Research and gold-buying behavior corroborate each other, suggesting that continued gold hoarding by central banks worldwide will be the main theme for gold in the second half of the year.

2026-07-13 10:24:01

Actions speak louder than words; this classic adage will be the core theme of the gold market in the second half of 2026. Two authoritative central bank surveys have already signaled a strong willingness to increase holdings, and subsequent data on actual gold purchases by central banks around the world further confirm the firm long-term bullish stance of sovereign institutions on gold.

During the June gold price correction, major Asian countries and key gold-purchasing central banks, such as Poland, increased their buying efforts against the trend, contrasting sharply with the behavior of retail investors and speculative funds selling gold to chase technology stocks. Central bank gold purchases are not a short-term gamble on interest rates and inflation, but rather a strategic move towards global monetary diversification over decades. The decline in gold prices actually provides an excellent entry window for official reserves, and ordinary investors should pay attention to this long-term value signal.

Two surveys conducted last month among global reserve management institutions gave a clear and consistent bullish signal. The World Gold Council survey showed that a record 45% of central banks plan to expand their gold reserves in the next 12 months; the Official Monetary and Financial Institutions Forum's annual survey also indicated that, against the backdrop of a fragmented global financial system and countries accelerating the diversification of their reserves, gold remains the top choice among reserve assets.

Surveys can only reflect policy planning; subsequent official reserve data will confirm market expectations through actual financial actions. According to the World Gold Council, global central bank official gold reserves increased by a net 41 tons in May, continuing the strong trend of sovereign gold purchases that has persisted for many years. Entering June, as gold prices continued to adjust, major global official gold buyers not only slowed their pace but also seized the opportunity of lower prices to expand their purchases. Central banks of major Asian countries increased their gold holdings by 15 tons that month, achieving 20 consecutive months of continuous purchases and marking the largest monthly increase this year. Poland's gold purchases were even more aggressive; the National Bank of Poland purchased a total of 82 tons of gold in the first half of 2026, and its governor, Adam Glapiński, publicly stated that the central bank is actively taking advantage of the decline in gold prices to expand its reserves.

The central bank's contrarian move to increase its gold holdings stands in stark contrast to the trading choices of ordinary market participants. Short-term speculative funds are withdrawing from the gold market and shifting towards artificial intelligence-related stocks with potential for upward movement. Coupled with rising market expectations of interest rate hikes, the opportunity cost of holding gold continues to increase, leading many retail investors to reduce their gold holdings. On one hand, official institutions are buying more as prices fall; on the other hand, private funds are exiting the market during corrections. These two drastically different operational approaches essentially reflect a difference between short-term trading mentality and long-term strategic allocation.

Central banks around the world purchase gold not because they closely monitor monthly inflation data or the pace of short-term interest rate adjustments by the Federal Reserve, nor do they intend to chase short-term price fluctuations. All gold purchases serve long-term monetary security planning. Reserve managers assess global financial risks over decades, building balance sheets capable of withstanding geopolitical conflicts, sharp exchange rate fluctuations, and changes in multipolar monetary systems. Gold's unique monetary attributes are the core support: ample liquidity, global recognition, no counterparty risk, and its value is not affected by the fiscal or monetary policies of a single country, effectively hedging against various systemic financial risks.

Because gold possesses unique long-term safe-haven reserve value, the recent temporary weakening of gold prices has not diminished the enthusiasm of official institutions to purchase gold. On the contrary, the price correction has reduced the cost of reserve allocation, making it a rare window of opportunity for central banks around the world to increase their holdings.

Retail investors often focus on short-term interest rate fluctuations that cause market ups and downs, easily overlooking the underlying value of gold in the context of the restructuring of the global monetary landscape.

Amidst frequent global geopolitical risks, weakening US dollar credibility, and the diversification of reserves by many countries, the long-term cycle of central banks accumulating gold is unlikely to end in the short term. For ordinary investors, it is crucial to move beyond short-term trading fluctuations, recognize the long-term allocation signals continuously released by official institutions worldwide, and rationally assess gold's medium- to long-term value as a store of value and a hedge against risk.

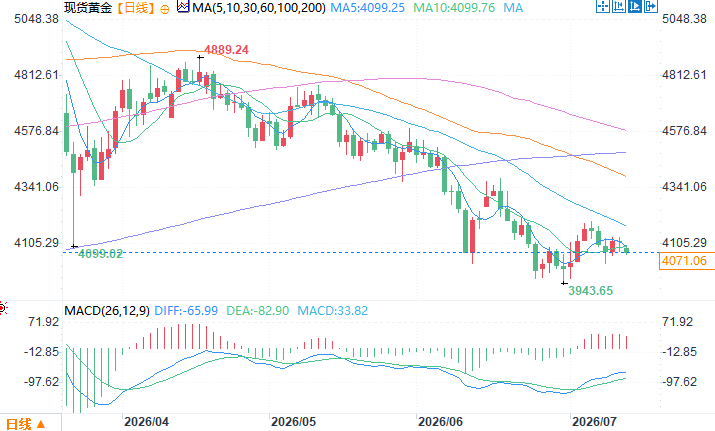

Spot gold daily chart source: EasyForex

At 10:22 AM Beijing time on July 13, spot gold was trading at $4072.06 per ounce.

During the June gold price correction, major Asian countries and key gold-purchasing central banks, such as Poland, increased their buying efforts against the trend, contrasting sharply with the behavior of retail investors and speculative funds selling gold to chase technology stocks. Central bank gold purchases are not a short-term gamble on interest rates and inflation, but rather a strategic move towards global monetary diversification over decades. The decline in gold prices actually provides an excellent entry window for official reserves, and ordinary investors should pay attention to this long-term value signal.

Research suggests increased holdings, which are confirmed by actual gold purchase data.

Two surveys conducted last month among global reserve management institutions gave a clear and consistent bullish signal. The World Gold Council survey showed that a record 45% of central banks plan to expand their gold reserves in the next 12 months; the Official Monetary and Financial Institutions Forum's annual survey also indicated that, against the backdrop of a fragmented global financial system and countries accelerating the diversification of their reserves, gold remains the top choice among reserve assets.

Surveys can only reflect policy planning; subsequent official reserve data will confirm market expectations through actual financial actions. According to the World Gold Council, global central bank official gold reserves increased by a net 41 tons in May, continuing the strong trend of sovereign gold purchases that has persisted for many years. Entering June, as gold prices continued to adjust, major global official gold buyers not only slowed their pace but also seized the opportunity of lower prices to expand their purchases. Central banks of major Asian countries increased their gold holdings by 15 tons that month, achieving 20 consecutive months of continuous purchases and marking the largest monthly increase this year. Poland's gold purchases were even more aggressive; the National Bank of Poland purchased a total of 82 tons of gold in the first half of 2026, and its governor, Adam Glapiński, publicly stated that the central bank is actively taking advantage of the decline in gold prices to expand its reserves.

Institutional and retail investors are diverging in their market trends, and their investment logic is completely different.

The central bank's contrarian move to increase its gold holdings stands in stark contrast to the trading choices of ordinary market participants. Short-term speculative funds are withdrawing from the gold market and shifting towards artificial intelligence-related stocks with potential for upward movement. Coupled with rising market expectations of interest rate hikes, the opportunity cost of holding gold continues to increase, leading many retail investors to reduce their gold holdings. On one hand, official institutions are buying more as prices fall; on the other hand, private funds are exiting the market during corrections. These two drastically different operational approaches essentially reflect a difference between short-term trading mentality and long-term strategic allocation.

Central banks around the world purchase gold not because they closely monitor monthly inflation data or the pace of short-term interest rate adjustments by the Federal Reserve, nor do they intend to chase short-term price fluctuations. All gold purchases serve long-term monetary security planning. Reserve managers assess global financial risks over decades, building balance sheets capable of withstanding geopolitical conflicts, sharp exchange rate fluctuations, and changes in multipolar monetary systems. Gold's unique monetary attributes are the core support: ample liquidity, global recognition, no counterparty risk, and its value is not affected by the fiscal or monetary policies of a single country, effectively hedging against various systemic financial risks.

Gold price pullback does not change its long-term investment value; investors should closely follow the central bank's long-term strategy.

Because gold possesses unique long-term safe-haven reserve value, the recent temporary weakening of gold prices has not diminished the enthusiasm of official institutions to purchase gold. On the contrary, the price correction has reduced the cost of reserve allocation, making it a rare window of opportunity for central banks around the world to increase their holdings.

Retail investors often focus on short-term interest rate fluctuations that cause market ups and downs, easily overlooking the underlying value of gold in the context of the restructuring of the global monetary landscape.

Amidst frequent global geopolitical risks, weakening US dollar credibility, and the diversification of reserves by many countries, the long-term cycle of central banks accumulating gold is unlikely to end in the short term. For ordinary investors, it is crucial to move beyond short-term trading fluctuations, recognize the long-term allocation signals continuously released by official institutions worldwide, and rationally assess gold's medium- to long-term value as a store of value and a hedge against risk.

Spot gold daily chart source: EasyForex

At 10:22 AM Beijing time on July 13, spot gold was trading at $4072.06 per ounce.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.