Weaker-than-expected non-farm payroll data has significantly cooled expectations for a Federal Reserve rate hike.

2026-07-03 01:29:44

After three consecutive months of steady recovery and continued expansion of new jobs, the US job market saw a significant slowdown in overall employment growth in June. While the official unemployment rate appeared to have fallen slightly, this positive data did not reflect an improvement in the real economy. Instead, it indicated that a large number of working-age individuals had voluntarily abandoned their job search plans and completely withdrawn from labor market statistics, with over 700,000 people no longer competing in the job market. This weak employment report, falling short of market expectations across the board, significantly undermined the mainstream expectation in global financial markets that the Federal Reserve would raise interest rates in the near future. If the upcoming July inflation monitoring data also shows a weakening trend, it will further solidify the Fed's policy logic of pausing its rate hike cycle and maintaining the current benchmark interest rate level.

June US employment performance: Data across the board fell short of expectations, with the unemployment rate's "false positive" report concealing hidden risks.

Non-farm payrolls fell far short of market expectations. In June, the U.S. non-farm payrolls increased by only 57,000 jobs, compared to a consensus forecast of 113,000 from major financial institutions – a near 50% drop. Simultaneously, the U.S. Bureau of Labor Statistics revised its April and May employment statistics, lowering the original figures by a combined 74,000 jobs. This suggests that the market's perception of a recovery in employment was significantly inflated, and the earlier labor market activity was substantially overestimated.

The unemployment rate fell slightly from 4.3% to 4.2% that month. Looking at the numerical change alone could easily lead to the misconception that the employment environment continued to improve. The core driver of this change was the significant drop in the labor force participation rate from 61.8% to 61.5%.

Breaking down the official statistics reveals the underlying issues: the number of employed people in the U.S. decreased by 500,000, and the number of registered unemployed people decreased by 213,000. The difference between the two figures directly reflects that more than 700,000 people have voluntarily left the labor market and stopped submitting resumes and looking for job opportunities.

The group most severely impacted by the shrinking willingness to work is the 25-54-year-old working-age population, whose labor force participation rate declined from 83.9% to 83.3%. As the core workforce in economic production, the continued contraction in job-seeking intentions among this group will constrain domestic consumption and industrial supply capacity in the long term, and the related risks warrant continued market vigilance. The market performance in terms of wages is entirely in line with institutional expectations: wages rose 0.3% month-on-month and 3.5% year-on-year, with overall wage growth remaining stable. There is no risk of wage overheating or a conversely, continued upward pressure on domestic inflation.

Employment is highly differentiated across industries, and employment growth is largely concentrated in a single source.

Overall demand for labor in the private sector remained sluggish, with only 49,000 new jobs added throughout the month. Employment expansion and contraction showed extreme divergence across different industries.

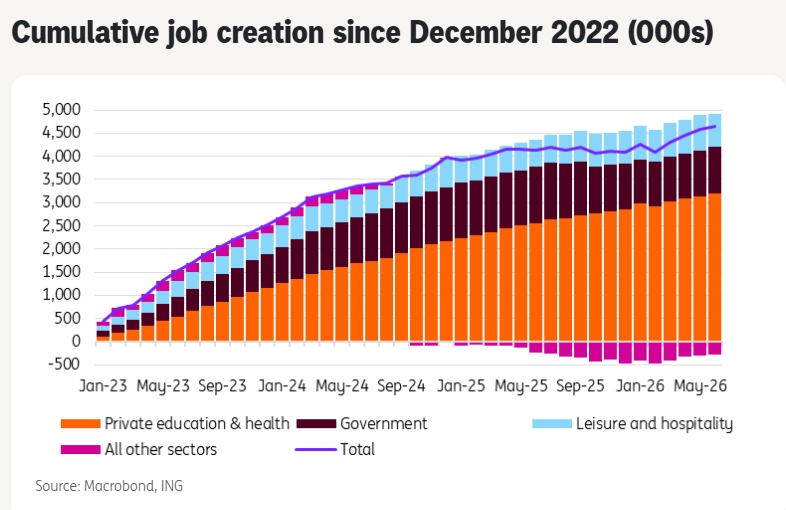

The private education and healthcare services sector was the only stable growth sector in the market, adding 69,000 jobs that month. Since December 2022, this sector has contributed 70% of all new jobs created in the United States. The increase in domestic employment is highly dependent on the education and healthcare sector, while most other industries lack the capacity to absorb new labor, highlighting the problem of an imbalanced employment structure.

The leisure and hospitality services industry experienced a sharper-than-expected decline, with a net decrease of 61,000 jobs in the month. Currently, during the World Cup, offline bars, stadiums, and restaurants/tourism venues are experiencing booming customer traffic. The significant drop in employment in this sector completely exceeded the prior predictions of all market institutions. In May, the industry even added 44,000 jobs. The market generally speculates that offline businesses overestimated the sustained consumer benefits of the World Cup and prematurely expanded their workforce. Subsequent customer traffic and revenue fell short of initial optimistic expectations, forcing them to reduce jobs to control labor costs.

Inflation remains the Federal Reserve's primary control target, and the probability of an interest rate hike this year has significantly decreased.

From January 2025 to February 2026, the average monthly increase in non-farm payrolls in the United States was only 8,571. A brief rebound occurred from March to May, with an average of 164,000 new jobs added per month over those three months. The weak employment statistics in June clearly demonstrate that the previous short-term employment recovery was unsustainable and will not develop into a long-term upward trend. Global foreign exchange and bond markets quickly repriced the Federal Reserve's monetary policy path, collectively reducing their bets on short-term interest rate hikes.

Federal Reserve Chairman Kevin Warsh has repeatedly stated publicly that the core objective of monetary policy at this stage remains to suppress persistently high inflation. Therefore, after the official release of the employment data, the overall volatility in the capital market was relatively mild: before the data release, market pricing reflected a cumulative interest rate hike expectation of 37 basis points by December; after the weak employment data was released, the market's cumulative interest rate hike expectation was directly lowered to 31 basis points.

On July 14, the U.S. Bureau of Labor Statistics will officially release the Consumer Price Index (CPI). Due to the impact of the decline in international crude oil prices on the domestic market and the sharp drop in gasoline prices, this inflation monitoring data is likely to show a month-on-month decline. Compared with the employment data, which has a stronger lag, the CPI can more directly reflect the current price trend and will also more profoundly change the judgment of various institutional investors on the pace of the Federal Reserve's subsequent policy operations.

Based on a comprehensive analysis of multiple existing data on the labor market and commodity prices, institutions predict that the market will remain stable in the medium to long term: the Federal Reserve will maintain the current benchmark interest rate for a considerable period of time and will not launch a new round of interest rate hikes throughout 2026.

June US employment performance: Data across the board fell short of expectations, with the unemployment rate's "false positive" report concealing hidden risks.

Non-farm payrolls fell far short of market expectations. In June, the U.S. non-farm payrolls increased by only 57,000 jobs, compared to a consensus forecast of 113,000 from major financial institutions – a near 50% drop. Simultaneously, the U.S. Bureau of Labor Statistics revised its April and May employment statistics, lowering the original figures by a combined 74,000 jobs. This suggests that the market's perception of a recovery in employment was significantly inflated, and the earlier labor market activity was substantially overestimated.

The unemployment rate fell slightly from 4.3% to 4.2% that month. Looking at the numerical change alone could easily lead to the misconception that the employment environment continued to improve. The core driver of this change was the significant drop in the labor force participation rate from 61.8% to 61.5%.

Breaking down the official statistics reveals the underlying issues: the number of employed people in the U.S. decreased by 500,000, and the number of registered unemployed people decreased by 213,000. The difference between the two figures directly reflects that more than 700,000 people have voluntarily left the labor market and stopped submitting resumes and looking for job opportunities.

The group most severely impacted by the shrinking willingness to work is the 25-54-year-old working-age population, whose labor force participation rate declined from 83.9% to 83.3%. As the core workforce in economic production, the continued contraction in job-seeking intentions among this group will constrain domestic consumption and industrial supply capacity in the long term, and the related risks warrant continued market vigilance. The market performance in terms of wages is entirely in line with institutional expectations: wages rose 0.3% month-on-month and 3.5% year-on-year, with overall wage growth remaining stable. There is no risk of wage overheating or a conversely, continued upward pressure on domestic inflation.

Employment is highly differentiated across industries, and employment growth is largely concentrated in a single source.

Overall demand for labor in the private sector remained sluggish, with only 49,000 new jobs added throughout the month. Employment expansion and contraction showed extreme divergence across different industries.

The private education and healthcare services sector was the only stable growth sector in the market, adding 69,000 jobs that month. Since December 2022, this sector has contributed 70% of all new jobs created in the United States. The increase in domestic employment is highly dependent on the education and healthcare sector, while most other industries lack the capacity to absorb new labor, highlighting the problem of an imbalanced employment structure.

The leisure and hospitality services industry experienced a sharper-than-expected decline, with a net decrease of 61,000 jobs in the month. Currently, during the World Cup, offline bars, stadiums, and restaurants/tourism venues are experiencing booming customer traffic. The significant drop in employment in this sector completely exceeded the prior predictions of all market institutions. In May, the industry even added 44,000 jobs. The market generally speculates that offline businesses overestimated the sustained consumer benefits of the World Cup and prematurely expanded their workforce. Subsequent customer traffic and revenue fell short of initial optimistic expectations, forcing them to reduce jobs to control labor costs.

Inflation remains the Federal Reserve's primary control target, and the probability of an interest rate hike this year has significantly decreased.

From January 2025 to February 2026, the average monthly increase in non-farm payrolls in the United States was only 8,571. A brief rebound occurred from March to May, with an average of 164,000 new jobs added per month over those three months. The weak employment statistics in June clearly demonstrate that the previous short-term employment recovery was unsustainable and will not develop into a long-term upward trend. Global foreign exchange and bond markets quickly repriced the Federal Reserve's monetary policy path, collectively reducing their bets on short-term interest rate hikes.

Federal Reserve Chairman Kevin Warsh has repeatedly stated publicly that the core objective of monetary policy at this stage remains to suppress persistently high inflation. Therefore, after the official release of the employment data, the overall volatility in the capital market was relatively mild: before the data release, market pricing reflected a cumulative interest rate hike expectation of 37 basis points by December; after the weak employment data was released, the market's cumulative interest rate hike expectation was directly lowered to 31 basis points.

On July 14, the U.S. Bureau of Labor Statistics will officially release the Consumer Price Index (CPI). Due to the impact of the decline in international crude oil prices on the domestic market and the sharp drop in gasoline prices, this inflation monitoring data is likely to show a month-on-month decline. Compared with the employment data, which has a stronger lag, the CPI can more directly reflect the current price trend and will also more profoundly change the judgment of various institutional investors on the pace of the Federal Reserve's subsequent policy operations.

Based on a comprehensive analysis of multiple existing data on the labor market and commodity prices, institutions predict that the market will remain stable in the medium to long term: the Federal Reserve will maintain the current benchmark interest rate for a considerable period of time and will not launch a new round of interest rate hikes throughout 2026.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.