From the micro-level dilemmas of Türkiye's oil purchases to the macro-level pressure on gold prices, a closed loop has formed.

2026-07-10 21:59:19

In today's complex global macroeconomic landscape, the outbreak of the US-Iran geopolitical conflict did not follow the traditional script of "soaring commodity prices and stagflation in the US economy".

On the contrary, the current financial market is witnessing a double-rising variation of "high nominal interest rates and high real interest rates," which is interwoven with expected inflation slowdown, the return of global safe-haven capital, and the generational technological revolution.

To unravel this complex logical puzzle, we need to examine the Federal Reserve's policy orientation from the "heads" of the global macro-level, and also from the "tails" of the micro-level, such as "Turkey buying oil," to see how the gears of the global dollar cycle turn.

From a short-term macroeconomic perspective, the current sustained rise and high level of nominal interest rates in the United States is facing a delicate economic environment: because key shipping lanes such as the Strait of Hormuz remain open despite the conflict, the fuse for global energy supply has not been fully lit, and oil prices have instead fluctuated and fallen from their highs. This phenomenon has directly led to a slowdown in market expectations for long-term inflation.

According to the Fisher equation in classic macroeconomics, the final equation is: nominal interest rate equals real interest rate minus inflation expectations.

When the Federal Reserve keeps nominal interest rates firmly at high levels in order to consolidate its anti-inflation efforts, the decline in long-term inflation expectations means that the current high interest rates and the fact that future inflation will not eat up too much interest income actually lead to a rise in real interest rates along with inflation expectations.

This misalignment between high nominal interest rates and falling inflation has led to a continuous rise in real interest rates for the real economy. It is this mechanism that has tightened global monetary policy at its very foundation.

This involves two factors that result in excessively high real interest rates. One is the excessive demand for funds caused by AI, which leads to a shortage of funds and higher prices. The other is the excessive government investment, which reduces the amount of money available for private investment.

In the supply and demand landscape of the loanable funds market, the persistently high real interest rates are supported by both the supply and demand sides:

Supply side (government deficit and crowding-out effect): The continued geopolitical tensions force the U.S. government to maintain high fiscal spending for defense, security and geopolitical competition.

This "big fiscal" model has greatly depleted national savings. The government, as a huge "money-sucking black hole" in the market, has continuously issued more national debt, creating a classic "crowding-out effect" on private investment and pushing up real interest rates from the supply side.

On the demand side (the productivity wave of the AI technological revolution): Unlike traditional economic recessions, the current real economy is undergoing a cross-generational technological revolution led by artificial intelligence (AI). Even in the face of such high financing costs, global tech giants are still engaging in massive capital expenditures (Capex) to secure future industry dominance. This extremely strong demand for real-economy loans and investments has become a rigid barrier preventing real interest rates from declining.

However, the reason why the US government's massive debt issuance did not cause the US Treasury market to collapse, but instead supported the dominance of the US dollar, lies in a brilliant "capital relay" within the global risk-averse model. We can understand this global capital repatriation paradigm through a typical micro-level perspective—Turkey's dilemma during the crisis.

When geopolitical conflicts escalate and uncertainty increases sharply, the micro-behavior of countries like Turkey, which lack core resources and whose currency (lira) faces significant devaluation risks, becomes part of the global financial machine.

The driving force behind the strengthening of the US dollar: Turkey must pay in US dollars, an international hard currency, to purchase oil, a rigid production factor, while oil-producing countries like Saudi Arabia will never accept the lira, which carries a high risk of devaluation. The actions of Turkey and other countries in selling their own currencies and frantically buying US dollars in the international foreign exchange market are a microcosm of the spontaneous behavior of countless risk-averse entities around the world.

This global, rigid demand meant that the dollar did not weaken during the crisis; instead, its purchasing power increased significantly, further strengthening the dollar's upward trend.

Rigid support for US Treasury yields (funding relay): In order to obtain urgently needed US dollar cash to pay Saudi Arabia, Türkiye had to put its holdings of US Treasury assets up for sale.

This sell-off would theoretically drive up interest rates. However, geopolitical conflicts have also triggered a global "risk-averse storm," with European funds and Asian billionaires snapping up dollars and searching for safe havens around the world. They immediately rushed to buy newly issued US Treasury bonds that were being offered at discounts and offering extremely high yields.

Subsequently, Saudi Arabia earned a huge amount of petrodollars from Turkey. In order to preserve the value of its assets, these dollars eventually flowed back into the US system by purchasing US Treasury bonds or depositing them in US banks.

It is this closed loop of "Türkiye selling US Treasury bonds for US dollars → European/Saudi capital taking over US Treasury bonds and flowing back to the United States" that perfectly resolves the pressure of the US government issuing large amounts of debt.

The continuous influx of global capital has created a strong, rigid demand for US Treasury bonds, ultimately supporting the maintenance of a relatively high and highly flexible real interest rate in the United States.

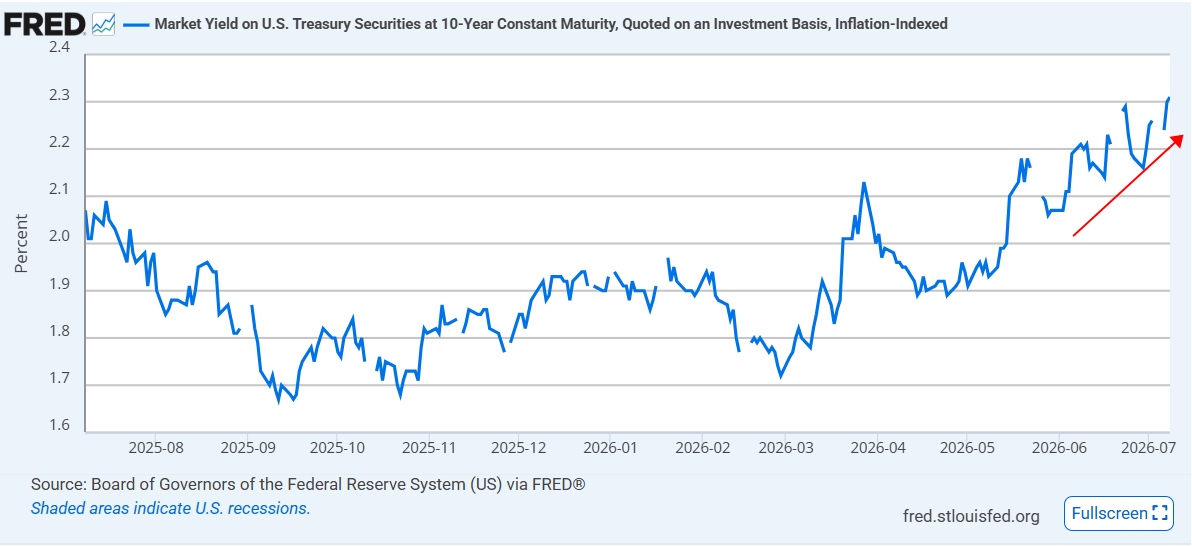

When all the above logical chains are seamlessly interwoven, the endpoint of the macroeconomic deduction inevitably points to gold, a traditional global safe-haven asset.

(Daily chart of real interest rate trends, source: Federal Reserve Bank of New York)

In traditional, fragmented understanding, geopolitical conflicts are often seen as catalysts for soaring gold prices. However, under the sophisticated paradigm of the global dollar cycle, this aura surrounding gold is being severely suppressed by high real interest rates.

As a "zero-interest asset" that does not generate any interest, the opportunity cost of holding gold is the real interest rate in the market. Currently, driven by factors such as "slowing forward inflation, government deficit squeeze, strong demand for AI investment," and "Turkish-style micro-level safe-haven capital repatriation," the real yield (real interest rate) of risk-free US Treasury bonds has climbed to a remarkable high.

This means that the opportunity cost for investors to hold gold to hedge against geopolitical risks has become extremely high. Compared to non-interest-bearing gold, "high real interest rate dollar assets," which are frantically bought up by global safe-haven funds and petrodollars, obviously offer a more attractive risk-free real return.

Therefore, under the dual pressure of a strengthening US dollar and a rigid increase in real interest rates, the attractiveness of gold has been systematically weakened, and its price will inevitably be subject to strong fluctuations and technical suppression at the macro level.

(Spot gold daily chart, source: FX678)

At 21:55 Beijing time, spot gold is currently trading at $4,100 per ounce.

On the contrary, the current financial market is witnessing a double-rising variation of "high nominal interest rates and high real interest rates," which is interwoven with expected inflation slowdown, the return of global safe-haven capital, and the generational technological revolution.

To unravel this complex logical puzzle, we need to examine the Federal Reserve's policy orientation from the "heads" of the global macro-level, and also from the "tails" of the micro-level, such as "Turkey buying oil," to see how the gears of the global dollar cycle turn.

The misalignment between nominal interest rates and slowing inflation: rising real interest rates due to the Fisher effect

From a short-term macroeconomic perspective, the current sustained rise and high level of nominal interest rates in the United States is facing a delicate economic environment: because key shipping lanes such as the Strait of Hormuz remain open despite the conflict, the fuse for global energy supply has not been fully lit, and oil prices have instead fluctuated and fallen from their highs. This phenomenon has directly led to a slowdown in market expectations for long-term inflation.

According to the Fisher equation in classic macroeconomics, the final equation is: nominal interest rate equals real interest rate minus inflation expectations.

When the Federal Reserve keeps nominal interest rates firmly at high levels in order to consolidate its anti-inflation efforts, the decline in long-term inflation expectations means that the current high interest rates and the fact that future inflation will not eat up too much interest income actually lead to a rise in real interest rates along with inflation expectations.

This misalignment between high nominal interest rates and falling inflation has led to a continuous rise in real interest rates for the real economy. It is this mechanism that has tightened global monetary policy at its very foundation.

Macroeconomic rigidity on both the supply and demand sides: the resonance between crowding-out effect and AI capital expenditure

This involves two factors that result in excessively high real interest rates. One is the excessive demand for funds caused by AI, which leads to a shortage of funds and higher prices. The other is the excessive government investment, which reduces the amount of money available for private investment.

In the supply and demand landscape of the loanable funds market, the persistently high real interest rates are supported by both the supply and demand sides:

Supply side (government deficit and crowding-out effect): The continued geopolitical tensions force the U.S. government to maintain high fiscal spending for defense, security and geopolitical competition.

This "big fiscal" model has greatly depleted national savings. The government, as a huge "money-sucking black hole" in the market, has continuously issued more national debt, creating a classic "crowding-out effect" on private investment and pushing up real interest rates from the supply side.

On the demand side (the productivity wave of the AI technological revolution): Unlike traditional economic recessions, the current real economy is undergoing a cross-generational technological revolution led by artificial intelligence (AI). Even in the face of such high financing costs, global tech giants are still engaging in massive capital expenditures (Capex) to secure future industry dominance. This extremely strong demand for real-economy loans and investments has become a rigid barrier preventing real interest rates from declining.

The meshing of microscopic gears: The capital repatriation paradigm triggered by Turkey's oil purchases

However, the reason why the US government's massive debt issuance did not cause the US Treasury market to collapse, but instead supported the dominance of the US dollar, lies in a brilliant "capital relay" within the global risk-averse model. We can understand this global capital repatriation paradigm through a typical micro-level perspective—Turkey's dilemma during the crisis.

When geopolitical conflicts escalate and uncertainty increases sharply, the micro-behavior of countries like Turkey, which lack core resources and whose currency (lira) faces significant devaluation risks, becomes part of the global financial machine.

The driving force behind the strengthening of the US dollar: Turkey must pay in US dollars, an international hard currency, to purchase oil, a rigid production factor, while oil-producing countries like Saudi Arabia will never accept the lira, which carries a high risk of devaluation. The actions of Turkey and other countries in selling their own currencies and frantically buying US dollars in the international foreign exchange market are a microcosm of the spontaneous behavior of countless risk-averse entities around the world.

This global, rigid demand meant that the dollar did not weaken during the crisis; instead, its purchasing power increased significantly, further strengthening the dollar's upward trend.

Rigid support for US Treasury yields (funding relay): In order to obtain urgently needed US dollar cash to pay Saudi Arabia, Türkiye had to put its holdings of US Treasury assets up for sale.

This sell-off would theoretically drive up interest rates. However, geopolitical conflicts have also triggered a global "risk-averse storm," with European funds and Asian billionaires snapping up dollars and searching for safe havens around the world. They immediately rushed to buy newly issued US Treasury bonds that were being offered at discounts and offering extremely high yields.

Subsequently, Saudi Arabia earned a huge amount of petrodollars from Turkey. In order to preserve the value of its assets, these dollars eventually flowed back into the US system by purchasing US Treasury bonds or depositing them in US banks.

It is this closed loop of "Türkiye selling US Treasury bonds for US dollars → European/Saudi capital taking over US Treasury bonds and flowing back to the United States" that perfectly resolves the pressure of the US government issuing large amounts of debt.

The continuous influx of global capital has created a strong, rigid demand for US Treasury bonds, ultimately supporting the maintenance of a relatively high and highly flexible real interest rate in the United States.

The logical conclusion: High real interest rates inevitably put downward pressure on the value of gold.

When all the above logical chains are seamlessly interwoven, the endpoint of the macroeconomic deduction inevitably points to gold, a traditional global safe-haven asset.

(Daily chart of real interest rate trends, source: Federal Reserve Bank of New York)

In traditional, fragmented understanding, geopolitical conflicts are often seen as catalysts for soaring gold prices. However, under the sophisticated paradigm of the global dollar cycle, this aura surrounding gold is being severely suppressed by high real interest rates.

As a "zero-interest asset" that does not generate any interest, the opportunity cost of holding gold is the real interest rate in the market. Currently, driven by factors such as "slowing forward inflation, government deficit squeeze, strong demand for AI investment," and "Turkish-style micro-level safe-haven capital repatriation," the real yield (real interest rate) of risk-free US Treasury bonds has climbed to a remarkable high.

This means that the opportunity cost for investors to hold gold to hedge against geopolitical risks has become extremely high. Compared to non-interest-bearing gold, "high real interest rate dollar assets," which are frantically bought up by global safe-haven funds and petrodollars, obviously offer a more attractive risk-free real return.

Therefore, under the dual pressure of a strengthening US dollar and a rigid increase in real interest rates, the attractiveness of gold has been systematically weakened, and its price will inevitably be subject to strong fluctuations and technical suppression at the macro level.

(Spot gold daily chart, source: FX678)

At 21:55 Beijing time, spot gold is currently trading at $4,100 per ounce.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.