the high reached a few days ago. This signal sends a clear message: the market is not entirely convinced that inflation risks have subsided, nor does it believe that the Federal Reserve will stop raising interest rates.

Torsten Slok, chief economist at Apollo Global Management, has proposed a disruptive view: lower oil prices could actually push up inflation. He explains that the mainstream market logic is shifting from "lower oil prices = cooling inflation" to "lower oil prices will stimulate an already overheated economy to release more demand, ultimately raising inflation again." Influenced by the unexpectedly high Consumer Price Index (CPI) in April, the strong non-farm payroll data in May, and the Federal Reserve's consistently hawkish stance, the current mainstream market view is that the resumption of shipping in the Strait of Hormuz will further exacerbate the overheated economy, forcing the Federal Reserve to raise interest rates again in the short term.

With geopolitical conflicts and multiple macroeconomic uncertainties intertwined, it will take time to observe whether Slock's judgment holds true. However, in the short term, inflationary pressures are expected to ease to some extent.

(The trend of US inflation as a percentage change year-on-year; inflation is expected to continue to decline slowly in 2026)

The Cleveland Federal Reserve's real-time CPI forecasting model indicates that after several consecutive months of inflation data exceeding expectations, the year-on-year growth rate of consumer prices will decline slightly. During the war, core CPI remained generally stable with only a slight increase; the model predicts that in this month's updated data, core CPI will rise by 2.9% year-on-year.

However, federal funds rate futures reflect the market's increased bet on a short-term rate hike: the probability of a 25 basis point rate hike at the next Federal Open Market Committee (FOMC) meeting on July 29 is 34%; by September, the market believes the probability of the Fed tightening monetary policy has risen to 67%.

Morningstar Investment Research predicts that the remaining short-term inflationary pressures will eventually subside: "We are optimistic about continued downward pressure on inflation over the next few years. The decline in energy prices will have a significant inflation-suppressing effect in 2027; the price shock from tariffs will also gradually disappear. In addition, wage growth has slowed significantly, which will help service inflation return to a reasonable range, and housing inflation will also continue its downward trend."

However, 2027 is still a long way off. While the market is currently welcoming the temporary benefits of cooling energy prices, the direction of the Federal Reserve's monetary policy remains uncertain, and this brief period of calm is likely to be short-lived.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.