One chart: The Baltic Dry Index rebounded after two months of slump, ushering in a window of opportunity for the large dry bulk shipping sector.

2026-06-30 23:48:45

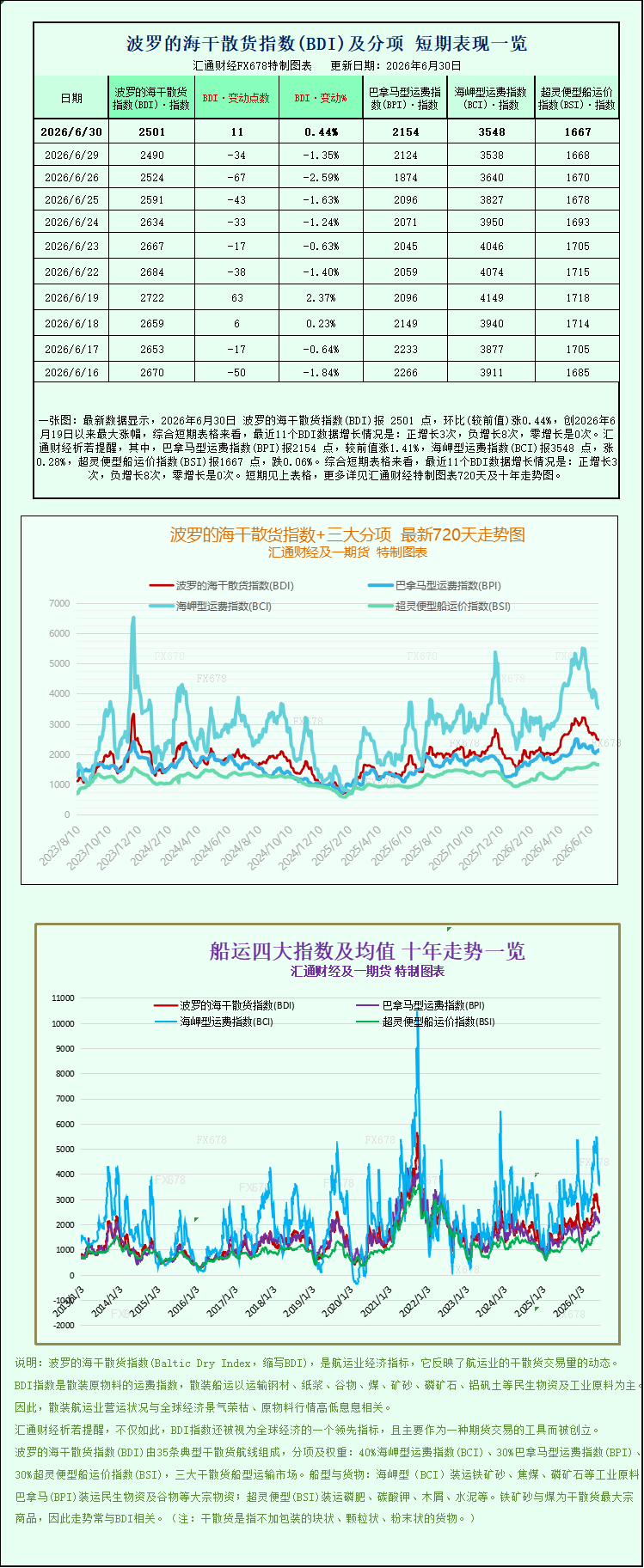

The latest data shows that the Baltic Dry Index (BDI) was 2501 points on June 30, 2026, up 0.44% from the previous week, marking the largest increase since June 19, 2026. Looking at the short-term charts, the BDI has seen positive growth 3 times, negative growth 8 times, and zero growth 0 times in the last 11 BDI data points. Specifically, the Panamax Freight Index (BPI) was 2154 points, up 1.41% from the previous week; the Capesize Freight Index (BCI) was 3548 points, up 0.28%; and the Supramax Freight Index (BSI) was 1667 points, down 0.06%. For detailed 720-day and 10-year trend charts of the Baltic Dry Index and its three main sub-indices, please refer to the specially designed charts.

The Baltic Dry Index (BADI), which tracks global dry bulk shipping freight rates, saw a slight rebound on Tuesday, ending its previous downward trend. The index hit a low point in more than two months, since April 15th, in the previous trading day. The rebound was driven by stronger freight rates for Capesize and Panamax vessels, signaling a temporary stabilization in the shipping market. Companies primarily operating large bulk carriers directly benefited from this freight rate recovery.

Looking at the specific market data for the day, the Baltic Dry Index (BDI), which aggregates freight rates for Capesize, Panamax, and Supramax vessels, rose 11 basis points, or 0.4%, to close at 2501 points. Previously, on Monday, the index had fallen below 2500 points, its lowest level in over two months, dragged down by weak short-term freight orders for iron ore and coal. The market had been concerned that dry bulk shipping was entering a new downward cycle. This slight rebound signals a key recovery in market sentiment and a clearing of short-term downward pressure. By vessel type, freight rates diverged significantly across different tonnages. Larger Capesize and Panamax vessels saw freight rate increases, while smaller Supramax vessels continued their weak and volatile trend.

Capesize vessels, the largest vessel type in the dry bulk market, were the core driver of this index rebound. The Baltic Capesize Index (.BACI) rose 10 points, or 0.3%, to close at 3548 points. These vessels have a certified deadweight of approximately 150,000 tons and primarily handle the long-distance transoceanic transport of industrial bulk commodities such as iron ore and metallurgical coal. They are also the most relied-upon vessel type for China's iron ore import trade. Market details show that the average daily operating revenue of Capesize vessels increased by $90 to $28,678, leading to an improvement in shipowners' immediate profitability.

The recent rise in Capesize freight rates is primarily driven by a recovery in demand for bulk commodities in China. Recent strong domestic manufacturing data has boosted steel mills' willingness to operate, leading to a corresponding increase in iron ore procurement demand. Meanwhile, shipments from major iron ore producing regions like Australia and Brazil have slowed recently, resulting in a decline in global short-term seaborne iron ore shipments and a tightening of the spot market supply, directly pushing up international iron ore futures prices. This price increase has offset previous pessimistic market expectations regarding shrinking profits for domestic steel companies, capacity reductions by steel mills, and reduced ore purchases. Traders are accelerating the signing of ocean-going charter orders, increasing short-term charter demand for Capesize vessels and consequently raising freight rates. Looking at the medium to long term, the Simandou high-grade iron ore project in Guinea continues to ramp up production. The sea distance from Guinea to China is far greater than that of the Brazil and Australia routes. This long-distance transportation model will continue to drive up the demand for Capesize vessels' ton-mile transport, providing long-term support for subsequent large vessel freight rates.

Panamax vessels emerged as another major driver of this market rally, outperforming Capesize vessels. The Panamax Index (.BPNI) surged 30 points, a 1.4% increase, closing at 2154 points. This vessel type, with a deadweight tonnage between 60,000 and 70,000 tons, primarily transports thermal coal, grains, and fertilizers. Its routes cover global grain and coal trade corridors and it can also transit the Panama Canal, offering greater trade flexibility. The average daily revenue for Panamax vessels increased by $266 to $19,383, demonstrating a significant improvement in profitability. Coal and grain are the two pillars supporting the Panamax vessel market. Summer is the peak season for global thermal power coal demand, with Asian countries increasing their coal import reserves. North and South American grain shipments are entering their export cycle, leading to increased orders for ocean freight of agricultural products such as wheat and corn. Furthermore, the reduced efficiency of the Panama Canal due to El Niño drought has prompted some cargo owners to detour around the Cape of Good Hope, extending transport distances and further amplifying demand for Panamax vessels, driving up freight rates.

In contrast, the market for smaller Supramax vessels did not follow the broader market recovery, instead exhibiting independent weakness. The Supramax index fell slightly by 1 point, a mere 0.06%, closing at 1667 points. These vessels have shallow drafts and primarily handle short-haul regional shipping and niche general cargo transport, relying on scattered regional orders and lacking the support of large-scale, long-distance commodity orders. The dispersed regional freight demand and relatively small order volume make it difficult to replicate the price increases seen with larger ocean-going vessels. Consequently, they have performed poorly in this round of market activity, resulting in a structural divergence in the dry bulk shipping market: "stronger large vessels, weaker small vessels."

From a shipping supply perspective, the fundamentals for future price increases in large dry bulk carriers are solid. Currently, new orders for dry bulk carriers account for only 11% of the overall fleet capacity, a near 25-year low, limiting the increase in new ship deliveries. Meanwhile, older vessels are subject to the International Maritime Organization's new carbon emission regulations (CII), leading to soaring operating costs for older, energy-intensive vessels. A large number of older Capesize and Panamax vessels are entering their scrapping cycle, resulting in a contraction in shipping capacity. With insufficient new vessel additions and accelerated clearing of aging capacity, if demand for bulk commodity shipping continues to rise, it will further exacerbate the tight supply-demand balance for large dry bulk carriers, raising the long-term freight rate center. Listed shipping companies holding large numbers of Capesize and Panamax vessels will continue to reap the benefits of rising freight rates.

From a macro perspective, global monetary policy and the geopolitical trade environment are also supporting dry bulk shipping. The global major economies have begun a cycle of interest rate cuts, reducing financing costs for commodity trade and increasing traders' willingness to stockpile and engage in transoceanic trade. Trade frictions between China and the US, and between Asia and Europe, have eased marginally, enhancing the stability of trade in grains, minerals, and energy, reducing uncertainty in shipping orders. In the short term, the Baltic Dry Index has just recovered from a two-month low, representing a rebound after bottoming out. Whether freight rates can continue to rise depends heavily on three core variables: the health of China's manufacturing sector, the pace of iron ore procurement by domestic steel mills, and the volume of iron ore shipments from Australia and Brazil. As long as demand from China's industrial sector remains resilient, freight rates for Capesize and Panamax vessels are likely to continue their upward trend, further extending the upward cycle of the entire large vessel shipping sector.

The Baltic Dry Index (BADI), which tracks global dry bulk shipping freight rates, saw a slight rebound on Tuesday, ending its previous downward trend. The index hit a low point in more than two months, since April 15th, in the previous trading day. The rebound was driven by stronger freight rates for Capesize and Panamax vessels, signaling a temporary stabilization in the shipping market. Companies primarily operating large bulk carriers directly benefited from this freight rate recovery.

Looking at the specific market data for the day, the Baltic Dry Index (BDI), which aggregates freight rates for Capesize, Panamax, and Supramax vessels, rose 11 basis points, or 0.4%, to close at 2501 points. Previously, on Monday, the index had fallen below 2500 points, its lowest level in over two months, dragged down by weak short-term freight orders for iron ore and coal. The market had been concerned that dry bulk shipping was entering a new downward cycle. This slight rebound signals a key recovery in market sentiment and a clearing of short-term downward pressure. By vessel type, freight rates diverged significantly across different tonnages. Larger Capesize and Panamax vessels saw freight rate increases, while smaller Supramax vessels continued their weak and volatile trend.

Capesize vessels, the largest vessel type in the dry bulk market, were the core driver of this index rebound. The Baltic Capesize Index (.BACI) rose 10 points, or 0.3%, to close at 3548 points. These vessels have a certified deadweight of approximately 150,000 tons and primarily handle the long-distance transoceanic transport of industrial bulk commodities such as iron ore and metallurgical coal. They are also the most relied-upon vessel type for China's iron ore import trade. Market details show that the average daily operating revenue of Capesize vessels increased by $90 to $28,678, leading to an improvement in shipowners' immediate profitability.

The recent rise in Capesize freight rates is primarily driven by a recovery in demand for bulk commodities in China. Recent strong domestic manufacturing data has boosted steel mills' willingness to operate, leading to a corresponding increase in iron ore procurement demand. Meanwhile, shipments from major iron ore producing regions like Australia and Brazil have slowed recently, resulting in a decline in global short-term seaborne iron ore shipments and a tightening of the spot market supply, directly pushing up international iron ore futures prices. This price increase has offset previous pessimistic market expectations regarding shrinking profits for domestic steel companies, capacity reductions by steel mills, and reduced ore purchases. Traders are accelerating the signing of ocean-going charter orders, increasing short-term charter demand for Capesize vessels and consequently raising freight rates. Looking at the medium to long term, the Simandou high-grade iron ore project in Guinea continues to ramp up production. The sea distance from Guinea to China is far greater than that of the Brazil and Australia routes. This long-distance transportation model will continue to drive up the demand for Capesize vessels' ton-mile transport, providing long-term support for subsequent large vessel freight rates.

Panamax vessels emerged as another major driver of this market rally, outperforming Capesize vessels. The Panamax Index (.BPNI) surged 30 points, a 1.4% increase, closing at 2154 points. This vessel type, with a deadweight tonnage between 60,000 and 70,000 tons, primarily transports thermal coal, grains, and fertilizers. Its routes cover global grain and coal trade corridors and it can also transit the Panama Canal, offering greater trade flexibility. The average daily revenue for Panamax vessels increased by $266 to $19,383, demonstrating a significant improvement in profitability. Coal and grain are the two pillars supporting the Panamax vessel market. Summer is the peak season for global thermal power coal demand, with Asian countries increasing their coal import reserves. North and South American grain shipments are entering their export cycle, leading to increased orders for ocean freight of agricultural products such as wheat and corn. Furthermore, the reduced efficiency of the Panama Canal due to El Niño drought has prompted some cargo owners to detour around the Cape of Good Hope, extending transport distances and further amplifying demand for Panamax vessels, driving up freight rates.

In contrast, the market for smaller Supramax vessels did not follow the broader market recovery, instead exhibiting independent weakness. The Supramax index fell slightly by 1 point, a mere 0.06%, closing at 1667 points. These vessels have shallow drafts and primarily handle short-haul regional shipping and niche general cargo transport, relying on scattered regional orders and lacking the support of large-scale, long-distance commodity orders. The dispersed regional freight demand and relatively small order volume make it difficult to replicate the price increases seen with larger ocean-going vessels. Consequently, they have performed poorly in this round of market activity, resulting in a structural divergence in the dry bulk shipping market: "stronger large vessels, weaker small vessels."

From a shipping supply perspective, the fundamentals for future price increases in large dry bulk carriers are solid. Currently, new orders for dry bulk carriers account for only 11% of the overall fleet capacity, a near 25-year low, limiting the increase in new ship deliveries. Meanwhile, older vessels are subject to the International Maritime Organization's new carbon emission regulations (CII), leading to soaring operating costs for older, energy-intensive vessels. A large number of older Capesize and Panamax vessels are entering their scrapping cycle, resulting in a contraction in shipping capacity. With insufficient new vessel additions and accelerated clearing of aging capacity, if demand for bulk commodity shipping continues to rise, it will further exacerbate the tight supply-demand balance for large dry bulk carriers, raising the long-term freight rate center. Listed shipping companies holding large numbers of Capesize and Panamax vessels will continue to reap the benefits of rising freight rates.

From a macro perspective, global monetary policy and the geopolitical trade environment are also supporting dry bulk shipping. The global major economies have begun a cycle of interest rate cuts, reducing financing costs for commodity trade and increasing traders' willingness to stockpile and engage in transoceanic trade. Trade frictions between China and the US, and between Asia and Europe, have eased marginally, enhancing the stability of trade in grains, minerals, and energy, reducing uncertainty in shipping orders. In the short term, the Baltic Dry Index has just recovered from a two-month low, representing a rebound after bottoming out. Whether freight rates can continue to rise depends heavily on three core variables: the health of China's manufacturing sector, the pace of iron ore procurement by domestic steel mills, and the volume of iron ore shipments from Australia and Brazil. As long as demand from China's industrial sector remains resilient, freight rates for Capesize and Panamax vessels are likely to continue their upward trend, further extending the upward cycle of the entire large vessel shipping sector.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.