With negotiations stalled and military standoff escalating, crude oil prices continued their volatile upward trend.

2026-02-19 20:56:40

On Thursday (February 19), during the European trading session, the price of April West Texas Intermediate (WTI) crude oil futures continued to rise. It reached $66.11 per barrel, a gain of 1.63%. US and Iranian officials are attempting to resolve their differences after negotiations between the two countries over Iran's nuclear program stalled. While the second round of indirect talks held in Geneva, Switzerland on February 17 made some progress, reaching a preliminary consensus on "identifying common goals and related technical issues," core differences remain unresolved. Iran is expected to submit a more concrete proposal in the coming weeks. On February 18, local time, White House Press Secretary Caroline Levitt further stated that the US-Iran negotiations had "made some progress," but the two sides remain "far apart" on key issues. Trump will continue to assess the progress of the negotiations, and the US State Department has imposed visa restrictions on 18 Iranian officials and telecommunications industry leaders, further highlighting the confrontational situation between the two sides.

Meanwhile, military tensions in the Middle East continue to escalate. The United States is deploying a second carrier strike group from the Caribbean to the Middle East, including the USS Abraham Lincoln and the USS Gerald R. Ford, and has increased its deployment with advanced fighter jets such as F-22s and F-35s. It is understood that the US military has already deployed one carrier strike group in the Middle East, and the second carrier strike group is in the process of deployment. In addition, it has deployed more than ten other types of warships, hundreds of fighter jets, and multiple air defense systems, and has used more than 150 military transport aircraft to transport weapons, equipment, and ammunition to the Middle East. The Iranian Islamic Revolutionary Guard Corps Navy conducted live-fire exercises in the Strait of Hormuz from February 16 to 17, temporarily closing parts of the waterway for several hours, further exacerbating market concerns about shipping security.

As of 7 p.m. on February 19, the White House declined to comment on whether it would set a deadline for negotiations or consider military options. However, sources familiar with the matter revealed that the U.S. military was prepared to launch a military strike against Iran as early as this weekend. President Trump, however, had not yet made a final decision, having privately debated the pros and cons of military action and consulted advisors and allies on the best course of action. Israel has raised its national alert level across the board, preparing for the possibility of a breakdown in U.S.-Iran negotiations. Two Israeli sources revealed that due to indications of a possible joint attack against Iran in the coming days, Israel is accelerating its military preparations. Israeli Prime Minister Netanyahu has chaired several special security meetings this week to assess the Israeli military's combat readiness and the U.S.-Israeli coordination capabilities. The Israeli security cabinet meeting originally scheduled for February 19 has been urgently postponed to this Sunday (February 22), seen as a tactical adjustment in response to a contingency plan.

Furthermore, reports indicate that if the United States launches military action against Iran, it is likely to be a large-scale operation lasting several weeks, with coordinated strikes by the US and Israel. This would be far larger than the June 12th conflict of last year, posing a greater "existential threat" to Iran, further fueling market risk aversion. In addition, senior US officials stated that all US troops involved in the Middle East military buildup should be in place by mid-March. US Secretary of State Rubio will travel to Israel on February 28th to meet with Israeli Prime Minister Netanyahu to further coordinate positions on the Iranian issue.

The real risk lies in the Strait of Hormuz—the "throat" of the global energy supply chain.

The core concern in the crude oil market is that if Iran decides to disrupt shipping in the Strait of Hormuz, military action could directly lead to a disruption of crude oil supplies. According to ANZ analysts, approximately 20% of global oil consumption relies on this waterway; and the latest industry data shows that the strait handles about 21 million barrels of crude oil daily, accounting for 30% of global seaborne oil trade. Major oil-producing countries such as Saudi Arabia and the UAE rely on this passage for over 90% of their exports, and 45% to 80% of China, Japan, and the EU's imported oil also passes through this route. There is widespread market concern that if the US and Israel launch a joint attack on Iran, Iran is highly likely to retaliate with long-range missiles against Israel and may resort to extreme measures such as closing the Strait of Hormuz, which would severely damage global crude oil supplies.

It is worth noting that if passage through the Strait is blocked, existing alternative routes will be severely underutilized. Saudi Arabia's Petroline has a capacity of approximately 5 million barrels per day, and the UAE's Abu Dhabi oil pipeline has a capacity of 1.5 million barrels per day. The combined capacity of these land routes is less than half of the Strait's daily traffic, meaning that any disruption will directly impact the global supply balance. Data from energy consulting firms shows that Iran's recent military exercises alone have driven Brent crude oil prices up by about 4%, and if the Strait is blocked, the price increase will far exceed that level.

Wednesday's 4% surge was just the beginning; the risk of oil price volatility continues to rise.

Wednesday's 4% jump in the oil market was merely an initial reaction to escalating tensions. On February 18th local time, international oil prices had already risen significantly. By the close of trading that day, WTI crude oil futures for March delivery rose 4.59% to $65.19 per barrel, and Brent crude oil futures for April delivery rose 4.35% to $70.35 per barrel, confirming the strong support for oil prices from geopolitical risks. Market analysis indicates that if a conflict breaks out, oil prices could rise another 5%–10%; if Iran successfully blocks the Strait of Hormuz, oil prices could rise another 10%. Even if a ceasefire is reached, the shipping lanes will remain impassable for a long period due to debris and other obstructions, which is the core risk currently facing the market.

From a supply and demand perspective, the OPEC+ alliance's recent stance of maintaining production cuts has further supported oil prices. The eight OPEC+ countries have reached an agreement to maintain current oil production levels until March 2026, continuing the phased production cuts suspended since December 2025, and maintaining a voluntary production cut of 3.24 million barrels per day. Member countries are highly aligned on the "production cuts to stabilize prices" strategy. In January 2026, OPEC+ daily production decreased by 439,000 barrels month-on-month, far exceeding expectations. Meanwhile, unplanned supply disruptions in Kazakhstan, Venezuela, Iran, and other regions further compressed global supply redundancy. At the same time, the crude oil investment market is heating up. The latest circulating shares of a domestic ETF fund linked to oil and gas industry stocks are 1.859 billion units, with a circulating scale of 2.673 billion yuan, representing a more than ninefold increase this year, reflecting the continued rise in investor attention to the crude oil market.

The key issues that traders are currently most concerned about

Current news is generally positive for oil prices, but the extent of this positive impact depends on several key factors: how long the military action will last and whether it will become a large-scale operation lasting several weeks; which areas within Iran (military bases, oil facilities, nuclear facilities, etc.) the US will target; whether Iran can successfully blockade oil tanker traffic in the Strait of Hormuz, for how long the blockade will last, and whether it will retaliate against Israel with long-range missiles; whether Iran will retaliate against US military bases around the world, or even targets on the US mainland; whether the US-Iran negotiations can achieve a breakthrough on core differences, and whether the specific proposals submitted by Iran will be accepted by the US; in addition, whether Trump will ultimately authorize military action against Iran is also a key variable affecting oil price trends.

Historical experience warns that the impact of geopolitical conflicts on oil prices is persistent.

Looking back at the Iraq-Kuwait War of the 1990s, when Iraqi leader Saddam Hussein was attacked by the US military, he launched Scud missiles at Saudi Arabia and even set fire to domestic oil wells, causing a sharp short-term contraction in global crude oil supply and a temporary surge in oil prices. Currently, the market is concerned that if the conflict between the US and Iran escalates, Iran may resort to similar extreme measures, further exacerbating the risk of supply shortages. In particular, if the US and Israel launch a large-scale joint attack, Iran's retaliation could affect shipping in the Strait of Hormuz and surrounding oil production facilities, with an impact on global crude oil supply far exceeding expectations and with lasting effects.

Speculative funds exacerbate volatility, oil prices may see another 10%–20% increase.

The current crude oil market appears relatively calm, but the situation could change rapidly. Market analysts believe that if war breaks out, speculative funds will aggressively go long, forcing short sellers to liquidate their positions, potentially leading to a further 10%-20% increase in oil prices. Currently, the geopolitical risk premium has reached $5-8 per barrel, and if the military standoff does not ease in the short term, the risk premium still has room to rise. Meanwhile, the commodity market as a whole is performing strongly, with gold futures prices returning to the $5,000/ounce mark. As of 5 PM on February 19th, London spot gold closed at $5,015/ounce, a year-to-date increase of over 16%. The simultaneous rise in gold, silver, and crude oil reflects the coexistence of risk aversion and inflation expectations in the market, further driving speculative funds into the commodity market and indirectly exacerbating crude oil price volatility.

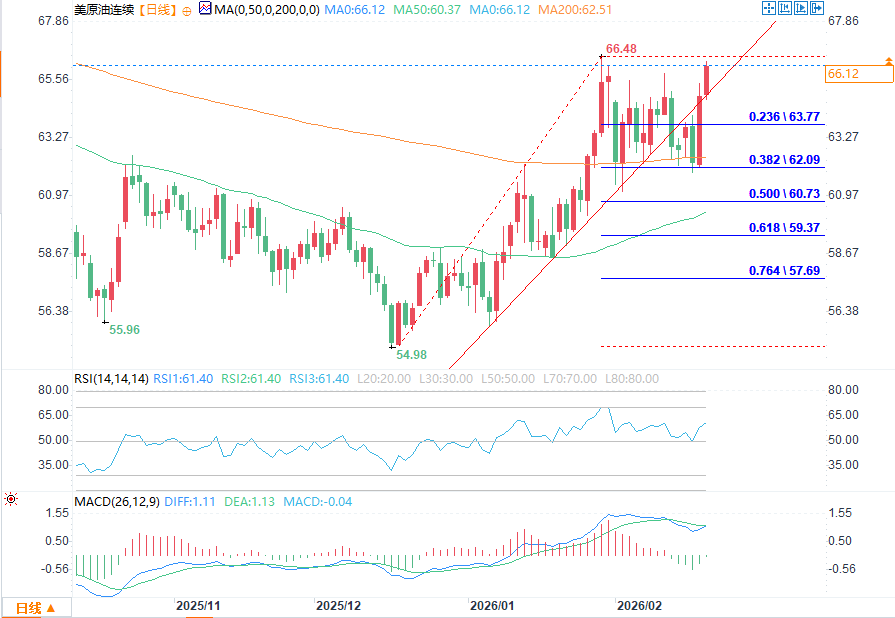

Technical Analysis: The market is driven by momentum and news, with the trading range widening.

(WTI crude oil daily chart source: FX678)

US crude oil rebounded from its low of $54.98 in January 2026, steadily rising along a clear red upward trend line. It has now broken through the previous densely traded area, showing a strong rebound from a technical perspective. Regarding the moving average system, the 50-day moving average ($60.37) and the 200-day moving average ($62.51) have both been firmly held by the price, and the short-term moving average has crossed above the long-term moving average, forming a bullish alignment and confirming a strengthening medium-term trend. As for oscillators, the RSI (14) is at 61.49, within the strong 50-70 range, indicating that bullish momentum remains, but it is approaching the overbought threshold, requiring caution regarding the risk of a short-term pullback. In the MACD indicator, both the DIFF and DEA are above the zero axis, and the red bars have narrowed slightly, suggesting that the upward momentum may slow down.

Key support levels below include: the red upward trend line at approximately $63.84, which is the core support for the recent rebound; a decisive break below this level could trigger a technical correction; the 200-day moving average at $62.51, a level with both psychological and technical significance; a breach of this level could lead to a test of the 50-day moving average at $60.37; and the 50% Fibonacci retracement level at $60.73, which resonates with the 50-day moving average and serves as a crucial defense line for the medium-term bulls. The upside target is the previous high of $66.48, which is the immediate resistance level for the current rebound; a break above $66.48 could lead to further gains towards $68.11 and $69.37.

Long-term outlook: Don't expect oil prices to stay above $100 for an extended period – global crude oil supply is ample.

It should be noted that global crude oil supply is currently ample, and only 20% of oil consumption relies on the Strait of Hormuz. Therefore, it is unnecessary to expect oil prices to remain above $90 or $100 per barrel in the long term. When the Russia-Ukraine conflict broke out in February 2022, crude oil futures surged to over $120 per barrel. Four years later, the conflict continues, and just a month ago, oil prices were only around $60 per barrel, nearly halved. This confirms that the support for oil prices from geopolitical conflicts is mostly temporary and unlikely to change the long-term supply and demand pattern.

From a fundamental perspective, the core focus should be on whether the Strait of Hormuz will be blocked and for how long, as this will determine how high oil prices can rise and how long they can maintain their current high levels. OPEC maintained its forecast in its latest monthly report that global oil demand will grow by 1.38 million barrels per day in 2026 and 1.34 million barrels per day in 2027, mainly supported by easing inflation, fiscal policy support, and improved trade. Meanwhile, the U.S. Energy Information Administration (EIA) estimates that China is continuously increasing its strategic reserves at a rate of approximately 1 million barrels per day, absorbing a significant portion of the global market's excess supply and alleviating concerns about oversupply to some extent. According to a comprehensive analysis of institutional views, oil prices will maintain a fluctuating upward trend in the short term, supported by geopolitical risks. However, in the long term, the global supply situation remains ample, and after a significant price increase, there is still room for a correction, and a sustained period above $100 per barrel is unlikely.

Meanwhile, military tensions in the Middle East continue to escalate. The United States is deploying a second carrier strike group from the Caribbean to the Middle East, including the USS Abraham Lincoln and the USS Gerald R. Ford, and has increased its deployment with advanced fighter jets such as F-22s and F-35s. It is understood that the US military has already deployed one carrier strike group in the Middle East, and the second carrier strike group is in the process of deployment. In addition, it has deployed more than ten other types of warships, hundreds of fighter jets, and multiple air defense systems, and has used more than 150 military transport aircraft to transport weapons, equipment, and ammunition to the Middle East. The Iranian Islamic Revolutionary Guard Corps Navy conducted live-fire exercises in the Strait of Hormuz from February 16 to 17, temporarily closing parts of the waterway for several hours, further exacerbating market concerns about shipping security.

As of 7 p.m. on February 19, the White House declined to comment on whether it would set a deadline for negotiations or consider military options. However, sources familiar with the matter revealed that the U.S. military was prepared to launch a military strike against Iran as early as this weekend. President Trump, however, had not yet made a final decision, having privately debated the pros and cons of military action and consulted advisors and allies on the best course of action. Israel has raised its national alert level across the board, preparing for the possibility of a breakdown in U.S.-Iran negotiations. Two Israeli sources revealed that due to indications of a possible joint attack against Iran in the coming days, Israel is accelerating its military preparations. Israeli Prime Minister Netanyahu has chaired several special security meetings this week to assess the Israeli military's combat readiness and the U.S.-Israeli coordination capabilities. The Israeli security cabinet meeting originally scheduled for February 19 has been urgently postponed to this Sunday (February 22), seen as a tactical adjustment in response to a contingency plan.

Furthermore, reports indicate that if the United States launches military action against Iran, it is likely to be a large-scale operation lasting several weeks, with coordinated strikes by the US and Israel. This would be far larger than the June 12th conflict of last year, posing a greater "existential threat" to Iran, further fueling market risk aversion. In addition, senior US officials stated that all US troops involved in the Middle East military buildup should be in place by mid-March. US Secretary of State Rubio will travel to Israel on February 28th to meet with Israeli Prime Minister Netanyahu to further coordinate positions on the Iranian issue.

The real risk lies in the Strait of Hormuz—the "throat" of the global energy supply chain.

The core concern in the crude oil market is that if Iran decides to disrupt shipping in the Strait of Hormuz, military action could directly lead to a disruption of crude oil supplies. According to ANZ analysts, approximately 20% of global oil consumption relies on this waterway; and the latest industry data shows that the strait handles about 21 million barrels of crude oil daily, accounting for 30% of global seaborne oil trade. Major oil-producing countries such as Saudi Arabia and the UAE rely on this passage for over 90% of their exports, and 45% to 80% of China, Japan, and the EU's imported oil also passes through this route. There is widespread market concern that if the US and Israel launch a joint attack on Iran, Iran is highly likely to retaliate with long-range missiles against Israel and may resort to extreme measures such as closing the Strait of Hormuz, which would severely damage global crude oil supplies.

It is worth noting that if passage through the Strait is blocked, existing alternative routes will be severely underutilized. Saudi Arabia's Petroline has a capacity of approximately 5 million barrels per day, and the UAE's Abu Dhabi oil pipeline has a capacity of 1.5 million barrels per day. The combined capacity of these land routes is less than half of the Strait's daily traffic, meaning that any disruption will directly impact the global supply balance. Data from energy consulting firms shows that Iran's recent military exercises alone have driven Brent crude oil prices up by about 4%, and if the Strait is blocked, the price increase will far exceed that level.

Wednesday's 4% surge was just the beginning; the risk of oil price volatility continues to rise.

Wednesday's 4% jump in the oil market was merely an initial reaction to escalating tensions. On February 18th local time, international oil prices had already risen significantly. By the close of trading that day, WTI crude oil futures for March delivery rose 4.59% to $65.19 per barrel, and Brent crude oil futures for April delivery rose 4.35% to $70.35 per barrel, confirming the strong support for oil prices from geopolitical risks. Market analysis indicates that if a conflict breaks out, oil prices could rise another 5%–10%; if Iran successfully blocks the Strait of Hormuz, oil prices could rise another 10%. Even if a ceasefire is reached, the shipping lanes will remain impassable for a long period due to debris and other obstructions, which is the core risk currently facing the market.

From a supply and demand perspective, the OPEC+ alliance's recent stance of maintaining production cuts has further supported oil prices. The eight OPEC+ countries have reached an agreement to maintain current oil production levels until March 2026, continuing the phased production cuts suspended since December 2025, and maintaining a voluntary production cut of 3.24 million barrels per day. Member countries are highly aligned on the "production cuts to stabilize prices" strategy. In January 2026, OPEC+ daily production decreased by 439,000 barrels month-on-month, far exceeding expectations. Meanwhile, unplanned supply disruptions in Kazakhstan, Venezuela, Iran, and other regions further compressed global supply redundancy. At the same time, the crude oil investment market is heating up. The latest circulating shares of a domestic ETF fund linked to oil and gas industry stocks are 1.859 billion units, with a circulating scale of 2.673 billion yuan, representing a more than ninefold increase this year, reflecting the continued rise in investor attention to the crude oil market.

The key issues that traders are currently most concerned about

Current news is generally positive for oil prices, but the extent of this positive impact depends on several key factors: how long the military action will last and whether it will become a large-scale operation lasting several weeks; which areas within Iran (military bases, oil facilities, nuclear facilities, etc.) the US will target; whether Iran can successfully blockade oil tanker traffic in the Strait of Hormuz, for how long the blockade will last, and whether it will retaliate against Israel with long-range missiles; whether Iran will retaliate against US military bases around the world, or even targets on the US mainland; whether the US-Iran negotiations can achieve a breakthrough on core differences, and whether the specific proposals submitted by Iran will be accepted by the US; in addition, whether Trump will ultimately authorize military action against Iran is also a key variable affecting oil price trends.

Historical experience warns that the impact of geopolitical conflicts on oil prices is persistent.

Looking back at the Iraq-Kuwait War of the 1990s, when Iraqi leader Saddam Hussein was attacked by the US military, he launched Scud missiles at Saudi Arabia and even set fire to domestic oil wells, causing a sharp short-term contraction in global crude oil supply and a temporary surge in oil prices. Currently, the market is concerned that if the conflict between the US and Iran escalates, Iran may resort to similar extreme measures, further exacerbating the risk of supply shortages. In particular, if the US and Israel launch a large-scale joint attack, Iran's retaliation could affect shipping in the Strait of Hormuz and surrounding oil production facilities, with an impact on global crude oil supply far exceeding expectations and with lasting effects.

Speculative funds exacerbate volatility, oil prices may see another 10%–20% increase.

The current crude oil market appears relatively calm, but the situation could change rapidly. Market analysts believe that if war breaks out, speculative funds will aggressively go long, forcing short sellers to liquidate their positions, potentially leading to a further 10%-20% increase in oil prices. Currently, the geopolitical risk premium has reached $5-8 per barrel, and if the military standoff does not ease in the short term, the risk premium still has room to rise. Meanwhile, the commodity market as a whole is performing strongly, with gold futures prices returning to the $5,000/ounce mark. As of 5 PM on February 19th, London spot gold closed at $5,015/ounce, a year-to-date increase of over 16%. The simultaneous rise in gold, silver, and crude oil reflects the coexistence of risk aversion and inflation expectations in the market, further driving speculative funds into the commodity market and indirectly exacerbating crude oil price volatility.

Technical Analysis: The market is driven by momentum and news, with the trading range widening.

(WTI crude oil daily chart source: FX678)

US crude oil rebounded from its low of $54.98 in January 2026, steadily rising along a clear red upward trend line. It has now broken through the previous densely traded area, showing a strong rebound from a technical perspective. Regarding the moving average system, the 50-day moving average ($60.37) and the 200-day moving average ($62.51) have both been firmly held by the price, and the short-term moving average has crossed above the long-term moving average, forming a bullish alignment and confirming a strengthening medium-term trend. As for oscillators, the RSI (14) is at 61.49, within the strong 50-70 range, indicating that bullish momentum remains, but it is approaching the overbought threshold, requiring caution regarding the risk of a short-term pullback. In the MACD indicator, both the DIFF and DEA are above the zero axis, and the red bars have narrowed slightly, suggesting that the upward momentum may slow down.

Key support levels below include: the red upward trend line at approximately $63.84, which is the core support for the recent rebound; a decisive break below this level could trigger a technical correction; the 200-day moving average at $62.51, a level with both psychological and technical significance; a breach of this level could lead to a test of the 50-day moving average at $60.37; and the 50% Fibonacci retracement level at $60.73, which resonates with the 50-day moving average and serves as a crucial defense line for the medium-term bulls. The upside target is the previous high of $66.48, which is the immediate resistance level for the current rebound; a break above $66.48 could lead to further gains towards $68.11 and $69.37.

Long-term outlook: Don't expect oil prices to stay above $100 for an extended period – global crude oil supply is ample.

It should be noted that global crude oil supply is currently ample, and only 20% of oil consumption relies on the Strait of Hormuz. Therefore, it is unnecessary to expect oil prices to remain above $90 or $100 per barrel in the long term. When the Russia-Ukraine conflict broke out in February 2022, crude oil futures surged to over $120 per barrel. Four years later, the conflict continues, and just a month ago, oil prices were only around $60 per barrel, nearly halved. This confirms that the support for oil prices from geopolitical conflicts is mostly temporary and unlikely to change the long-term supply and demand pattern.

From a fundamental perspective, the core focus should be on whether the Strait of Hormuz will be blocked and for how long, as this will determine how high oil prices can rise and how long they can maintain their current high levels. OPEC maintained its forecast in its latest monthly report that global oil demand will grow by 1.38 million barrels per day in 2026 and 1.34 million barrels per day in 2027, mainly supported by easing inflation, fiscal policy support, and improved trade. Meanwhile, the U.S. Energy Information Administration (EIA) estimates that China is continuously increasing its strategic reserves at a rate of approximately 1 million barrels per day, absorbing a significant portion of the global market's excess supply and alleviating concerns about oversupply to some extent. According to a comprehensive analysis of institutional views, oil prices will maintain a fluctuating upward trend in the short term, supported by geopolitical risks. However, in the long term, the global supply situation remains ample, and after a significant price increase, there is still room for a correction, and a sustained period above $100 per barrel is unlikely.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.