A chart shows that a sharp decline in Capesize freight rates dragged down the Baltic Dry Index, resulting in a significant weekly drop.

2026-07-18 00:30:15

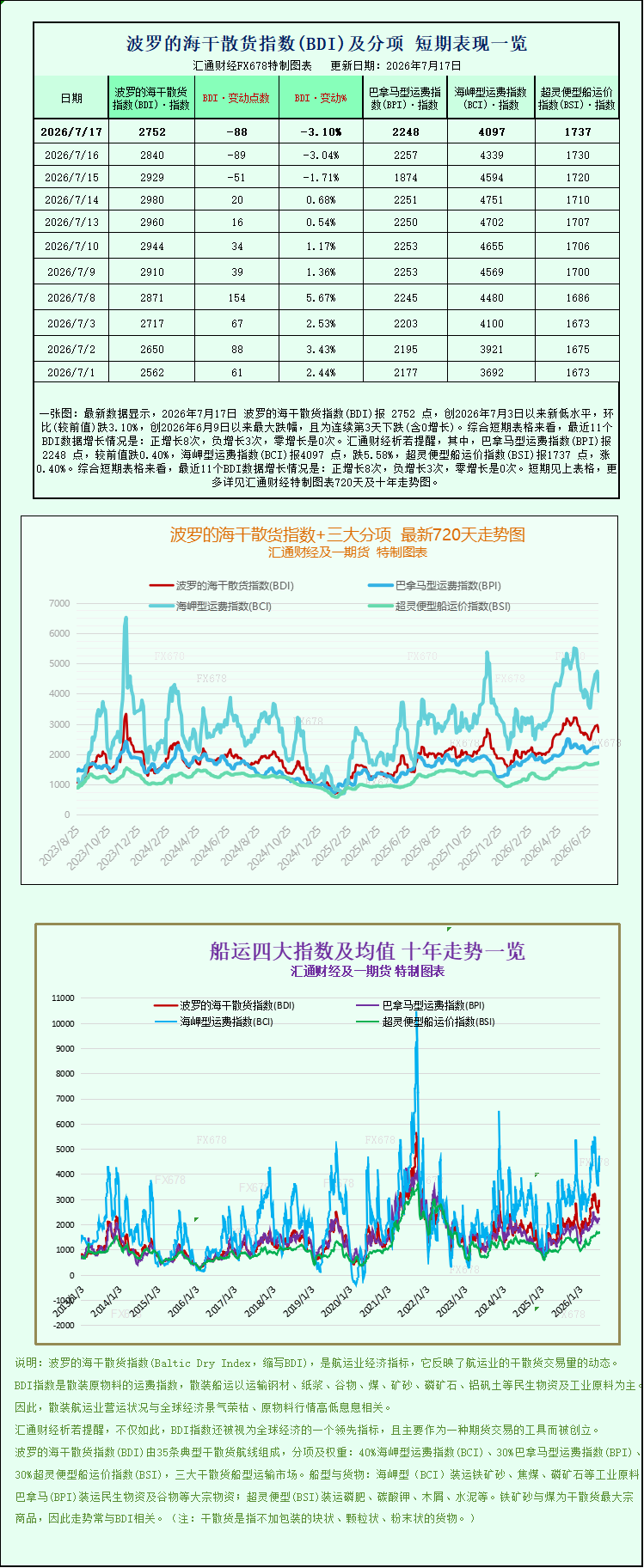

Latest data shows that the Baltic Dry Index (BDI) closed at 2752 points on July 17, 2026, a new low since July 3, 2026, down 3.10% month-on-month, the largest drop since June 9, 2026, and marking the third consecutive day of decline (including zero growth). Looking at the short-term charts, the recent 11 BDI data points show: 8 positive increases, 3 negative increases, and 0 zero increases. Specifically, the Panamax Freight Index (BPI) closed at 2248 points, down 0.40% from the previous value; the Capesize Freight Index (BCI) closed at 4097 points, down 5.58%; and the Supramax Freight Index (BSI) closed at 1737 points, up 0.40%. For detailed 720-day and 10-year trend charts of the Baltic Dry Index and its three main sub-indices, please refer to the charts specially created by FX678. As a key indicator of the global dry bulk shipping market, the Baltic Dry Index (BDI) continued its downward pressure this week, falling sharply again on Friday to record a substantial weekly decline. The primary drag on the index was the significant weakness in Capesize (Good Hope) vessel freight rates. Although the iron ore futures market showed a slight recovery, it failed to reverse the overall weak trend in the shipping market. The mismatch between supply and demand and the cooling of short-term freight demand were the main drivers of this round of freight rate declines.  Data shows that the Baltic Dry Index (BDI), which covers freight rates for the three major dry bulk shipping types—Capesize, Panamax, and Supramax—plunged 88 points on the day, a single-day drop of 3.1%, ultimately closing at 2752 points, its lowest level in nearly two weeks since July 3. Looking at the weekly performance, the index has fallen by more than 6% this week, ending its previous period of fluctuating upward movement and reflecting a significant decline in the global dry bulk shipping market. As an important leading indicator of global commodity shipping activity and international trade activity, the sharp weekly decline in the BDI also reflects a temporary contraction in short-term global demand for industrial raw materials. The core drag on this round of index decline came from the large Capesize vessel market. This type of vessel mainly carries ultra-heavy industrial raw materials such as iron ore and coal, and is a core weighted segment of the dry bulk market; its freight rate fluctuations have the most significant impact on the overall index. This week, the Capesize index fell far more sharply than the broader market, plunging 242 points in a single day, a drop of 5.6%, closing at 4097 points. The cumulative weekly decline approached 12%, making it the biggest culprit dragging down the Baltic Dry Index (BDI). Specific profit data more directly reflects the weakness in the Capesize market. The average daily earnings of Capesize vessels primarily engaged in the transportation of 150,000-ton bulk industrial raw materials declined sharply, with average daily revenue decreasing by $2,196 to a recent low of $33,653. Industry analysts point out that the sharp drop in Capesize freight rates is mainly due to a cooling demand for iron ore and coal ocean shipping in the short term. Recently, the pace of global steel mill operations has slowed, coupled with the end of the previous concentrated commodity transportation window, resulting in a supply-demand imbalance of "more ships than cargo." At the same time, the continuous addition of new dry bulk shipping capacity this year has further suppressed the upside potential for large vessel freight rates, leading to this round of deep correction in large vessel freight rates. It is worth noting that the shipping market and the commodity futures market are showing a clear divergence. While ocean freight rates continued to weaken, domestic iron ore futures prices bucked the trend and are poised for a second consecutive week of gains. This rebound in iron ore prices is mainly attributed to the continued decline in domestic port inventories and a temporary recovery in downstream steel market demand, which boosted restocking demand and provided strong support for prices. However, from a medium-term perspective, global iron ore supply remains ample, with stable shipments from major overseas mines. This ample supply significantly limits the upside potential for prices, resulting in a limited recovery in the futures market and failing to drive a sustained recovery in ocean shipping demand. Compared to the sharp decline in Capesize vessels, the medium-sized Panamax vessel market has shown relative resilience, with more moderate fluctuations. Data shows that the Panamax index fell slightly by 9 points on the day, a daily drop of only 0.4%, closing at 2248 points. The cumulative decline for the week was only 0.2%, maintaining a relatively stable trend. This vessel type mainly carries 60,000 to 70,000 tons of bulk commodities such as coal and grain, catering to global food trade and regional energy transportation needs, making it relatively more resilient in the market. The average daily revenue of its vessels fell slightly by $80, with the latest average at $20,236. Profitability remained stable without a significant decline, highlighting the structural differences in demand across different cargo types. Regarding smaller vessels, the Supramax index also continued its weak and volatile pattern this week. As the most numerous and flexible vessel type in the dry bulk market, Supramax vessels cover diverse niche bulk cargo transportation scenarios and are less affected by the cyclical fluctuations in large industrial raw material transportation. However, given the overall weak market sentiment and ample supply across the industry, they failed to break away from independent trends, with freight rates following the broader market downward pressure, further reinforcing the overall weak market trend. In summary, the recent weekly decline in the Baltic Dry Index is a result of both structural demand decline and ample industry supply. In the short term, the weakening demand for industrial bulk raw material transportation corresponding to Capesize vessels is the direct cause of the index's decline. In the medium to long term, the concentrated delivery of new global dry bulk vessels in 2026 will perpetuate the overall market overcapacity, exerting sustained downward pressure on freight rates. Market analysts believe that whether the Baltic Dry Index (BDI) can stabilize and rebound depends primarily on the pace of resumption of work and production in domestic infrastructure and manufacturing, as well as the strength of the recovery in end-user transportation demand for iron ore and coal. If downstream demand continues to recover, the shipping market is expected to gradually stop falling and stabilize.

Data shows that the Baltic Dry Index (BDI), which covers freight rates for the three major dry bulk shipping types—Capesize, Panamax, and Supramax—plunged 88 points on the day, a single-day drop of 3.1%, ultimately closing at 2752 points, its lowest level in nearly two weeks since July 3. Looking at the weekly performance, the index has fallen by more than 6% this week, ending its previous period of fluctuating upward movement and reflecting a significant decline in the global dry bulk shipping market. As an important leading indicator of global commodity shipping activity and international trade activity, the sharp weekly decline in the BDI also reflects a temporary contraction in short-term global demand for industrial raw materials. The core drag on this round of index decline came from the large Capesize vessel market. This type of vessel mainly carries ultra-heavy industrial raw materials such as iron ore and coal, and is a core weighted segment of the dry bulk market; its freight rate fluctuations have the most significant impact on the overall index. This week, the Capesize index fell far more sharply than the broader market, plunging 242 points in a single day, a drop of 5.6%, closing at 4097 points. The cumulative weekly decline approached 12%, making it the biggest culprit dragging down the Baltic Dry Index (BDI). Specific profit data more directly reflects the weakness in the Capesize market. The average daily earnings of Capesize vessels primarily engaged in the transportation of 150,000-ton bulk industrial raw materials declined sharply, with average daily revenue decreasing by $2,196 to a recent low of $33,653. Industry analysts point out that the sharp drop in Capesize freight rates is mainly due to a cooling demand for iron ore and coal ocean shipping in the short term. Recently, the pace of global steel mill operations has slowed, coupled with the end of the previous concentrated commodity transportation window, resulting in a supply-demand imbalance of "more ships than cargo." At the same time, the continuous addition of new dry bulk shipping capacity this year has further suppressed the upside potential for large vessel freight rates, leading to this round of deep correction in large vessel freight rates. It is worth noting that the shipping market and the commodity futures market are showing a clear divergence. While ocean freight rates continued to weaken, domestic iron ore futures prices bucked the trend and are poised for a second consecutive week of gains. This rebound in iron ore prices is mainly attributed to the continued decline in domestic port inventories and a temporary recovery in downstream steel market demand, which boosted restocking demand and provided strong support for prices. However, from a medium-term perspective, global iron ore supply remains ample, with stable shipments from major overseas mines. This ample supply significantly limits the upside potential for prices, resulting in a limited recovery in the futures market and failing to drive a sustained recovery in ocean shipping demand. Compared to the sharp decline in Capesize vessels, the medium-sized Panamax vessel market has shown relative resilience, with more moderate fluctuations. Data shows that the Panamax index fell slightly by 9 points on the day, a daily drop of only 0.4%, closing at 2248 points. The cumulative decline for the week was only 0.2%, maintaining a relatively stable trend. This vessel type mainly carries 60,000 to 70,000 tons of bulk commodities such as coal and grain, catering to global food trade and regional energy transportation needs, making it relatively more resilient in the market. The average daily revenue of its vessels fell slightly by $80, with the latest average at $20,236. Profitability remained stable without a significant decline, highlighting the structural differences in demand across different cargo types. Regarding smaller vessels, the Supramax index also continued its weak and volatile pattern this week. As the most numerous and flexible vessel type in the dry bulk market, Supramax vessels cover diverse niche bulk cargo transportation scenarios and are less affected by the cyclical fluctuations in large industrial raw material transportation. However, given the overall weak market sentiment and ample supply across the industry, they failed to break away from independent trends, with freight rates following the broader market downward pressure, further reinforcing the overall weak market trend. In summary, the recent weekly decline in the Baltic Dry Index is a result of both structural demand decline and ample industry supply. In the short term, the weakening demand for industrial bulk raw material transportation corresponding to Capesize vessels is the direct cause of the index's decline. In the medium to long term, the concentrated delivery of new global dry bulk vessels in 2026 will perpetuate the overall market overcapacity, exerting sustained downward pressure on freight rates. Market analysts believe that whether the Baltic Dry Index (BDI) can stabilize and rebound depends primarily on the pace of resumption of work and production in domestic infrastructure and manufacturing, as well as the strength of the recovery in end-user transportation demand for iron ore and coal. If downstream demand continues to recover, the shipping market is expected to gradually stop falling and stabilize.

Data shows that the Baltic Dry Index (BDI), which covers freight rates for the three major dry bulk shipping types—Capesize, Panamax, and Supramax—plunged 88 points on the day, a single-day drop of 3.1%, ultimately closing at 2752 points, its lowest level in nearly two weeks since July 3. Looking at the weekly performance, the index has fallen by more than 6% this week, ending its previous period of fluctuating upward movement and reflecting a significant decline in the global dry bulk shipping market. As an important leading indicator of global commodity shipping activity and international trade activity, the sharp weekly decline in the BDI also reflects a temporary contraction in short-term global demand for industrial raw materials. The core drag on this round of index decline came from the large Capesize vessel market. This type of vessel mainly carries ultra-heavy industrial raw materials such as iron ore and coal, and is a core weighted segment of the dry bulk market; its freight rate fluctuations have the most significant impact on the overall index. This week, the Capesize index fell far more sharply than the broader market, plunging 242 points in a single day, a drop of 5.6%, closing at 4097 points. The cumulative weekly decline approached 12%, making it the biggest culprit dragging down the Baltic Dry Index (BDI). Specific profit data more directly reflects the weakness in the Capesize market. The average daily earnings of Capesize vessels primarily engaged in the transportation of 150,000-ton bulk industrial raw materials declined sharply, with average daily revenue decreasing by $2,196 to a recent low of $33,653. Industry analysts point out that the sharp drop in Capesize freight rates is mainly due to a cooling demand for iron ore and coal ocean shipping in the short term. Recently, the pace of global steel mill operations has slowed, coupled with the end of the previous concentrated commodity transportation window, resulting in a supply-demand imbalance of "more ships than cargo." At the same time, the continuous addition of new dry bulk shipping capacity this year has further suppressed the upside potential for large vessel freight rates, leading to this round of deep correction in large vessel freight rates. It is worth noting that the shipping market and the commodity futures market are showing a clear divergence. While ocean freight rates continued to weaken, domestic iron ore futures prices bucked the trend and are poised for a second consecutive week of gains. This rebound in iron ore prices is mainly attributed to the continued decline in domestic port inventories and a temporary recovery in downstream steel market demand, which boosted restocking demand and provided strong support for prices. However, from a medium-term perspective, global iron ore supply remains ample, with stable shipments from major overseas mines. This ample supply significantly limits the upside potential for prices, resulting in a limited recovery in the futures market and failing to drive a sustained recovery in ocean shipping demand. Compared to the sharp decline in Capesize vessels, the medium-sized Panamax vessel market has shown relative resilience, with more moderate fluctuations. Data shows that the Panamax index fell slightly by 9 points on the day, a daily drop of only 0.4%, closing at 2248 points. The cumulative decline for the week was only 0.2%, maintaining a relatively stable trend. This vessel type mainly carries 60,000 to 70,000 tons of bulk commodities such as coal and grain, catering to global food trade and regional energy transportation needs, making it relatively more resilient in the market. The average daily revenue of its vessels fell slightly by $80, with the latest average at $20,236. Profitability remained stable without a significant decline, highlighting the structural differences in demand across different cargo types. Regarding smaller vessels, the Supramax index also continued its weak and volatile pattern this week. As the most numerous and flexible vessel type in the dry bulk market, Supramax vessels cover diverse niche bulk cargo transportation scenarios and are less affected by the cyclical fluctuations in large industrial raw material transportation. However, given the overall weak market sentiment and ample supply across the industry, they failed to break away from independent trends, with freight rates following the broader market downward pressure, further reinforcing the overall weak market trend. In summary, the recent weekly decline in the Baltic Dry Index is a result of both structural demand decline and ample industry supply. In the short term, the weakening demand for industrial bulk raw material transportation corresponding to Capesize vessels is the direct cause of the index's decline. In the medium to long term, the concentrated delivery of new global dry bulk vessels in 2026 will perpetuate the overall market overcapacity, exerting sustained downward pressure on freight rates. Market analysts believe that whether the Baltic Dry Index (BDI) can stabilize and rebound depends primarily on the pace of resumption of work and production in domestic infrastructure and manufacturing, as well as the strength of the recovery in end-user transportation demand for iron ore and coal. If downstream demand continues to recover, the shipping market is expected to gradually stop falling and stabilize.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.