A chart shows the Baltic Dry Index rising to a one-week high, with stronger profitability for Capesize vessels driving a market recovery.

2026-07-03 00:25:02

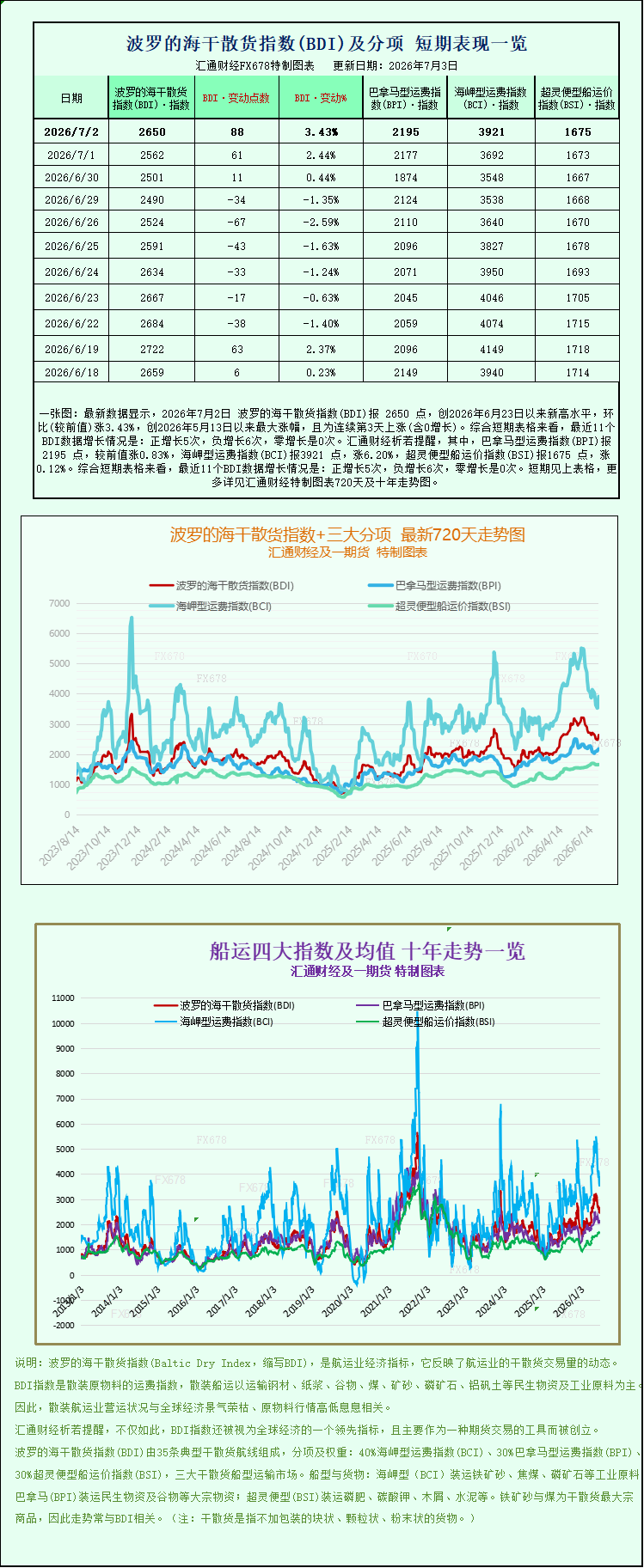

Latest data shows that the Baltic Dry Index (BDI) reached 2650 points on July 2, 2026, a new high since June 23, 2026, up 3.43% month-on-month (compared to the previous value), the largest increase since May 13, 2026, and the third consecutive day of increase (including zero growth). Looking at the short-term charts, the recent 11 BDI data points show: 5 positive increases, 6 negative increases, and 0 zero increases. Specifically, the Panamax Freight Index (BPI) was 2195 points, up 0.83% from the previous value; the Capesize Freight Index (BCI) was 3921 points, up 6.20%; and the Supramax Freight Index (BSI) was 1675 points, up 0.12%. For detailed 720-day and 10-year trend charts of the Baltic Dry Index and its three main sub-indices, please refer to the specially designed charts.

On July 2nd, the Baltic Dry Index (BDI) saw a significant rebound, with the overall index stabilizing above 2650 points, reaching its highest level in over a week since June 24th. This market recovery exhibits a clear structural trend, with freight rates and profitability for large Capesize bulk carriers surging, becoming the core driver of the index's rise. Meanwhile, freight rates for medium and small bulk carriers followed suit with smaller increases and relatively stable trends. The core catalyst behind this rally is the expectation of tightening iron ore supply in China, driving up iron ore prices and subsequently boosting long-haul shipping demand. The global dry bulk shipping market is experiencing a continued short-term recovery.

Data shows that the Baltic Dry Index (BDI), which reflects freight rates across all vessel types (Capemax, Panamax, and Supramax), rose 88 points, or 3.4%, to close at 2650 points, completely reversing the previous weak and volatile trend. Market chartering inquiries increased significantly, and shipowners' confidence in quoting prices continued to recover. In terms of vessel type, the market performance of different tonnage vessels showed a clear divergence, with large mining vessels significantly outperforming medium and small vessels, becoming the absolute driving force behind this index rebound.

The Capesize vessel market, a mainstay of iron ore ocean shipping, experienced a strong surge. The Capesize index jumped 229 points, a significant increase of 6.2%, closing at 3921 points, leading all vessel types in gains. Standard 150,000-ton deadweight Capesize vessels primarily handle long-haul iron ore transport from Australia, Brazil, and Guinea to China, while also handling large-scale coal ocean shipping. They are the vessel type most deeply intertwined with the dry bulk market and iron ore trade. Profitability data also improved dramatically, with average daily revenue increasing by $2,079 to $32,060 per day, resulting in a significant increase in per-vessel operating income and continuously expanding profit margins for shipowners.

The recent surge in Capesize freight rates is primarily driven by the tightening of the domestic iron ore distribution network. Recent market controls in China have restricted the delivery of some iron ore products from Australian mining giant Fortske to domestic steel mills, directly leading to a tightening of the domestic spot iron ore supply and pushing up iron ore futures prices. As the world's largest steel producer and iron ore consumer, China absorbs the vast majority of global seaborne iron ore supply, and Fortske exports most of its production capacity to China. These spot controls have directly reduced the short-term available supply, causing a rapid reversal in market supply and demand expectations.

To compensate for the supply shortage in Fortsk, domestic steel mills have begun to increase their iron ore purchases from distant mining areas such as Brazil and West Africa. Compared to the short-haul routes from Australia to China, the Brazil and West Africa routes involve longer distances, resulting in a significant increase in the demand for the same cargo volume in terms of sea freight ton-miles, directly driving up the rigid demand for Capesize vessels. Coupled with the current slow pace of new Capesize vessel capacity deployment, the market supply and demand remain in tight balance, further amplifying the increase in freight rates and driving a rapid rise in the profitability of large bulk carriers.

Medium-sized Panamax bulk carriers also saw a slight recovery, but the momentum was relatively mild. Data shows that the Panamax index rose 18 points, or 0.8%, to close at 2195 points, corresponding to an increase of $167 in average daily revenue per vessel, to $19,758 per day. This vessel type has a deadweight to 60,000-70,000 tons and primarily transports coal, grain, and other cargoes. Its routes are flexible, and it handles a diverse range of cargoes. Its performance is mainly supported by conventional fundamentals such as global coal consumption for thermal power plants and grain exports, and is minimally affected by the recent iron ore policy changes. Currently, summer restocking in European thermal power plants is creating temporary demand, supporting a slight recovery in freight rates, but the lack of strong incremental demand means the overall upward trend is gradual.

The market for small Supramax vessels remained largely stable, with the index rising only 2 points, or 0.1%, to close at 1675. These vessels have shallow drafts, are suitable for a wide range of ports, and primarily transport fertilizers, steel, and small-volume general cargo. Transportation demand is fragmented, and market capacity is ample. Coupled with the fact that global grain trade has not yet entered its traditional peak season, and the lack of new positive catalysts, freight rates remained within a narrow range, having a negligible impact on the overall index.

Overall, the current dry bulk market exhibits a typical structural trend of "strong performance from large vessels and stable performance from medium and small vessels," with iron ore supply news being the core factor influencing the market in the short term. Industry analysts point out that the market sentiment regarding tight iron ore supply will continue in the short term, and steel mills' continued restocking is expected to support Capesize freight rates at high levels, driving the overall index upward. However, uncertainties remain in the medium to long term, and it is necessary to continuously monitor the implementation of domestic iron ore policies, shipment volumes from major mining areas, and the purchasing pace of steel mills.

Meanwhile, small and medium-sized vessels, constrained by stable demand for certain cargo types and relatively ample shipping capacity, are unlikely to experience a significant market reversal in the short term and will generally maintain a moderate and volatile trend. This round of index rebound has effectively improved the profit expectations of large bulk carrier companies, further highlighting the divergence in industry performance. The subsequent market trend will continue to revolve around the commodity trading pattern and the supply and demand structure of maritime shipping.

On July 2nd, the Baltic Dry Index (BDI) saw a significant rebound, with the overall index stabilizing above 2650 points, reaching its highest level in over a week since June 24th. This market recovery exhibits a clear structural trend, with freight rates and profitability for large Capesize bulk carriers surging, becoming the core driver of the index's rise. Meanwhile, freight rates for medium and small bulk carriers followed suit with smaller increases and relatively stable trends. The core catalyst behind this rally is the expectation of tightening iron ore supply in China, driving up iron ore prices and subsequently boosting long-haul shipping demand. The global dry bulk shipping market is experiencing a continued short-term recovery.

Data shows that the Baltic Dry Index (BDI), which reflects freight rates across all vessel types (Capemax, Panamax, and Supramax), rose 88 points, or 3.4%, to close at 2650 points, completely reversing the previous weak and volatile trend. Market chartering inquiries increased significantly, and shipowners' confidence in quoting prices continued to recover. In terms of vessel type, the market performance of different tonnage vessels showed a clear divergence, with large mining vessels significantly outperforming medium and small vessels, becoming the absolute driving force behind this index rebound.

The Capesize vessel market, a mainstay of iron ore ocean shipping, experienced a strong surge. The Capesize index jumped 229 points, a significant increase of 6.2%, closing at 3921 points, leading all vessel types in gains. Standard 150,000-ton deadweight Capesize vessels primarily handle long-haul iron ore transport from Australia, Brazil, and Guinea to China, while also handling large-scale coal ocean shipping. They are the vessel type most deeply intertwined with the dry bulk market and iron ore trade. Profitability data also improved dramatically, with average daily revenue increasing by $2,079 to $32,060 per day, resulting in a significant increase in per-vessel operating income and continuously expanding profit margins for shipowners.

The recent surge in Capesize freight rates is primarily driven by the tightening of the domestic iron ore distribution network. Recent market controls in China have restricted the delivery of some iron ore products from Australian mining giant Fortske to domestic steel mills, directly leading to a tightening of the domestic spot iron ore supply and pushing up iron ore futures prices. As the world's largest steel producer and iron ore consumer, China absorbs the vast majority of global seaborne iron ore supply, and Fortske exports most of its production capacity to China. These spot controls have directly reduced the short-term available supply, causing a rapid reversal in market supply and demand expectations.

To compensate for the supply shortage in Fortsk, domestic steel mills have begun to increase their iron ore purchases from distant mining areas such as Brazil and West Africa. Compared to the short-haul routes from Australia to China, the Brazil and West Africa routes involve longer distances, resulting in a significant increase in the demand for the same cargo volume in terms of sea freight ton-miles, directly driving up the rigid demand for Capesize vessels. Coupled with the current slow pace of new Capesize vessel capacity deployment, the market supply and demand remain in tight balance, further amplifying the increase in freight rates and driving a rapid rise in the profitability of large bulk carriers.

Medium-sized Panamax bulk carriers also saw a slight recovery, but the momentum was relatively mild. Data shows that the Panamax index rose 18 points, or 0.8%, to close at 2195 points, corresponding to an increase of $167 in average daily revenue per vessel, to $19,758 per day. This vessel type has a deadweight to 60,000-70,000 tons and primarily transports coal, grain, and other cargoes. Its routes are flexible, and it handles a diverse range of cargoes. Its performance is mainly supported by conventional fundamentals such as global coal consumption for thermal power plants and grain exports, and is minimally affected by the recent iron ore policy changes. Currently, summer restocking in European thermal power plants is creating temporary demand, supporting a slight recovery in freight rates, but the lack of strong incremental demand means the overall upward trend is gradual.

The market for small Supramax vessels remained largely stable, with the index rising only 2 points, or 0.1%, to close at 1675. These vessels have shallow drafts, are suitable for a wide range of ports, and primarily transport fertilizers, steel, and small-volume general cargo. Transportation demand is fragmented, and market capacity is ample. Coupled with the fact that global grain trade has not yet entered its traditional peak season, and the lack of new positive catalysts, freight rates remained within a narrow range, having a negligible impact on the overall index.

Overall, the current dry bulk market exhibits a typical structural trend of "strong performance from large vessels and stable performance from medium and small vessels," with iron ore supply news being the core factor influencing the market in the short term. Industry analysts point out that the market sentiment regarding tight iron ore supply will continue in the short term, and steel mills' continued restocking is expected to support Capesize freight rates at high levels, driving the overall index upward. However, uncertainties remain in the medium to long term, and it is necessary to continuously monitor the implementation of domestic iron ore policies, shipment volumes from major mining areas, and the purchasing pace of steel mills.

Meanwhile, small and medium-sized vessels, constrained by stable demand for certain cargo types and relatively ample shipping capacity, are unlikely to experience a significant market reversal in the short term and will generally maintain a moderate and volatile trend. This round of index rebound has effectively improved the profit expectations of large bulk carrier companies, further highlighting the divergence in industry performance. The subsequent market trend will continue to revolve around the commodity trading pattern and the supply and demand structure of maritime shipping.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.