A chart shows that the Baltic Dry Index declined slightly, dragged down by weak Capesize freight rates.

2026-07-08 23:40:04

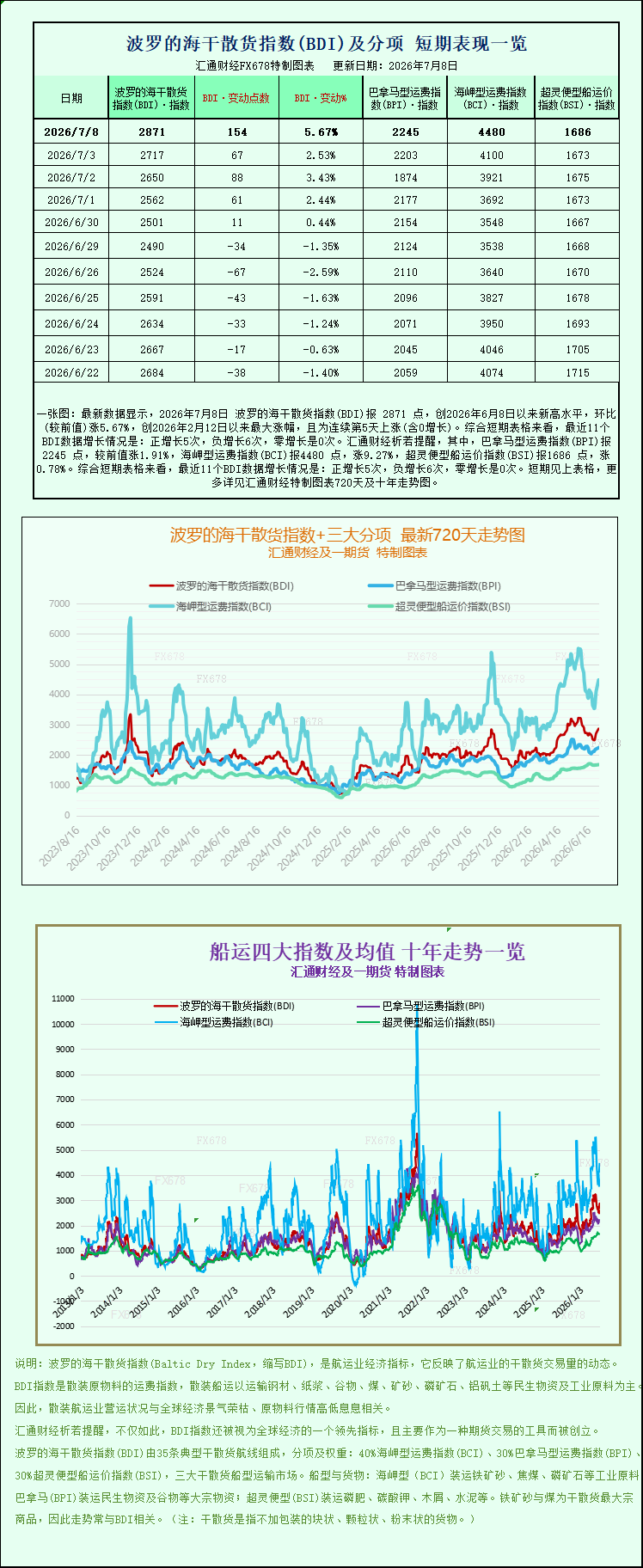

Latest data shows that the Baltic Dry Index (BDI) reached 2871 points on July 8, 2026, a new high since June 8, 2026, up 5.67% month-on-month, the largest increase since February 12, 2026, and marking the fifth consecutive day of increase (including zero growth). Looking at the short-term charts, the recent 11 BDI data points show: 5 positive increases, 6 negative increases, and 0 zero increases. Specifically, the Panamax Freight Index (BPI) reached 2245 points, up 1.91% from the previous value; the Capesize Freight Index (BCI) reached 4480 points, up 9.27%; and the Supramax Freight Index (BSI) reached 1686 points, up 0.78%. For detailed 720-day and 10-year trend charts of the Baltic Dry Index and its three main sub-indices, please refer to the specially designed charts.

The Baltic Exchange released its latest dry bulk freight data, showing a slight decline in the global core dry bulk shipping index, revealing a significant structural divergence in the market. This decline was primarily driven by weakening Capesize freight rates, while Panamax and Supramax vessel rates bucked the trend and rose. Meanwhile, iron ore futures rebounded, indicating a clear divergence between the shipping market and commodity price movements.

The Baltic Dry Index (BADI) is a core indicator of the global dry bulk shipping market, comprehensively reflecting freight rates for Capesize, Panamax, and Supramax vessels, and directly reflecting the prosperity of ocean shipping for bulk commodities such as iron ore, coal, and grain. Data for the day showed that the Baltic Dry Index fell 4 points, a decrease of 0.1%, closing at 2871 points. While the overall decline was moderate, significant differences in market conditions were observed across different vessel types.

As the ship type with the largest weighting in the index, the Capesize vessel market performed poorly, becoming a major drag on the overall market. On that day, the Capesize Vessel Index (BACI) fell 34 points, a drop of 0.8%, to 4480 points; the average daily revenue of 150,000-ton standard Capesize vessels, which mainly engage in ocean shipping of iron ore and coal, decreased by US$310 to US$37,130, and the short-term profits of large ship owners continued to be under pressure.

The weakening of Capesize freight rates stems from a loose short-term supply and demand situation. This vessel type is highly integrated into China's steel industry chain, with domestic market demand directly influencing ocean freight volumes. Currently, China is in the off-season for construction, and high temperatures and heavy rainfall are suppressing end-user steel demand. Steel mills have high inventories and shrinking production profits, leading them to actively control blast furnace operations and adopt a just-in-time purchasing model for Australian and Brazilian iron ore, resulting in a significant reduction in long-distance ocean-going iron ore shipments. Simultaneously, major overseas mines are entering their equipment maintenance cycles, causing a temporary decline in iron ore shipments, further compressing Capesize cargo availability. Coupled with the concentrated delivery of new ships and the return of idle capacity, short-term supply is ample, continuously suppressing large-vessel freight rates.

It's worth noting that while the shipping market was weak, iron ore futures bucked the trend and rose on the same day. This price increase was mainly driven by improved domestic warehousing demand and a marginal recovery in real estate sales. Market expectations for a recovery in the real estate market in the second half of the year and concentrated restocking by steel mills were rising, pushing iron ore futures higher. However, these long-term positive factors have not yet materialized, and short-term spot demand remained weak, ultimately resulting in a divergence between rising futures prices and weakening shipping prices.

Unlike the sluggish large vessel market, the small and medium-sized bulk carrier market performed strongly, effectively offsetting the downward pressure on the overall market. The Panamax Index (BPNI) rose 15 points, or 0.7%, to 2245 points that day. The average daily revenue of this type of vessel, primarily engaged in short- and medium-haul coal and grain transportation, increased by $140 to $20,209. This robust market performance was mainly due to the peak season for global grain trade, ample export orders for grain from North and South America and the Black Sea, coupled with stable demand for coal for summer thermal power generation in Southeast Asia and South Asia. This resulted in a consistently abundant supply of cargo for short- and medium-haul freight, supporting a steady rise in freight rates.

Supramax vessels also maintained their upward trend, with the index (BSIS) rising 10 points, or 0.6%, to 1686 points. These vessels are highly flexible and suitable for transporting small-volume bulk cargoes such as bauxite, building materials, and fertilizers, and are less affected by the off-season in the steel industry chain. Currently, global inter-regional trade in small-volume industrial products is stable, and infrastructure projects in Southeast Asia continue to release freight demand, driving a sustained recovery in small-vehicle freight rates.

Overall, the current dry bulk shipping market lacks a unified cyclical trend and exhibits a clear structural divergence: large vessels, heavily reliant on industrial raw materials, are weakening due to the off-season downturn, while small and medium-sized vessels, dependent on grain and regional trade, are maintaining a robust market. Industry analysts indicate that Capesize freight rates may continue their volatile and weak trend in the short term, as the off-season freight shortage is unlikely to be quickly compensated for; however, with the completion of overseas mine maintenance and a recovery in domestic downstream demand in the third quarter, large vessel freight rates have room for recovery. Meanwhile, small and medium-sized vessels have ample cargo support, and their high-level prosperity is likely to continue.

From a supply chain perspective, the short-term decline in Capesize freight rates can slightly reduce the logistics costs of imported iron ore for domestic steel mills, offsetting the pressure of rising raw material prices. For shipping companies, differences in fleet structure will lead to profit divergence; companies heavily invested in large bulk carriers will face short-term profit pressure, while those focusing on small and medium-sized vessels will have greater operational stability. Going forward, the market's core focus will be on three key indicators: the pace of domestic steel mill restocking, overseas mine shipments, and the global grain export situation.

The Baltic Exchange released its latest dry bulk freight data, showing a slight decline in the global core dry bulk shipping index, revealing a significant structural divergence in the market. This decline was primarily driven by weakening Capesize freight rates, while Panamax and Supramax vessel rates bucked the trend and rose. Meanwhile, iron ore futures rebounded, indicating a clear divergence between the shipping market and commodity price movements.

The Baltic Dry Index (BADI) is a core indicator of the global dry bulk shipping market, comprehensively reflecting freight rates for Capesize, Panamax, and Supramax vessels, and directly reflecting the prosperity of ocean shipping for bulk commodities such as iron ore, coal, and grain. Data for the day showed that the Baltic Dry Index fell 4 points, a decrease of 0.1%, closing at 2871 points. While the overall decline was moderate, significant differences in market conditions were observed across different vessel types.

As the ship type with the largest weighting in the index, the Capesize vessel market performed poorly, becoming a major drag on the overall market. On that day, the Capesize Vessel Index (BACI) fell 34 points, a drop of 0.8%, to 4480 points; the average daily revenue of 150,000-ton standard Capesize vessels, which mainly engage in ocean shipping of iron ore and coal, decreased by US$310 to US$37,130, and the short-term profits of large ship owners continued to be under pressure.

The weakening of Capesize freight rates stems from a loose short-term supply and demand situation. This vessel type is highly integrated into China's steel industry chain, with domestic market demand directly influencing ocean freight volumes. Currently, China is in the off-season for construction, and high temperatures and heavy rainfall are suppressing end-user steel demand. Steel mills have high inventories and shrinking production profits, leading them to actively control blast furnace operations and adopt a just-in-time purchasing model for Australian and Brazilian iron ore, resulting in a significant reduction in long-distance ocean-going iron ore shipments. Simultaneously, major overseas mines are entering their equipment maintenance cycles, causing a temporary decline in iron ore shipments, further compressing Capesize cargo availability. Coupled with the concentrated delivery of new ships and the return of idle capacity, short-term supply is ample, continuously suppressing large-vessel freight rates.

It's worth noting that while the shipping market was weak, iron ore futures bucked the trend and rose on the same day. This price increase was mainly driven by improved domestic warehousing demand and a marginal recovery in real estate sales. Market expectations for a recovery in the real estate market in the second half of the year and concentrated restocking by steel mills were rising, pushing iron ore futures higher. However, these long-term positive factors have not yet materialized, and short-term spot demand remained weak, ultimately resulting in a divergence between rising futures prices and weakening shipping prices.

Unlike the sluggish large vessel market, the small and medium-sized bulk carrier market performed strongly, effectively offsetting the downward pressure on the overall market. The Panamax Index (BPNI) rose 15 points, or 0.7%, to 2245 points that day. The average daily revenue of this type of vessel, primarily engaged in short- and medium-haul coal and grain transportation, increased by $140 to $20,209. This robust market performance was mainly due to the peak season for global grain trade, ample export orders for grain from North and South America and the Black Sea, coupled with stable demand for coal for summer thermal power generation in Southeast Asia and South Asia. This resulted in a consistently abundant supply of cargo for short- and medium-haul freight, supporting a steady rise in freight rates.

Supramax vessels also maintained their upward trend, with the index (BSIS) rising 10 points, or 0.6%, to 1686 points. These vessels are highly flexible and suitable for transporting small-volume bulk cargoes such as bauxite, building materials, and fertilizers, and are less affected by the off-season in the steel industry chain. Currently, global inter-regional trade in small-volume industrial products is stable, and infrastructure projects in Southeast Asia continue to release freight demand, driving a sustained recovery in small-vehicle freight rates.

Overall, the current dry bulk shipping market lacks a unified cyclical trend and exhibits a clear structural divergence: large vessels, heavily reliant on industrial raw materials, are weakening due to the off-season downturn, while small and medium-sized vessels, dependent on grain and regional trade, are maintaining a robust market. Industry analysts indicate that Capesize freight rates may continue their volatile and weak trend in the short term, as the off-season freight shortage is unlikely to be quickly compensated for; however, with the completion of overseas mine maintenance and a recovery in domestic downstream demand in the third quarter, large vessel freight rates have room for recovery. Meanwhile, small and medium-sized vessels have ample cargo support, and their high-level prosperity is likely to continue.

From a supply chain perspective, the short-term decline in Capesize freight rates can slightly reduce the logistics costs of imported iron ore for domestic steel mills, offsetting the pressure of rising raw material prices. For shipping companies, differences in fleet structure will lead to profit divergence; companies heavily invested in large bulk carriers will face short-term profit pressure, while those focusing on small and medium-sized vessels will have greater operational stability. Going forward, the market's core focus will be on three key indicators: the pace of domestic steel mill restocking, overseas mine shipments, and the global grain export situation.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.