War rewrites interest rate rules; interest rate swaps leak information; war rhythm

2026-03-09 18:34:00

The escalating conflict in the Middle East has become a key variable affecting global interest rates and foreign exchange markets.

The surge in oil prices triggered by the war directly pushed up inflationary pressures, completely reversing the previous downward trend in global swap rates, which was dominated by declining inflation. After LIBOR ceased publication in September 2024, SOFR became the core of the US dollar benchmark interest rate system and served as the anchor for market financing costs.

This sudden change has not only significantly complicated global central bank interest rate cut expectations, but also further solidified the US dollar's core safe-haven status, and the global interest rate market is undergoing a dramatic restructuring driven by war.

The outbreak of the Middle East wars quickly impacted the global interest rate pricing mechanism, with the entire yield curve of the US dollar, euro, and pound sterling experiencing a sharp upward repricing.

Although the impact of war extends to multiple sectors, the core anchor of current market transactions remains crude oil—the supply disruptions and transportation risks caused by the war drive up oil prices, which in turn, through the inflation transmission chain, ultimately exert a reverse pressure on central bank interest rate policies.

Prior to this, swap rates had been declining continuously since the end of 2025, with the core logic being that market confidence in a slowdown in inflation was growing and that the central bank had already fully priced in subsequent easing cycles.

SOFR (Secured Overnight Financing Rate) is the benchmark interest rate published daily by the Federal Reserve Bank of New York. It is calculated based on actual transaction data in the overnight repurchase market using U.S. Treasury bonds as collateral, reflecting the cost for financial institutions to lend funds overnight using Treasury bonds as collateral. It has three core characteristics: near-risk-free, highly transparent, and based on real transactions.

The outbreak of the Middle East war completely reversed this trend that had lasted for months this week.

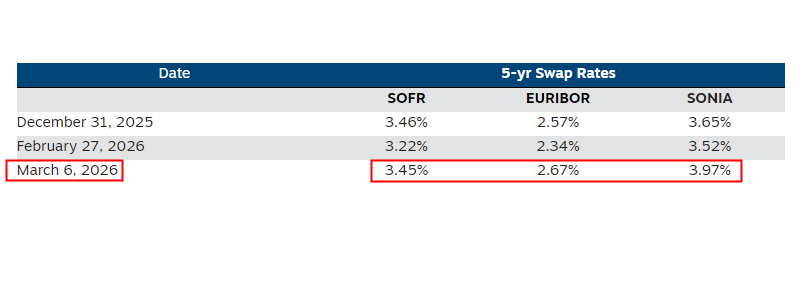

By comparing three key time points—the end of 2025, the week before the outbreak of war, and the week after the outbreak of war—the shifts in the five-year swap rates for the US dollar (SOFR), the euro, and the British pound (SONIA) are clearly visible, directly reflecting the impact of war on interest rate pricing.

In late February, the five-year swap rate fell significantly from its year-end level, and the market unanimously bet that the central bank's interest rate cut cycle would officially begin in 2026.

All currency financing entities are actively locking in long-term fixed interest rates based on the interest rate cuts in the forward curve, thus mitigating the risk of subsequent interest rate declines.

But the sudden outbreak of war changed everything.

In just one week from February 27 to March 6, the trading logic completely reversed: the five-year SOFR for the US dollar rose by more than 20 basis points, the euro swap rate climbed by more than 30 basis points, and the SONIA for the British pound jumped by nearly 45 basis points. After experiencing a fall followed by a rise, the market interest rate center was caught off guard by the war.

(Swap rates experienced an initial drop followed by a surge)

The reversal in the pound market was particularly dramatic, with interest rates rising directly above the end of 2025, demonstrating the extent of the restructuring of expectations triggered by the war.

The core driver of this round of interest rate repricing is the renewed rise in inflation expectations triggered by the war.

Geopolitical conflicts have directly driven up crude oil and commodity prices. Just as global inflation seemed to be entering its final decline phase, the rebound in energy prices has brought significant uncertainty to the path of inflation returning to the target.

More importantly, the inflation triggered by the war was a typical supply-driven inflation, which put the Bank of England, the Federal Reserve, and the European Central Bank in a policy dilemma.

Economists point out that the central bank's interest rate decision can neither increase oil production in the Persian Gulf nor reopen blocked trade routes. In the face of supply disruptions, monetary policy is essentially unable to solve the fundamental problem.

Inflation and expectations are facing upward risks again, making it difficult for the central bank to cut interest rates quickly at the pace previously expected by the market. However, aggressive interest rate hikes may turn external supply shocks into a decline in domestic demand, significantly compressing policy space.

In other words, the central bank's attempt to control inflation through interest rate adjustments may be futile and even have side effects at this moment.

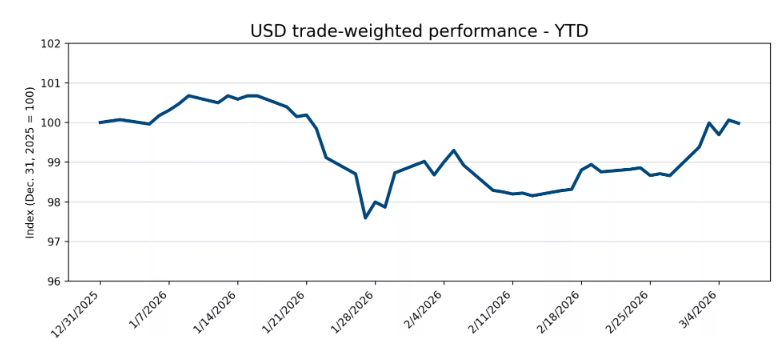

At the same time, the geopolitical uncertainty brought about by the Middle East wars has fully activated the safe-haven properties of the US dollar.

The US dollar trade-weighted index, with January 1, 2026 as the base of 100, has completely reversed its weak trend since the beginning of the year and has recently shown a strong upward trend, highlighting the continuous return of safe-haven funds to US dollar assets.

This phenomenon once again confirms that during the period when risk sentiment triggered by the war subsides, the US dollar remains the preferred safe-haven asset for global funds, and the market's previous concerns about the depreciation of the US dollar have been over-indulged.

For traders who previously shorted the US dollar but whose positions were impacted by the magnitude and speed of the current war-driven surge, the current level of significant dollar strength provides an ideal hedging window, effectively mitigating the risk of exchange rate fluctuations caused by the escalation of the war.

(US Dollar Index Trend)

In the event of sudden geopolitical events such as war, interest rate policy intervention often fails to achieve the desired effect and may even backfire. The market itself can quickly price the impact of geopolitics, and the market's pricing is largely based on the trend of global swap rates.

Since valuation is approximately equal to the square of E/r, when swap rates rise and raise the global interest rate center, the square of the interest rate r used to discount tech stock valuations and gold holding costs will also rise, leading to a significant drop in valuations or a significant increase in holding costs. The recent US-Iran conflict, which resulted in a sharp drop in US tech stocks and a lack of gold price increases, perfectly illustrates this point.

The lesson for traders is that in the face of extreme events like war, the development of geopolitical events themselves and interest rate trends are more leading indicators in the market. When we see swap rates rising and US Treasury yields continuing to rise, it indicates that the market believes that oil from the Strait of Hormuz cannot be transported out. Similarly, when US Treasury yields turn around, it also indicates that the turning point of the US-Iran war is coming.

The surge in oil prices triggered by the war directly pushed up inflationary pressures, completely reversing the previous downward trend in global swap rates, which was dominated by declining inflation. After LIBOR ceased publication in September 2024, SOFR became the core of the US dollar benchmark interest rate system and served as the anchor for market financing costs.

This sudden change has not only significantly complicated global central bank interest rate cut expectations, but also further solidified the US dollar's core safe-haven status, and the global interest rate market is undergoing a dramatic restructuring driven by war.

War directly impacts the global interest rate system; crude oil becomes the core of the transmission.

The outbreak of the Middle East wars quickly impacted the global interest rate pricing mechanism, with the entire yield curve of the US dollar, euro, and pound sterling experiencing a sharp upward repricing.

Although the impact of war extends to multiple sectors, the core anchor of current market transactions remains crude oil—the supply disruptions and transportation risks caused by the war drive up oil prices, which in turn, through the inflation transmission chain, ultimately exert a reverse pressure on central bank interest rate policies.

Prior to this, swap rates had been declining continuously since the end of 2025, with the core logic being that market confidence in a slowdown in inflation was growing and that the central bank had already fully priced in subsequent easing cycles.

SOFR (Secured Overnight Financing Rate) is the benchmark interest rate published daily by the Federal Reserve Bank of New York. It is calculated based on actual transaction data in the overnight repurchase market using U.S. Treasury bonds as collateral, reflecting the cost for financial institutions to lend funds overnight using Treasury bonds as collateral. It has three core characteristics: near-risk-free, highly transparent, and based on real transactions.

The outbreak of the Middle East war completely reversed this trend that had lasted for months this week.

The five-year swap rate has shifted dramatically, and war has rewritten market expectations.

By comparing three key time points—the end of 2025, the week before the outbreak of war, and the week after the outbreak of war—the shifts in the five-year swap rates for the US dollar (SOFR), the euro, and the British pound (SONIA) are clearly visible, directly reflecting the impact of war on interest rate pricing.

In late February, the five-year swap rate fell significantly from its year-end level, and the market unanimously bet that the central bank's interest rate cut cycle would officially begin in 2026.

All currency financing entities are actively locking in long-term fixed interest rates based on the interest rate cuts in the forward curve, thus mitigating the risk of subsequent interest rate declines.

But the sudden outbreak of war changed everything.

In just one week from February 27 to March 6, the trading logic completely reversed: the five-year SOFR for the US dollar rose by more than 20 basis points, the euro swap rate climbed by more than 30 basis points, and the SONIA for the British pound jumped by nearly 45 basis points. After experiencing a fall followed by a rise, the market interest rate center was caught off guard by the war.

(Swap rates experienced an initial drop followed by a surge)

The reversal in the pound market was particularly dramatic, with interest rates rising directly above the end of 2025, demonstrating the extent of the restructuring of expectations triggered by the war.

War fuels inflation expectations, putting central banks in a policy dilemma.

The core driver of this round of interest rate repricing is the renewed rise in inflation expectations triggered by the war.

Geopolitical conflicts have directly driven up crude oil and commodity prices. Just as global inflation seemed to be entering its final decline phase, the rebound in energy prices has brought significant uncertainty to the path of inflation returning to the target.

More importantly, the inflation triggered by the war was a typical supply-driven inflation, which put the Bank of England, the Federal Reserve, and the European Central Bank in a policy dilemma.

Economists point out that the central bank's interest rate decision can neither increase oil production in the Persian Gulf nor reopen blocked trade routes. In the face of supply disruptions, monetary policy is essentially unable to solve the fundamental problem.

Inflation and expectations are facing upward risks again, making it difficult for the central bank to cut interest rates quickly at the pace previously expected by the market. However, aggressive interest rate hikes may turn external supply shocks into a decline in domestic demand, significantly compressing policy space.

In other words, the central bank's attempt to control inflation through interest rate adjustments may be futile and even have side effects at this moment.

War triggers risk aversion, strengthening the dollar and providing a hedging window.

At the same time, the geopolitical uncertainty brought about by the Middle East wars has fully activated the safe-haven properties of the US dollar.

The US dollar trade-weighted index, with January 1, 2026 as the base of 100, has completely reversed its weak trend since the beginning of the year and has recently shown a strong upward trend, highlighting the continuous return of safe-haven funds to US dollar assets.

This phenomenon once again confirms that during the period when risk sentiment triggered by the war subsides, the US dollar remains the preferred safe-haven asset for global funds, and the market's previous concerns about the depreciation of the US dollar have been over-indulged.

For traders who previously shorted the US dollar but whose positions were impacted by the magnitude and speed of the current war-driven surge, the current level of significant dollar strength provides an ideal hedging window, effectively mitigating the risk of exchange rate fluctuations caused by the escalation of the war.

(US Dollar Index Trend)

Summarize:

In the event of sudden geopolitical events such as war, interest rate policy intervention often fails to achieve the desired effect and may even backfire. The market itself can quickly price the impact of geopolitics, and the market's pricing is largely based on the trend of global swap rates.

Since valuation is approximately equal to the square of E/r, when swap rates rise and raise the global interest rate center, the square of the interest rate r used to discount tech stock valuations and gold holding costs will also rise, leading to a significant drop in valuations or a significant increase in holding costs. The recent US-Iran conflict, which resulted in a sharp drop in US tech stocks and a lack of gold price increases, perfectly illustrates this point.

The lesson for traders is that in the face of extreme events like war, the development of geopolitical events themselves and interest rate trends are more leading indicators in the market. When we see swap rates rising and US Treasury yields continuing to rise, it indicates that the market believes that oil from the Strait of Hormuz cannot be transported out. Similarly, when US Treasury yields turn around, it also indicates that the turning point of the US-Iran war is coming.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.