Recession risks are rising! PCE may have peaked, and expectations for the dollar and interest rates are shifting.

2026-06-25 21:17:26

The Federal Reserve officially released the May Personal Consumption Expenditures Price Index, its core inflation watchdog.

Overall PCE rose 4.1% year-on-year, in line with market expectations, a significant increase from the previous value of 3.8% in April, reaching the peak since April 2023;

Excluding the highly volatile food and energy sectors, the core PCE rose 3.4% year-on-year, which is in line with market expectations and higher than the previous value of 3.3% in April, marking the highest level since October 2023.

The core reason for the short-term surge in inflation in May was that the geopolitical conflict between the US and Iran disrupted shipping in the Strait of Hormuz, pushing up gasoline retail prices across the United States.

Data from the American Automobile Association shows that fuel costs rose sharply in May, directly driving up the overall PCE reading.

However, the market has seen clear signs of a shift. Since May 20, international crude oil prices have continued to decline, retail gasoline prices have fallen by about $0.56 per gallon, US-Iran negotiations are progressing steadily, shipping capacity in the Taiwan Strait is gradually recovering, and the one-off price increase impact from energy is entering a phase of waning.

Morningstar senior economist Caldwell previously analyzed that the gradual fading of the tariff increase effect, coupled with the decline in crude oil prices, will continue to suppress inflation. As long as the strait is not closed to navigation for a long time, the central price level in the United States will steadily decline this year.

The release of this data further corroborates this judgment: short-term inflation driven by energy is not sustainable, and the overall PCE is showing increasingly clear signs of peaking.

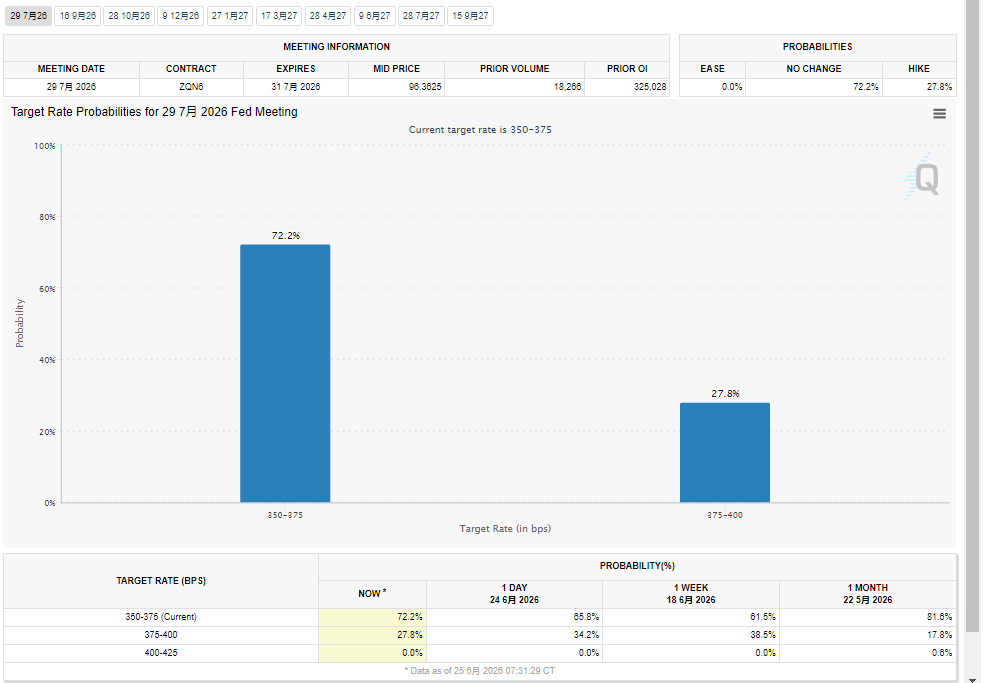

The market's earlier prediction that "May will be the peak of overall inflation for the year" has been validated. However, the stickiness of inflation and the downward pressure on the economy have become increasingly prominent. CME interest rate futures have seen a significant drop of 10% in the probability of a July rate hike, bringing it to 27.8%. The dual logic of wartime inflation and post-war recession brought about by the Middle East geopolitical conflict has further intensified.

(CME interest rate futures, source: CME Group)

Although overall inflation has reached a turning point, the resilience of core inflation components has not eased accordingly, becoming a key hidden danger suppressing the economy in the medium to long term.

First, inflation in the service sector remains high. Excluding housing, the year-on-year inflation rate of core services has climbed from 3.3% in the fourth quarter of 2025 to the current 3.7%. Rigid wage growth has increased labor costs for enterprises, and the pace of price cooling in the service sector is much slower than market expectations.

Secondly, the inflation logic on the commodity side has completely reversed. Durable goods, which had been weak for a long time before the pandemic, rose 3.3% year-on-year in April, with price increases covering all categories except fuel. Mott Capital analyst Kremer warned that if the natural deflationary buffer of durable goods disappears permanently, the underlying logic of inflation in the United States will change fundamentally, and relying solely on falling oil prices will not be enough to completely suppress prices.

In addition, the price increase effect brought about by the tariffs implemented last year has not yet been fully cleared. Bank of America's chief economist, Barway, pointed out that the deflationary dividend brought about by the housing sector has peaked, and multiple continuous supply shocks have significantly prolonged the period of sticky inflation.

The current Middle East conflict is replicating the classic economic cycle of "wartime inflation and post-war recession," and the US economy is contracting faster than the market had previously anticipated.

During the outbreak of the conflict, the contraction in the supply of crude oil and commodities directly pushed up prices, giving rise to a period of high inflation. The sustained high prices eroded residents' real disposable income, and coupled with the Federal Reserve's forced tightening of monetary policy to combat inflation, the cost of credit financing for the whole society increased, and consumption and business investment continued to weaken.

The market had previously bet that the Federal Reserve would cut interest rates to support weak employment, but the continuous rebound in inflation has completely reversed the expectations of easing.

Deutsche Bank predicts that the Federal Reserve will complete two rate hikes in 2026, raising the federal funds rate to 4.1%, and will pause rate adjustments in 2027. The rate cut cycle will not start until 2028 at the earliest.

Persistent high interest rates continue to squeeze domestic demand and corporate profits, and the US economy is gradually entering a stagflation environment of high inflation and low growth. The downward pressure on the economy will be concentrated in the second half of the year.

Several investment banks, including Bank of America, Goldman Sachs, and UBS, have previously stated that the May PCE trend will resonate with the CPI and PPI data for the same period.

A Bank of America research report noted that the ongoing geopolitical tensions in Iran have intensified global supply-side pressures, while rising stock markets have driven up financial services pricing. These two factors combined have supported stronger prices in May, and the current PCE data corroborates previous price indicators.

Meanwhile, institutions have reached a consensus on the future trend of inflation: UBS predicts that the overall PCE will decline sharply in June as oil prices fall, but the core PCE will remain at its current high level in June, and a clear cooling signal will not appear until July.

Federal Reserve Chairman Warsh insisted on a data-driven policy framework of phased interest rate decisions and would not lock in the interest rate path in advance. The inflation data, which met expectations, may continue to influence expectations for interest rate hikes at the end of the year.

From a trading perspective, the PCE data was in complete line with market expectations, and CME Fed rate futures pricing saw a sharp drop.

Previously, the market priced in a 25 basis point rate hike at the July FOMC meeting, which fluctuated around 36%, before plunging to 27%.

Positions priced in at least one rate hike this year also fluctuated slightly. Affected by moderate inflation data, the US dollar index experienced a brief surge followed by a decline.

As mentioned in yesterday's article, the plunge in US Treasury yields may be due to safe-haven funds buying US Treasuries, or simply a downward revision of inflation expectations, which has relieved the interest rate hike crisis. Currently, it seems more likely to be the latter, that is, the continuous plunge in US Treasury yields means that market concerns about inflation have subsided significantly.

Meanwhile, given the anticipated global recession following the war, traders betting on US interest rate hikes should be wary of the risks.

The absence of unexpected inflationary pressures in the short term will limit further upside potential for the US dollar.

However, the stickiness of core inflation in the medium to long term still needs to be observed, but the rapid drop in US Treasury bonds means that the downside potential of the US dollar is also limited.

The key indicators to watch in the future are the June PCE and non-farm payroll data. If overall inflation falls as expected in June and core inflation cools marginally, the US dollar index will experience a phase of correction. If core service inflation continues to strengthen, renewed expectations of interest rate hikes will drive the US dollar to open up upward space again.

Technical Analysis: The US dollar index has broken out of its trading range on the daily chart and is currently consolidating around the 50% retracement level, maintaining its strength. As long as the US dollar index remains strong, the market is still betting on an interest rate hike at the end of the year.

(US Dollar Index Daily Chart, Source: FX678)

At 21:12 Beijing time, the US dollar index is currently at 101.6.

Overall PCE rose 4.1% year-on-year, in line with market expectations, a significant increase from the previous value of 3.8% in April, reaching the peak since April 2023;

Excluding the highly volatile food and energy sectors, the core PCE rose 3.4% year-on-year, which is in line with market expectations and higher than the previous value of 3.3% in April, marking the highest level since October 2023.

Short-term inflationary spikes are driven by energy disturbances, and the decline in oil prices supports the logic that the overall PCE has peaked.

The core reason for the short-term surge in inflation in May was that the geopolitical conflict between the US and Iran disrupted shipping in the Strait of Hormuz, pushing up gasoline retail prices across the United States.

Data from the American Automobile Association shows that fuel costs rose sharply in May, directly driving up the overall PCE reading.

However, the market has seen clear signs of a shift. Since May 20, international crude oil prices have continued to decline, retail gasoline prices have fallen by about $0.56 per gallon, US-Iran negotiations are progressing steadily, shipping capacity in the Taiwan Strait is gradually recovering, and the one-off price increase impact from energy is entering a phase of waning.

Morningstar senior economist Caldwell previously analyzed that the gradual fading of the tariff increase effect, coupled with the decline in crude oil prices, will continue to suppress inflation. As long as the strait is not closed to navigation for a long time, the central price level in the United States will steadily decline this year.

The release of this data further corroborates this judgment: short-term inflation driven by energy is not sustainable, and the overall PCE is showing increasingly clear signs of peaking.

The market's earlier prediction that "May will be the peak of overall inflation for the year" has been validated. However, the stickiness of inflation and the downward pressure on the economy have become increasingly prominent. CME interest rate futures have seen a significant drop of 10% in the probability of a July rate hike, bringing it to 27.8%. The dual logic of wartime inflation and post-war recession brought about by the Middle East geopolitical conflict has further intensified.

(CME interest rate futures, source: CME Group)

Structural inflation remains sticky and persistent, with multiple factors prolonging the price decline cycle.

Although overall inflation has reached a turning point, the resilience of core inflation components has not eased accordingly, becoming a key hidden danger suppressing the economy in the medium to long term.

First, inflation in the service sector remains high. Excluding housing, the year-on-year inflation rate of core services has climbed from 3.3% in the fourth quarter of 2025 to the current 3.7%. Rigid wage growth has increased labor costs for enterprises, and the pace of price cooling in the service sector is much slower than market expectations.

Secondly, the inflation logic on the commodity side has completely reversed. Durable goods, which had been weak for a long time before the pandemic, rose 3.3% year-on-year in April, with price increases covering all categories except fuel. Mott Capital analyst Kremer warned that if the natural deflationary buffer of durable goods disappears permanently, the underlying logic of inflation in the United States will change fundamentally, and relying solely on falling oil prices will not be enough to completely suppress prices.

In addition, the price increase effect brought about by the tariffs implemented last year has not yet been fully cleared. Bank of America's chief economist, Barway, pointed out that the deflationary dividend brought about by the housing sector has peaked, and multiple continuous supply shocks have significantly prolonged the period of sticky inflation.

Geopolitical conflicts sow the seeds of stagflation: wartime inflation drives up prices, while post-war economic contraction accelerates.

The current Middle East conflict is replicating the classic economic cycle of "wartime inflation and post-war recession," and the US economy is contracting faster than the market had previously anticipated.

During the outbreak of the conflict, the contraction in the supply of crude oil and commodities directly pushed up prices, giving rise to a period of high inflation. The sustained high prices eroded residents' real disposable income, and coupled with the Federal Reserve's forced tightening of monetary policy to combat inflation, the cost of credit financing for the whole society increased, and consumption and business investment continued to weaken.

The market had previously bet that the Federal Reserve would cut interest rates to support weak employment, but the continuous rebound in inflation has completely reversed the expectations of easing.

Deutsche Bank predicts that the Federal Reserve will complete two rate hikes in 2026, raising the federal funds rate to 4.1%, and will pause rate adjustments in 2027. The rate cut cycle will not start until 2028 at the earliest.

Persistent high interest rates continue to squeeze domestic demand and corporate profits, and the US economy is gradually entering a stagflation environment of high inflation and low growth. The downward pressure on the economy will be concentrated in the second half of the year.

Data from multiple institutions, when cross-validated, shows a clear divergence in the pace of decline among different inflation components.

Several investment banks, including Bank of America, Goldman Sachs, and UBS, have previously stated that the May PCE trend will resonate with the CPI and PPI data for the same period.

A Bank of America research report noted that the ongoing geopolitical tensions in Iran have intensified global supply-side pressures, while rising stock markets have driven up financial services pricing. These two factors combined have supported stronger prices in May, and the current PCE data corroborates previous price indicators.

Meanwhile, institutions have reached a consensus on the future trend of inflation: UBS predicts that the overall PCE will decline sharply in June as oil prices fall, but the core PCE will remain at its current high level in June, and a clear cooling signal will not appear until July.

Federal Reserve Chairman Warsh insisted on a data-driven policy framework of phased interest rate decisions and would not lock in the interest rate path in advance. The inflation data, which met expectations, may continue to influence expectations for interest rate hikes at the end of the year.

Interest rate futures plunge, US Treasury yields ease interest rate hike crisis

From a trading perspective, the PCE data was in complete line with market expectations, and CME Fed rate futures pricing saw a sharp drop.

Previously, the market priced in a 25 basis point rate hike at the July FOMC meeting, which fluctuated around 36%, before plunging to 27%.

Positions priced in at least one rate hike this year also fluctuated slightly. Affected by moderate inflation data, the US dollar index experienced a brief surge followed by a decline.

As mentioned in yesterday's article, the plunge in US Treasury yields may be due to safe-haven funds buying US Treasuries, or simply a downward revision of inflation expectations, which has relieved the interest rate hike crisis. Currently, it seems more likely to be the latter, that is, the continuous plunge in US Treasury yields means that market concerns about inflation have subsided significantly.

Meanwhile, given the anticipated global recession following the war, traders betting on US interest rate hikes should be wary of the risks.

The absence of unexpected inflationary pressures in the short term will limit further upside potential for the US dollar.

However, the stickiness of core inflation in the medium to long term still needs to be observed, but the rapid drop in US Treasury bonds means that the downside potential of the US dollar is also limited.

The key indicators to watch in the future are the June PCE and non-farm payroll data. If overall inflation falls as expected in June and core inflation cools marginally, the US dollar index will experience a phase of correction. If core service inflation continues to strengthen, renewed expectations of interest rate hikes will drive the US dollar to open up upward space again.

Technical Analysis: The US dollar index has broken out of its trading range on the daily chart and is currently consolidating around the 50% retracement level, maintaining its strength. As long as the US dollar index remains strong, the market is still betting on an interest rate hike at the end of the year.

(US Dollar Index Daily Chart, Source: FX678)

At 21:12 Beijing time, the US dollar index is currently at 101.6.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.