A chart shows the Baltic Dry Index falling to a two-month low, with weaker freight rates for major vessel types dragging down market prices.

2026-06-25 23:57:29

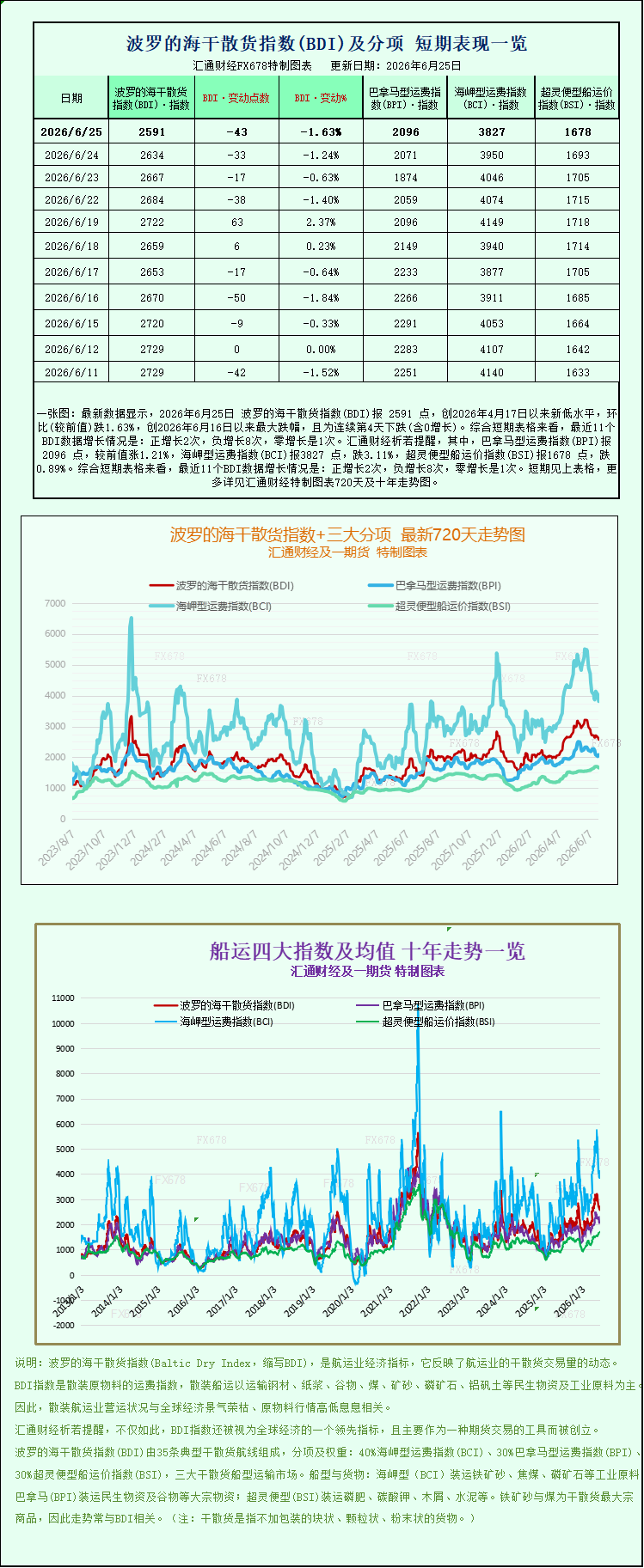

Latest data shows that the Baltic Dry Index (BDI) closed at 2591 points on June 25, 2026, a new low since April 17, 2026, down 1.63% month-on-month, the largest drop since June 16, 2026, and marking the fourth consecutive day of decline (including zero growth). Looking at the short-term charts, the recent 11 BDI data points show: 2 positive increases, 8 negative increases, and 1 zero increase. Specifically, the Panamax Freight Index (BPI) closed at 2096 points, up 1.21% from the previous value; the Capesize Freight Index (BCI) closed at 3827 points, down 3.11%; and the Supramax Freight Index (BSI) closed at 1678 points, down 0.89%. For detailed 720-day and 10-year trend charts of the Baltic Dry Index and its three main sub-indices, please refer to the specially designed charts.

On June 25, 2026, the international shipping market experienced a period of correction. Latest data released that evening showed that the Baltic Dry Index (BDI), the core benchmark for global dry bulk shipping, declined significantly on Thursday, indicating a continued cooling of overall market sentiment. By the close of trading that day, the Baltic Dry Index had fallen 43 points, a drop of 1.6%, to 2591 points, marking its lowest closing level in over two months since April 17th. This signifies the end of the recent upward trend in dry bulk shipping and a return to a weak adjustment phase. Looking at the sub-segments, the decline in the index showed a clear divergence, not a general decline across the entire industry. Freight rates for large Capesize vessels and small to medium-sized Supramax vessels weakened simultaneously, becoming the core factor dragging down the market. Meanwhile, Panamax vessels bucked the trend, rising due to the strong demand for food and energy transportation, offsetting some of the downward pressure. This fully reflects the structural supply-demand mismatch in the current global dry bulk shipping market.

As a barometer of global shipping and bulk commodity trade, the Baltic Dry Index (BDI) comprehensively tracks spot freight rates for the three major dry bulk carrier types: Capesize, Panamax, and Supramax. It directly reflects the transnational transport activity of basic commodities such as iron ore, coal, grains, fertilizers, and industrial building materials. Its fluctuations not only directly determine the revenue and profits of global shipping companies but also provide early predictions of global industrial production, infrastructure investment, and international trade trends. The recent decline in the index to a relatively low level indicates that overall global dry bulk shipping demand weakened at the end of the second quarter, and the previous market recovery momentum has largely subsided. Against the backdrop of weak macroeconomic demand and insufficient cargo volume, the shipping market has entered a period of adjustment.

Detailed ship type data shows that Capesize vessels, the largest in size and corresponding to the strongest demand for industrial raw material transportation, experienced the most significant decline in this round, becoming the core drag on the index. Data shows that the Capesize Exclusive Freight Index (BACI) fell sharply by 123 points in a single day, a drop of 3.1%, closing at 3827 points, leading the market decline. Correspondingly, vessel operating profits shrank significantly. Capesize spot vessels, mainly carrying 150,000-ton ultra-large bulk cargoes, saw their average daily earnings plummet by $1117, with the latest average daily revenue falling to $31205, a significant decline in profitability compared to the previous period. Capesize vessels primarily handle the ocean transport of core industrial raw materials such as iron ore, coking coal, and thermal coal from Brazil and Australia to China. These routes are highly dependent on domestic steel industry demand, and their freight rate fluctuations are closely linked to domestic steelmaking raw material procurement and industrial operating rates.

The core reason for the sharp drop in Capesize freight rates is the continued weakness in demand across the domestic steel industry chain, leading to pessimistic expectations regarding the transportation prospects of bulk steelmaking raw materials. Recently, the recovery in operating rates of downstream industries such as construction, machinery manufacturing, and steel structures has fallen short of expectations. Steel market inventories are high, transactions are weak, and steel prices remain under pressure. Domestic steel mills have generally adopted strategies of limiting production, reducing output, and controlling inventory, actively reducing the scale of procurement of raw materials such as iron ore and coking coal, resulting in a significant decrease in imported bulk raw material cargoes. Affected by the cooling demand, domestic coking coal spot prices have continued to decline recently, and market expectations for future steelmaking raw material imports and ocean shipping demand have continued to weaken. The contraction in demand has directly led to insufficient orders for ocean bulk cargo transportation, resulting in a relative surplus of available Capesize vessel capacity, and consequently, a significant decline in route freight rates and average daily vessel earnings.

The small bulk carrier market also continued its weak trend, further exacerbating the downward pressure on the overall market index. Data shows that the Supramax Freight Index (BSIS) fell 15 points, or 0.9%, to close at 1678 points, a near ten-day low since June 15th. Supramax vessels are flexible in tonnage and highly adaptable, mainly handling small to medium-sized batches of bulk cargo such as coal, grain, fertilizer, building materials, and non-ferrous metal ores. They widely cover short- and medium-haul routes within the global region and can sensitively reflect the true activity of a broad spectrum of global bulk cargo trade. The continued weakness in freight rates for this vessel type indicates that the current market weakness is not concentrated in the industrial raw materials sector. Overall global bulk cargo trade demand is insufficient. Apart from the steel industry chain, global infrastructure and small- to medium-sized industrial production-related bulk cargo transportation demand is also trending towards flatness, making the overall market recovery relatively weak.

Amidst a generally weak market, Panamax vessels bucked the trend, becoming the only positive support in the entire market. Data shows that the Panamax Freight Index (BPNI) rose 25 points, or 1.2%, to close at 2096 points; average daily vessel revenue increased by $224, steadily rising to $18,865. Panamax vessels primarily transport 60,000 to 70,000 tons of coal, grain, soybeans, and other energy and agricultural products, making them the mainstay of global energy trade and cross-border grain and oil circulation. This round of counter-trend increases is primarily due to support from global seasonal demand. Currently, it is the peak export season for grains from North and South America, leading to a continuous increase in global grain and oil trade volume and ample grain transport cargo capacity. Simultaneously, with the peak summer electricity consumption season approaching in the Northern Hemisphere, many countries are replenishing their thermal coal reserves in advance, resulting in a temporary recovery in energy import transportation demand. This effectively supports the tight supply and demand of Panamax vessels, driving freight rates upward against the trend.

Overall, the current dry bulk shipping market exhibits a distinct structural divergence: "cooling demand for industrial raw materials and robust demand for consumer energy and food." This explains the overall decline in the index and the mixed performance of different sub-sectors. On the supply side, global dry bulk vessel capacity deployment remains generally stable, with new vessels being delivered in an orderly manner and the scrapping of older vessels slowing down. The overall market capacity supply is ample, making it difficult to provide sustained support for freight rates. On the demand side, the slowdown in the global manufacturing recovery and weak domestic steel demand are the core negative factors suppressing the market. Meanwhile, the temporary inelastic demand for food and energy can only support certain types of vessels and cannot drive a recovery in overall market sentiment.

Looking ahead, the dry bulk shipping market is expected to maintain a structurally weak and volatile pattern in the short term. Domestic steel end-user demand shows no signs of a rapid recovery, and import demand for steelmaking raw materials is likely to remain under pressure, with Capesize freight rates likely to continue their weak and volatile trend. Meanwhile, the global peak season for grain exports continues, and Panamax freight rates are expected to maintain some resilience and continue to exhibit independent price movements. In the medium to long term, with the continued implementation of global pro-growth policies in the second half of the year, the gradual start of the traditional industrial peak season, and the steady recovery of domestic infrastructure and manufacturing demand, bulk cargo transportation demand is expected to marginally recover, driving the Baltic Dry Index to gradually stabilize and recover. However, given the moderate global economic recovery and limited overall growth in bulk trade, a one-sided surge in the market is unlikely; the market will likely continue to be characterized by structural differentiation and range-bound fluctuations.

On June 25, 2026, the international shipping market experienced a period of correction. Latest data released that evening showed that the Baltic Dry Index (BDI), the core benchmark for global dry bulk shipping, declined significantly on Thursday, indicating a continued cooling of overall market sentiment. By the close of trading that day, the Baltic Dry Index had fallen 43 points, a drop of 1.6%, to 2591 points, marking its lowest closing level in over two months since April 17th. This signifies the end of the recent upward trend in dry bulk shipping and a return to a weak adjustment phase. Looking at the sub-segments, the decline in the index showed a clear divergence, not a general decline across the entire industry. Freight rates for large Capesize vessels and small to medium-sized Supramax vessels weakened simultaneously, becoming the core factor dragging down the market. Meanwhile, Panamax vessels bucked the trend, rising due to the strong demand for food and energy transportation, offsetting some of the downward pressure. This fully reflects the structural supply-demand mismatch in the current global dry bulk shipping market.

As a barometer of global shipping and bulk commodity trade, the Baltic Dry Index (BDI) comprehensively tracks spot freight rates for the three major dry bulk carrier types: Capesize, Panamax, and Supramax. It directly reflects the transnational transport activity of basic commodities such as iron ore, coal, grains, fertilizers, and industrial building materials. Its fluctuations not only directly determine the revenue and profits of global shipping companies but also provide early predictions of global industrial production, infrastructure investment, and international trade trends. The recent decline in the index to a relatively low level indicates that overall global dry bulk shipping demand weakened at the end of the second quarter, and the previous market recovery momentum has largely subsided. Against the backdrop of weak macroeconomic demand and insufficient cargo volume, the shipping market has entered a period of adjustment.

Detailed ship type data shows that Capesize vessels, the largest in size and corresponding to the strongest demand for industrial raw material transportation, experienced the most significant decline in this round, becoming the core drag on the index. Data shows that the Capesize Exclusive Freight Index (BACI) fell sharply by 123 points in a single day, a drop of 3.1%, closing at 3827 points, leading the market decline. Correspondingly, vessel operating profits shrank significantly. Capesize spot vessels, mainly carrying 150,000-ton ultra-large bulk cargoes, saw their average daily earnings plummet by $1117, with the latest average daily revenue falling to $31205, a significant decline in profitability compared to the previous period. Capesize vessels primarily handle the ocean transport of core industrial raw materials such as iron ore, coking coal, and thermal coal from Brazil and Australia to China. These routes are highly dependent on domestic steel industry demand, and their freight rate fluctuations are closely linked to domestic steelmaking raw material procurement and industrial operating rates.

The core reason for the sharp drop in Capesize freight rates is the continued weakness in demand across the domestic steel industry chain, leading to pessimistic expectations regarding the transportation prospects of bulk steelmaking raw materials. Recently, the recovery in operating rates of downstream industries such as construction, machinery manufacturing, and steel structures has fallen short of expectations. Steel market inventories are high, transactions are weak, and steel prices remain under pressure. Domestic steel mills have generally adopted strategies of limiting production, reducing output, and controlling inventory, actively reducing the scale of procurement of raw materials such as iron ore and coking coal, resulting in a significant decrease in imported bulk raw material cargoes. Affected by the cooling demand, domestic coking coal spot prices have continued to decline recently, and market expectations for future steelmaking raw material imports and ocean shipping demand have continued to weaken. The contraction in demand has directly led to insufficient orders for ocean bulk cargo transportation, resulting in a relative surplus of available Capesize vessel capacity, and consequently, a significant decline in route freight rates and average daily vessel earnings.

The small bulk carrier market also continued its weak trend, further exacerbating the downward pressure on the overall market index. Data shows that the Supramax Freight Index (BSIS) fell 15 points, or 0.9%, to close at 1678 points, a near ten-day low since June 15th. Supramax vessels are flexible in tonnage and highly adaptable, mainly handling small to medium-sized batches of bulk cargo such as coal, grain, fertilizer, building materials, and non-ferrous metal ores. They widely cover short- and medium-haul routes within the global region and can sensitively reflect the true activity of a broad spectrum of global bulk cargo trade. The continued weakness in freight rates for this vessel type indicates that the current market weakness is not concentrated in the industrial raw materials sector. Overall global bulk cargo trade demand is insufficient. Apart from the steel industry chain, global infrastructure and small- to medium-sized industrial production-related bulk cargo transportation demand is also trending towards flatness, making the overall market recovery relatively weak.

Amidst a generally weak market, Panamax vessels bucked the trend, becoming the only positive support in the entire market. Data shows that the Panamax Freight Index (BPNI) rose 25 points, or 1.2%, to close at 2096 points; average daily vessel revenue increased by $224, steadily rising to $18,865. Panamax vessels primarily transport 60,000 to 70,000 tons of coal, grain, soybeans, and other energy and agricultural products, making them the mainstay of global energy trade and cross-border grain and oil circulation. This round of counter-trend increases is primarily due to support from global seasonal demand. Currently, it is the peak export season for grains from North and South America, leading to a continuous increase in global grain and oil trade volume and ample grain transport cargo capacity. Simultaneously, with the peak summer electricity consumption season approaching in the Northern Hemisphere, many countries are replenishing their thermal coal reserves in advance, resulting in a temporary recovery in energy import transportation demand. This effectively supports the tight supply and demand of Panamax vessels, driving freight rates upward against the trend.

Overall, the current dry bulk shipping market exhibits a distinct structural divergence: "cooling demand for industrial raw materials and robust demand for consumer energy and food." This explains the overall decline in the index and the mixed performance of different sub-sectors. On the supply side, global dry bulk vessel capacity deployment remains generally stable, with new vessels being delivered in an orderly manner and the scrapping of older vessels slowing down. The overall market capacity supply is ample, making it difficult to provide sustained support for freight rates. On the demand side, the slowdown in the global manufacturing recovery and weak domestic steel demand are the core negative factors suppressing the market. Meanwhile, the temporary inelastic demand for food and energy can only support certain types of vessels and cannot drive a recovery in overall market sentiment.

Looking ahead, the dry bulk shipping market is expected to maintain a structurally weak and volatile pattern in the short term. Domestic steel end-user demand shows no signs of a rapid recovery, and import demand for steelmaking raw materials is likely to remain under pressure, with Capesize freight rates likely to continue their weak and volatile trend. Meanwhile, the global peak season for grain exports continues, and Panamax freight rates are expected to maintain some resilience and continue to exhibit independent price movements. In the medium to long term, with the continued implementation of global pro-growth policies in the second half of the year, the gradual start of the traditional industrial peak season, and the steady recovery of domestic infrastructure and manufacturing demand, bulk cargo transportation demand is expected to marginally recover, driving the Baltic Dry Index to gradually stabilize and recover. However, given the moderate global economic recovery and limited overall growth in bulk trade, a one-sided surge in the market is unlikely; the market will likely continue to be characterized by structural differentiation and range-bound fluctuations.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.