A chart shows that Capesize freight rates have weakened significantly, and the Baltic Dry Index has ended its highs and begun to decline.

2026-07-15 23:20:12

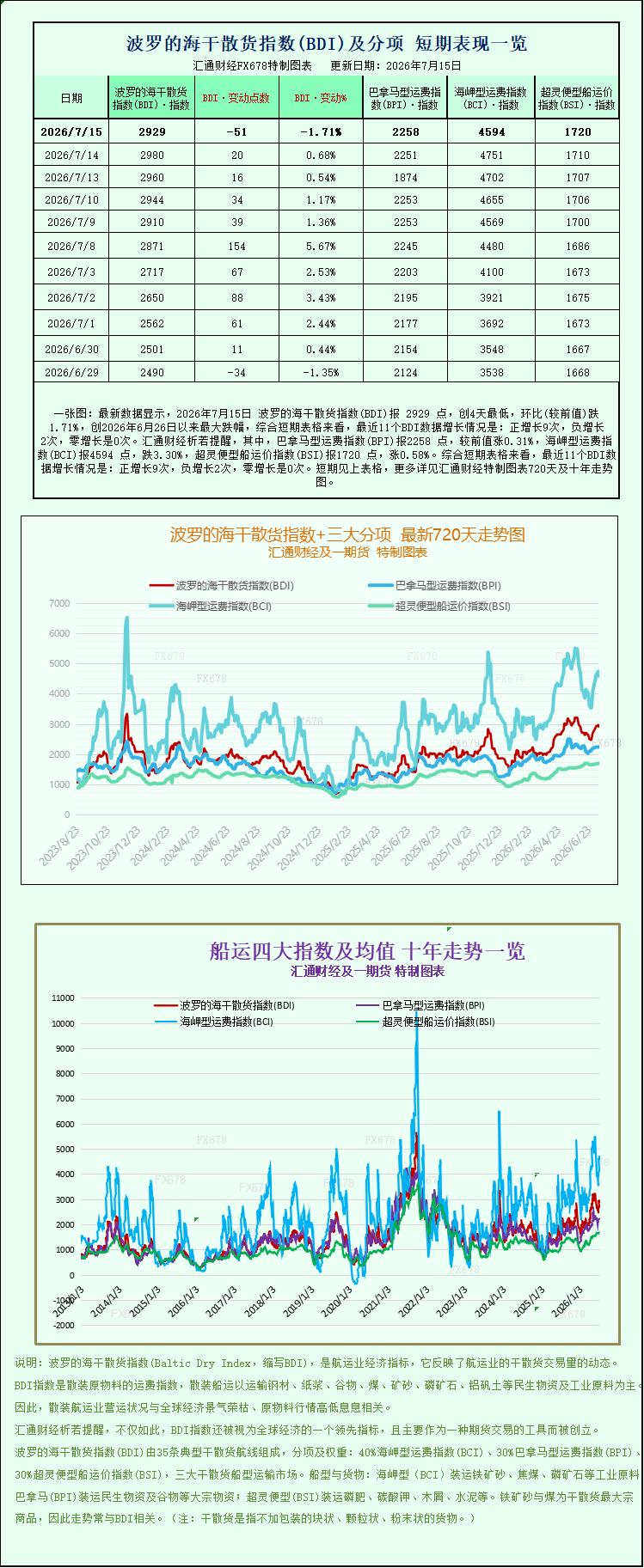

Latest data shows that on July 15, 2026, the Baltic Dry Index (BDI) was 2929 points, a four-day low, down 1.71% from the previous day, the largest drop since June 26, 2026. Looking at the short-term charts, the BDI has seen positive growth 9 times, negative growth 2 times, and zero growth in the last 11 BDI readings. Specifically, the Panamax Freight Index (BPI) was 2258 points, up 0.31% from the previous day; the Capesize Freight Index (BCI) was 4594 points, down 3.30%; and the Supramax Freight Index (BSI) was 1720 points, up 0.58%. For detailed 720-day and 10-year charts of the Baltic Dry Index and its three main sub-indices, please refer to the charts provided by FX678.  The international dry bulk shipping market, which had been rising steadily recently, experienced a temporary correction. The Baltic Dry Index (BDI), after several days of gains and reaching a more than one-month high, fell significantly on Wednesday, July 15th. This decline was primarily driven by a sharp weakening of Capesize (Good Hope) bulk carrier freight rates. The divergence in freight rates between large and small vessel types was significant, reflecting a structural adjustment in the global supply and demand pattern for bulk commodities. As a core indicator of the global dry bulk shipping market, the Baltic Dry Index tracks freight rates for the three major dry bulk carrier types: Capesize, Panamax, and Supramax. It directly reflects changes in global demand and capacity for bulk raw materials such as ore, coal, and grain. Data shows that the index fell sharply by 51 points, a drop of 1.7%, closing at 2929 points, completely ending the previous continuous upward trend and marking a slowdown from the highs since early June. This signifies a formal slowdown in the short-term upward momentum of the dry bulk shipping market. The core drag on this index correction was the large Capesize bulk carrier market. This vessel type primarily carries ultra-large freight orders of 150,000 tons and above, and is the core vessel type for ocean shipping of industrial bulk raw materials such as iron ore, thermal coal, and metallurgical coal. It is highly correlated with the global steel and energy supply chains, making it extremely sensitive to freight rate fluctuations. Data shows that the Capesize vessel-specific index (.BACI) plummeted 157 points that day, a drop of 3.3%, closing at 4594 points, a decline far exceeding the market average. The corresponding core vessel type's profitability also came under pressure. The average daily operating income of mainstream 150,000-ton Capesize vessels (.BATCA) fell sharply by $1420, with the latest daily earnings dropping to $38,163, resulting in a significant contraction in the profit margins of large dry bulk carrier owners. Industry analysts point out that the plunge in Capesize freight rates is not accidental, but rather a result of a short-term supply-demand mismatch and weakening downstream demand. In the early part of June and early July, a surge in global steel mill restocking and overseas energy procurement demand led to a sharp increase in cargo volume on ocean-going mining and coal shipping routes, pushing Capesize freight rates to a monthly high. However, by mid-July, market demand cooled rapidly. On the one hand, the domestic steel market entered its traditional off-season, with weak end-user construction demand, high steel mill inventories, and pressure on profitability, prompting a proactive reduction in iron ore import restocking. This resulted in a significant decrease in ocean-going orders from major Australian and Brazilian ore suppliers in the Pacific. On the other hand, industrial production in Europe and the United States slowed, leading to insufficient growth in ocean-going demand for metallurgical and thermal coal, and a shortage of cargo volume on long-haul routes. This resulted in a relative oversupply of large vessels, causing freight rates to fall accordingly. Simultaneously, the previous high prices stimulated the return of some idle large vessels to the market, further easing short-term supply and exacerbating downward pressure on freight rates. In stark contrast to the sluggish performance of large Capesize vessels, the medium and small bulk carrier market continued its steady upward trend, exhibiting a clear structural differentiation. The Panamax market saw a slight recovery, with the Panamax Index (.BPNI) rising 7 points, or 0.3%, to close at 2258 points. The average daily earnings of mainstream Panamax vessels increased by $65 to $20,325. Panamax vessels primarily carry 60,000 to 70,000 tons of cargo, mainly transporting commodities such as coal, grain, and fertilizer. Their routes are mainly short- and medium-haul within the region, making them less affected by fluctuations in global industrial bulk demand. Analysts from international multimodal transport companies stated in their latest weekly report that the Panamax bulk carrier market remained stable and resilient last week, with regional shipping activities being the core support. Stable regional trade demand for grain and industrial raw materials in the Asia-Pacific and Atlantic regions continued to release rigid cargo volumes, supporting a steady recovery in vessel prices. However, limited growth in overall global bulk trade prevented sustained upward momentum, failing to establish a definitive upward trend, and instead exhibiting a moderate upward trend with a steady upward bias. The small Supramax market performed the best, showing an independent upward trend. The Supramax vessel index rose 10 points, or 0.6%, to close at 1720 points, a near four-year high since August 2022. Supramax vessels, with their flexible and adaptable hulls, can navigate between small and medium-sized ports, primarily handling regional general cargo, grain, and small-batch energy and raw material transport orders. Benefiting from increased global regional trade activity and continued release of freight demand at small and medium-sized ports, market demand remains strong. Coupled with the relatively rigid deployment of small vessel capacity, the supply-demand balance is tight, driving freight rates to new highs. Overall, the dry bulk shipping market has moved beyond the previous broad-based price increases and entered a phase of structural differentiation. Large industrial raw material transport vessels have seen freight rates retreat from their highs due to weakening short-term demand in the steel and energy supply chains, cooling market activity. Meanwhile, small and medium-sized vessels engaged in short- and medium-haul, regional transport have maintained resilient price increases thanks to stable demand from consumer and regional industrial trade. Industry insiders indicate that future market trends will continue to depend on the pace of global industrial recovery, steel mill restocking cycles, and the release of peak season demand in the grain trade. In the short term, Capesize freight rates may continue to fluctuate with a slightly downward trend, while the strong performance of the small and medium-sized vessel market is expected to continue. The overall index will exhibit characteristics of consolidation and structural differentiation.

The international dry bulk shipping market, which had been rising steadily recently, experienced a temporary correction. The Baltic Dry Index (BDI), after several days of gains and reaching a more than one-month high, fell significantly on Wednesday, July 15th. This decline was primarily driven by a sharp weakening of Capesize (Good Hope) bulk carrier freight rates. The divergence in freight rates between large and small vessel types was significant, reflecting a structural adjustment in the global supply and demand pattern for bulk commodities. As a core indicator of the global dry bulk shipping market, the Baltic Dry Index tracks freight rates for the three major dry bulk carrier types: Capesize, Panamax, and Supramax. It directly reflects changes in global demand and capacity for bulk raw materials such as ore, coal, and grain. Data shows that the index fell sharply by 51 points, a drop of 1.7%, closing at 2929 points, completely ending the previous continuous upward trend and marking a slowdown from the highs since early June. This signifies a formal slowdown in the short-term upward momentum of the dry bulk shipping market. The core drag on this index correction was the large Capesize bulk carrier market. This vessel type primarily carries ultra-large freight orders of 150,000 tons and above, and is the core vessel type for ocean shipping of industrial bulk raw materials such as iron ore, thermal coal, and metallurgical coal. It is highly correlated with the global steel and energy supply chains, making it extremely sensitive to freight rate fluctuations. Data shows that the Capesize vessel-specific index (.BACI) plummeted 157 points that day, a drop of 3.3%, closing at 4594 points, a decline far exceeding the market average. The corresponding core vessel type's profitability also came under pressure. The average daily operating income of mainstream 150,000-ton Capesize vessels (.BATCA) fell sharply by $1420, with the latest daily earnings dropping to $38,163, resulting in a significant contraction in the profit margins of large dry bulk carrier owners. Industry analysts point out that the plunge in Capesize freight rates is not accidental, but rather a result of a short-term supply-demand mismatch and weakening downstream demand. In the early part of June and early July, a surge in global steel mill restocking and overseas energy procurement demand led to a sharp increase in cargo volume on ocean-going mining and coal shipping routes, pushing Capesize freight rates to a monthly high. However, by mid-July, market demand cooled rapidly. On the one hand, the domestic steel market entered its traditional off-season, with weak end-user construction demand, high steel mill inventories, and pressure on profitability, prompting a proactive reduction in iron ore import restocking. This resulted in a significant decrease in ocean-going orders from major Australian and Brazilian ore suppliers in the Pacific. On the other hand, industrial production in Europe and the United States slowed, leading to insufficient growth in ocean-going demand for metallurgical and thermal coal, and a shortage of cargo volume on long-haul routes. This resulted in a relative oversupply of large vessels, causing freight rates to fall accordingly. Simultaneously, the previous high prices stimulated the return of some idle large vessels to the market, further easing short-term supply and exacerbating downward pressure on freight rates. In stark contrast to the sluggish performance of large Capesize vessels, the medium and small bulk carrier market continued its steady upward trend, exhibiting a clear structural differentiation. The Panamax market saw a slight recovery, with the Panamax Index (.BPNI) rising 7 points, or 0.3%, to close at 2258 points. The average daily earnings of mainstream Panamax vessels increased by $65 to $20,325. Panamax vessels primarily carry 60,000 to 70,000 tons of cargo, mainly transporting commodities such as coal, grain, and fertilizer. Their routes are mainly short- and medium-haul within the region, making them less affected by fluctuations in global industrial bulk demand. Analysts from international multimodal transport companies stated in their latest weekly report that the Panamax bulk carrier market remained stable and resilient last week, with regional shipping activities being the core support. Stable regional trade demand for grain and industrial raw materials in the Asia-Pacific and Atlantic regions continued to release rigid cargo volumes, supporting a steady recovery in vessel prices. However, limited growth in overall global bulk trade prevented sustained upward momentum, failing to establish a definitive upward trend, and instead exhibiting a moderate upward trend with a steady upward bias. The small Supramax market performed the best, showing an independent upward trend. The Supramax vessel index rose 10 points, or 0.6%, to close at 1720 points, a near four-year high since August 2022. Supramax vessels, with their flexible and adaptable hulls, can navigate between small and medium-sized ports, primarily handling regional general cargo, grain, and small-batch energy and raw material transport orders. Benefiting from increased global regional trade activity and continued release of freight demand at small and medium-sized ports, market demand remains strong. Coupled with the relatively rigid deployment of small vessel capacity, the supply-demand balance is tight, driving freight rates to new highs. Overall, the dry bulk shipping market has moved beyond the previous broad-based price increases and entered a phase of structural differentiation. Large industrial raw material transport vessels have seen freight rates retreat from their highs due to weakening short-term demand in the steel and energy supply chains, cooling market activity. Meanwhile, small and medium-sized vessels engaged in short- and medium-haul, regional transport have maintained resilient price increases thanks to stable demand from consumer and regional industrial trade. Industry insiders indicate that future market trends will continue to depend on the pace of global industrial recovery, steel mill restocking cycles, and the release of peak season demand in the grain trade. In the short term, Capesize freight rates may continue to fluctuate with a slightly downward trend, while the strong performance of the small and medium-sized vessel market is expected to continue. The overall index will exhibit characteristics of consolidation and structural differentiation.

The international dry bulk shipping market, which had been rising steadily recently, experienced a temporary correction. The Baltic Dry Index (BDI), after several days of gains and reaching a more than one-month high, fell significantly on Wednesday, July 15th. This decline was primarily driven by a sharp weakening of Capesize (Good Hope) bulk carrier freight rates. The divergence in freight rates between large and small vessel types was significant, reflecting a structural adjustment in the global supply and demand pattern for bulk commodities. As a core indicator of the global dry bulk shipping market, the Baltic Dry Index tracks freight rates for the three major dry bulk carrier types: Capesize, Panamax, and Supramax. It directly reflects changes in global demand and capacity for bulk raw materials such as ore, coal, and grain. Data shows that the index fell sharply by 51 points, a drop of 1.7%, closing at 2929 points, completely ending the previous continuous upward trend and marking a slowdown from the highs since early June. This signifies a formal slowdown in the short-term upward momentum of the dry bulk shipping market. The core drag on this index correction was the large Capesize bulk carrier market. This vessel type primarily carries ultra-large freight orders of 150,000 tons and above, and is the core vessel type for ocean shipping of industrial bulk raw materials such as iron ore, thermal coal, and metallurgical coal. It is highly correlated with the global steel and energy supply chains, making it extremely sensitive to freight rate fluctuations. Data shows that the Capesize vessel-specific index (.BACI) plummeted 157 points that day, a drop of 3.3%, closing at 4594 points, a decline far exceeding the market average. The corresponding core vessel type's profitability also came under pressure. The average daily operating income of mainstream 150,000-ton Capesize vessels (.BATCA) fell sharply by $1420, with the latest daily earnings dropping to $38,163, resulting in a significant contraction in the profit margins of large dry bulk carrier owners. Industry analysts point out that the plunge in Capesize freight rates is not accidental, but rather a result of a short-term supply-demand mismatch and weakening downstream demand. In the early part of June and early July, a surge in global steel mill restocking and overseas energy procurement demand led to a sharp increase in cargo volume on ocean-going mining and coal shipping routes, pushing Capesize freight rates to a monthly high. However, by mid-July, market demand cooled rapidly. On the one hand, the domestic steel market entered its traditional off-season, with weak end-user construction demand, high steel mill inventories, and pressure on profitability, prompting a proactive reduction in iron ore import restocking. This resulted in a significant decrease in ocean-going orders from major Australian and Brazilian ore suppliers in the Pacific. On the other hand, industrial production in Europe and the United States slowed, leading to insufficient growth in ocean-going demand for metallurgical and thermal coal, and a shortage of cargo volume on long-haul routes. This resulted in a relative oversupply of large vessels, causing freight rates to fall accordingly. Simultaneously, the previous high prices stimulated the return of some idle large vessels to the market, further easing short-term supply and exacerbating downward pressure on freight rates. In stark contrast to the sluggish performance of large Capesize vessels, the medium and small bulk carrier market continued its steady upward trend, exhibiting a clear structural differentiation. The Panamax market saw a slight recovery, with the Panamax Index (.BPNI) rising 7 points, or 0.3%, to close at 2258 points. The average daily earnings of mainstream Panamax vessels increased by $65 to $20,325. Panamax vessels primarily carry 60,000 to 70,000 tons of cargo, mainly transporting commodities such as coal, grain, and fertilizer. Their routes are mainly short- and medium-haul within the region, making them less affected by fluctuations in global industrial bulk demand. Analysts from international multimodal transport companies stated in their latest weekly report that the Panamax bulk carrier market remained stable and resilient last week, with regional shipping activities being the core support. Stable regional trade demand for grain and industrial raw materials in the Asia-Pacific and Atlantic regions continued to release rigid cargo volumes, supporting a steady recovery in vessel prices. However, limited growth in overall global bulk trade prevented sustained upward momentum, failing to establish a definitive upward trend, and instead exhibiting a moderate upward trend with a steady upward bias. The small Supramax market performed the best, showing an independent upward trend. The Supramax vessel index rose 10 points, or 0.6%, to close at 1720 points, a near four-year high since August 2022. Supramax vessels, with their flexible and adaptable hulls, can navigate between small and medium-sized ports, primarily handling regional general cargo, grain, and small-batch energy and raw material transport orders. Benefiting from increased global regional trade activity and continued release of freight demand at small and medium-sized ports, market demand remains strong. Coupled with the relatively rigid deployment of small vessel capacity, the supply-demand balance is tight, driving freight rates to new highs. Overall, the dry bulk shipping market has moved beyond the previous broad-based price increases and entered a phase of structural differentiation. Large industrial raw material transport vessels have seen freight rates retreat from their highs due to weakening short-term demand in the steel and energy supply chains, cooling market activity. Meanwhile, small and medium-sized vessels engaged in short- and medium-haul, regional transport have maintained resilient price increases thanks to stable demand from consumer and regional industrial trade. Industry insiders indicate that future market trends will continue to depend on the pace of global industrial recovery, steel mill restocking cycles, and the release of peak season demand in the grain trade. In the short term, Capesize freight rates may continue to fluctuate with a slightly downward trend, while the strong performance of the small and medium-sized vessel market is expected to continue. The overall index will exhibit characteristics of consolidation and structural differentiation.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.