One chart: Strong freight rates across all sectors boost the market; Baltic Dry Index hits one-month high.

2026-07-09 23:15:32

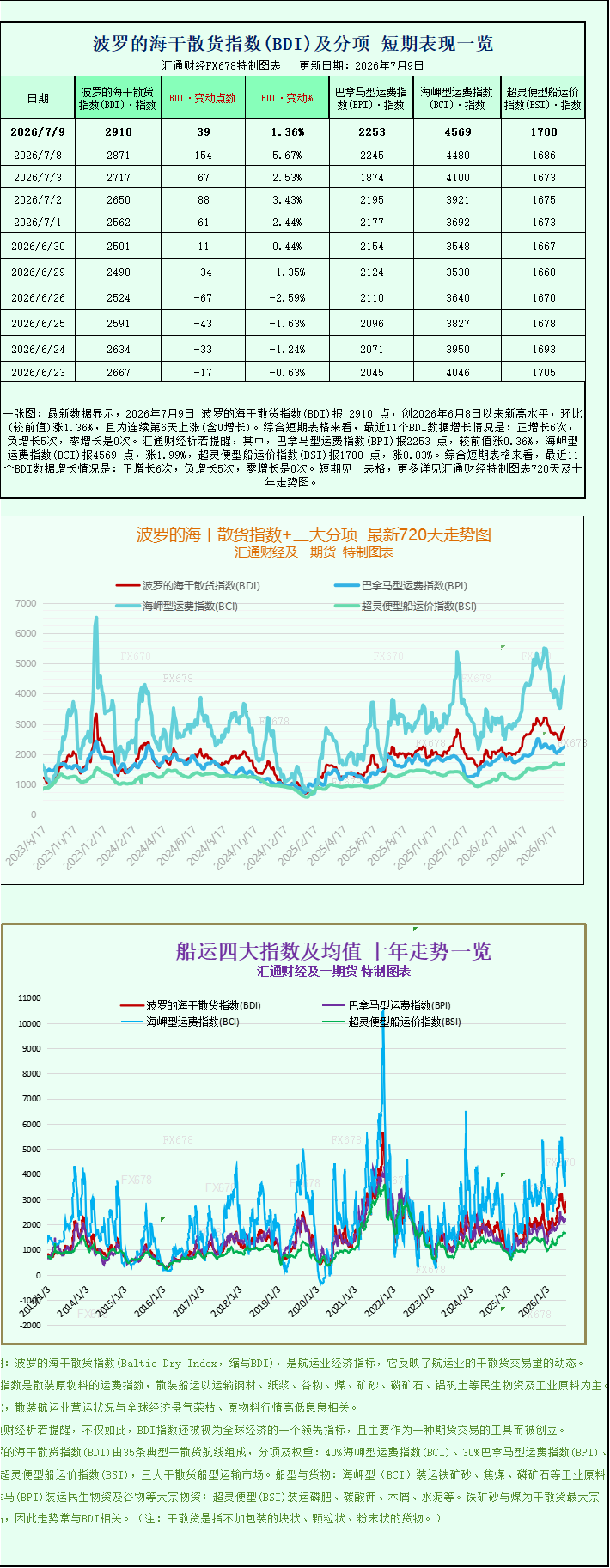

The latest data shows that the Baltic Dry Index (BDI) reached 2910 points on July 9, 2026, a new high since June 8, 2026, up 1.36% month-on-month, marking the sixth consecutive day of increase (including zero growth). Looking at the short-term charts, the recent 11 BDI data points show: 6 positive increases, 5 negative increases, and 0 zero increases. Specifically, the Panamax Freight Index (BPI) was 2253 points, up 0.36% from the previous value; the Capesize Freight Index (BCI) was 4569 points, up 1.99%; and the Supramax Freight Index (BSI) was 1700 points, up 0.83%. For detailed 720-day and 10-year trend charts of the Baltic Dry Index and its three main sub-indices, please refer to the specially designed charts.

The international dry bulk shipping market has recently seen a comprehensive recovery, with freight rates for all vessel types rising simultaneously, driving a sustained increase in core industry benchmark indices. On Thursday, the Baltic Dry Index (BDI) saw a significant rise, with both the overall index and the indices for each vessel type closing higher. The core BDI successfully reached a new monthly high since June 8, indicating a continued recovery in the short-term dry bulk shipping market and a phased improvement in the market's supply and demand dynamics.

Data shows that the Baltic Dry Index (BDI), which tracks freight rates for the three major dry bulk carrier types—Capesize, Panamax, and Supramax—rose 39 points, or 1.4%, to close at 2910 points, its highest level in nearly a month. This increase was not driven by a single vessel type, but rather by a coordinated strengthening across the entire sector. Freight rates for large, medium, and small dry bulk carriers all climbed, completely reversing the previous pattern of localized market fluctuations and divergent price movements, clearly indicating an overall recovery in the industry.

As the largest vessel type in terms of tonnage and with the highest weighting in the index, Capesize vessels saw the most significant gains in this round of increases, becoming the core driving force behind the market's rise. The Capesize index surged 89 points, a 2% increase, closing at 4569 points, also a one-month high. Corresponding market revenue data shows that Capesize vessels primarily engaged in the transportation of ultra-large industrial raw materials such as iron ore and coal (150,000 tons) saw an average daily revenue increase of $801, with the latest daily revenue reaching $37,931, indicating a steady rise in profitability.

The rise in Capesize freight rates is closely related to the dynamics of the global iron ore trade. Currently, the international iron ore market is exhibiting range-bound trading, with a complex interplay of bullish and bearish factors. On one hand, a strike by some BHP Billiton iron ore workers has raised concerns about disruptions to mine production and shipping, potentially leading to a short-term tightening of global iron ore supply and benefiting demand for ocean shipping. On the other hand, as a core global iron ore consumer, China is currently in its traditional off-season, with weak demand for steel from end-users. This has offset some of the positive supply-side expectations, preventing iron ore prices from rising unilaterally and instead maintaining a range-bound pattern, thus allowing Capesize freight rates to rise at a steady pace.

The medium-sized vessel market also maintained a steady upward trend, supporting the overall market index's stable rise. Panamax vessels, primarily engaged in the transportation of 60,000 to 70,000-ton bulk cargo such as coal and grain, saw a slight recovery in the market that day. The Panamax index rose 8 points, or 0.4%, to close at 2253 points. The corresponding average daily revenue for Panamax vessels increased by $67, reaching $20,276. Compared to larger vessel types, the increase in Panamax freight rates was relatively moderate, mainly due to the steady release of global demand for grain and industrial coal, and the steady replenishment demand in Europe and the United States supporting route freight rates, resulting in an overall stable and positive trend.

The small dry bulk shipping sector also rose in tandem, indicating a broad-based market upturn. The Supramax index rose 14 points, or 0.8%, to close at 1700. These vessels are primarily suited for short-haul, small-volume bulk cargo transportation, covering regional trade and raw material turnover. The increase in freight rates reflects the increased activity in global regional commodity trade, the continued expansion of market demand recovery, and the comprehensive foundation for a rebound in the dry bulk shipping market.

From an industry fundamentals perspective, the recent collective rise in dry bulk indices is the result of a combination of short-term demand recovery and improved medium- to long-term shipping capacity. Currently, the global dry bulk fleet's order book is at a multi-year low, with limited new capacity deployment, resulting in a tight overall market supply and providing solid support for rising freight rates. Furthermore, short-term global restocking of industrial raw materials and accelerated energy and food trade have further stimulated shipping market demand, driving a synchronized recovery in freight rates across all vessel types.

Industry analysts indicate that the Baltic Dry Index (BDI), a core leading indicator of global commodity trade and shipping activity, has reached a new monthly high, suggesting a continued recovery in global physical trade demand. Future market trends will continue to focus on iron ore supply disruptions, the pace of recovery in Chinese end-user demand, and the global flow of commodity trade. If demand continues to recover, coupled with a persistently tight shipping capacity, dry bulk freight rates are expected to maintain a high level of fluctuation.

The international dry bulk shipping market has recently seen a comprehensive recovery, with freight rates for all vessel types rising simultaneously, driving a sustained increase in core industry benchmark indices. On Thursday, the Baltic Dry Index (BDI) saw a significant rise, with both the overall index and the indices for each vessel type closing higher. The core BDI successfully reached a new monthly high since June 8, indicating a continued recovery in the short-term dry bulk shipping market and a phased improvement in the market's supply and demand dynamics.

Data shows that the Baltic Dry Index (BDI), which tracks freight rates for the three major dry bulk carrier types—Capesize, Panamax, and Supramax—rose 39 points, or 1.4%, to close at 2910 points, its highest level in nearly a month. This increase was not driven by a single vessel type, but rather by a coordinated strengthening across the entire sector. Freight rates for large, medium, and small dry bulk carriers all climbed, completely reversing the previous pattern of localized market fluctuations and divergent price movements, clearly indicating an overall recovery in the industry.

As the largest vessel type in terms of tonnage and with the highest weighting in the index, Capesize vessels saw the most significant gains in this round of increases, becoming the core driving force behind the market's rise. The Capesize index surged 89 points, a 2% increase, closing at 4569 points, also a one-month high. Corresponding market revenue data shows that Capesize vessels primarily engaged in the transportation of ultra-large industrial raw materials such as iron ore and coal (150,000 tons) saw an average daily revenue increase of $801, with the latest daily revenue reaching $37,931, indicating a steady rise in profitability.

The rise in Capesize freight rates is closely related to the dynamics of the global iron ore trade. Currently, the international iron ore market is exhibiting range-bound trading, with a complex interplay of bullish and bearish factors. On one hand, a strike by some BHP Billiton iron ore workers has raised concerns about disruptions to mine production and shipping, potentially leading to a short-term tightening of global iron ore supply and benefiting demand for ocean shipping. On the other hand, as a core global iron ore consumer, China is currently in its traditional off-season, with weak demand for steel from end-users. This has offset some of the positive supply-side expectations, preventing iron ore prices from rising unilaterally and instead maintaining a range-bound pattern, thus allowing Capesize freight rates to rise at a steady pace.

The medium-sized vessel market also maintained a steady upward trend, supporting the overall market index's stable rise. Panamax vessels, primarily engaged in the transportation of 60,000 to 70,000-ton bulk cargo such as coal and grain, saw a slight recovery in the market that day. The Panamax index rose 8 points, or 0.4%, to close at 2253 points. The corresponding average daily revenue for Panamax vessels increased by $67, reaching $20,276. Compared to larger vessel types, the increase in Panamax freight rates was relatively moderate, mainly due to the steady release of global demand for grain and industrial coal, and the steady replenishment demand in Europe and the United States supporting route freight rates, resulting in an overall stable and positive trend.

The small dry bulk shipping sector also rose in tandem, indicating a broad-based market upturn. The Supramax index rose 14 points, or 0.8%, to close at 1700. These vessels are primarily suited for short-haul, small-volume bulk cargo transportation, covering regional trade and raw material turnover. The increase in freight rates reflects the increased activity in global regional commodity trade, the continued expansion of market demand recovery, and the comprehensive foundation for a rebound in the dry bulk shipping market.

From an industry fundamentals perspective, the recent collective rise in dry bulk indices is the result of a combination of short-term demand recovery and improved medium- to long-term shipping capacity. Currently, the global dry bulk fleet's order book is at a multi-year low, with limited new capacity deployment, resulting in a tight overall market supply and providing solid support for rising freight rates. Furthermore, short-term global restocking of industrial raw materials and accelerated energy and food trade have further stimulated shipping market demand, driving a synchronized recovery in freight rates across all vessel types.

Industry analysts indicate that the Baltic Dry Index (BDI), a core leading indicator of global commodity trade and shipping activity, has reached a new monthly high, suggesting a continued recovery in global physical trade demand. Future market trends will continue to focus on iron ore supply disruptions, the pace of recovery in Chinese end-user demand, and the global flow of commodity trade. If demand continues to recover, coupled with a persistently tight shipping capacity, dry bulk freight rates are expected to maintain a high level of fluctuation.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.