Citigroup predicts the Bank of Korea will raise interest rates twice to 3% in 2026.

2026-03-18 17:15:00

According to APP, Citigroup stated that the Bank of Korea (BOK) may raise its policy rate to 3% this year as soaring global oil prices push up inflation. Citigroup economist Jin-Wook Kim wrote in a report that the BOK is expected to raise rates twice, by 25 basis points each time, once in July and once in October, bringing the benchmark rate close to 3%. These moves would mark the resumption of a tightening cycle after a long pause, as price pressures have proven more persistent than previously anticipated. Brent crude oil may rise to $110-$120 per barrel in the near term, affected by disruptions related to the conflict with Iran, before falling back later this year. This price surge—equivalent to a further increase of up to 20% over the next 12 months on top of already high oil prices—will have a greater impact on inflation than on economic growth. The significant asymmetric impact of rising oil prices on inflation will prompt the BOK to adopt a more hawkish stance, especially given historically loose financial conditions.

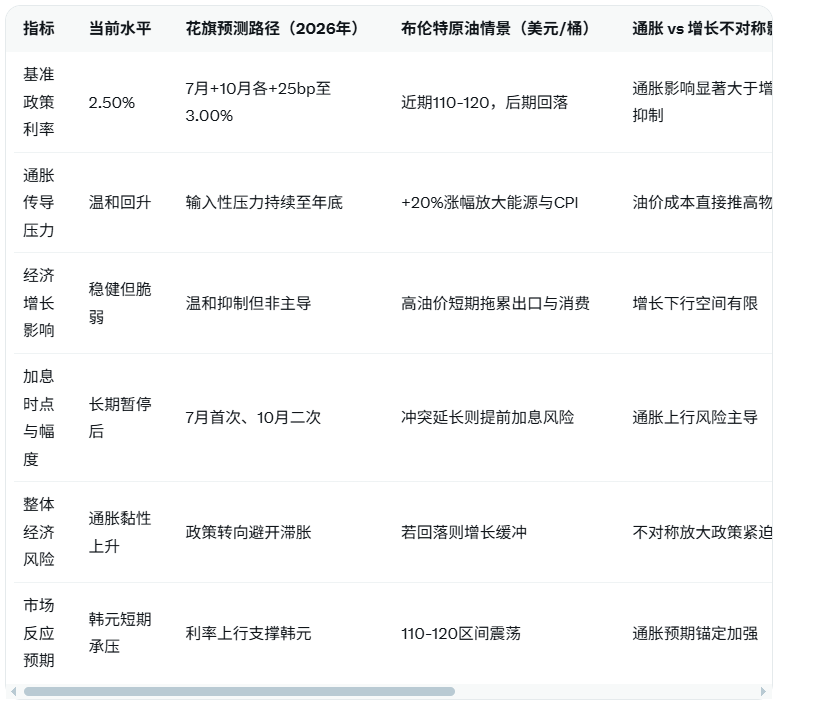

The latest market data shows that as of March 2026, the Bank of Korea's benchmark interest rate will remain stable at 2.50%, the latest level since the pause in rate hikes at the end of 2024. This forecast will bring the interest rate up by a cumulative 50 basis points to 3.00% within the year, which is in stark contrast to the Federal Reserve's current path of maintaining a higher and longer range of 3.50%-3.75%.

To clearly compare the policy paths and their multi-dimensional impacts, the following table presents key indicators (including interest rate levels, oil price scenarios, asymmetric shocks to inflation and growth, timing of policy shifts, comparison with the Federal Reserve's strategy, and key expert assessments):

From an in-depth analysis perspective, the Iranian conflict, through disruptions to channels like the Strait of Hormuz, directly pushed up Brent crude oil prices. Jin-Wook Kim explicitly contrasted this with the Federal Reserve's strategy of "higher and longer": the Fed delayed interest rate cuts due to similar oil price shocks, while South Korea, as an import-dependent economy, faces more direct and asymmetrical imported inflationary pressures. A 20% increase in oil prices significantly boosts CPI more than it drags down GDP. It's reasonable to speculate that if crude oil prices remain in the $110-$120 range until the second quarter, South Korea's annual inflation may exceed 3.5%, forcing the central bank to precisely raise interest rates in July and October to anchor expectations. Conversely, if the conflict eases in mid-to-late April, a drop in oil prices will buffer growth pressure, but the policy shift will be irreversible. This comparison with the Fed's path highlights the vulnerability of major Asian economies to global energy shocks. Historically, loose monetary conditions have further amplified the necessity of interest rate hikes to avoid an inflationary spiral. Coupled with an export-oriented growth model, while high oil prices are a short-term negative for consumption and investment, they provide relative support for the Korean won, creating a linkage effect with the Fed's strong dollar.

On the other hand, the resilience of the US economy raises the bar for the Federal Reserve to cut interest rates, while South Korea needs to be more proactive in addressing imported risks. Citigroup's assessment indicates that the asymmetric impact of oil prices on inflation will become a core policy variable. A hawkish stance from the central bank will help stabilize financial conditions, but caution is needed regarding the potential for excessive tightening to have a secondary impact on exports. Traders generally believe that this forecast will drive a short-term strengthening of the Korean won, a slight steepening of the yield curve, and create a cross-market resonance with the signals from the Federal Reserve meeting.

Editor's Summary : While the surge in oil prices due to the Iranian conflict has amplified global inflation uncertainty, Citi's forecast of two rate hikes by the Bank of Korea to 3%, compared to the Federal Reserve's higher and longer-term path, highlights the accelerating transmission of geopolitical risks to the policies of Asian importing countries. The future pace of interest rates depends on the speed of oil price declines and inflation confirmation; the market needs to continue monitoring the July meeting and crude oil developments.

Frequently Asked Questions

Q1: Why does Citi predict that the Bank of Korea will raise interest rates twice to 3% in 2026 instead of keeping them unchanged?

A: Jin-Wook Kim points out that the Iranian conflict has pushed Brent crude oil prices to $110-120, equivalent to a 20% increase in oil prices over the next 12 months. Imported inflationary pressures are far greater than previously expected and are more persistent. The resumption of tightening after a long pause is precisely to offset this asymmetric impact, contrasting with the Federal Reserve's strategy of delaying rate cuts for a longer period due to similar oil prices, thus preventing inflation from spiraling out of control.

Q2: Where exactly does the asymmetric impact of rising oil prices on South Korea's inflation and economic growth manifest itself?

A: Soaring oil prices directly increase energy, transportation, and import costs, amplifying the risk of CPI increases, while the drag on export-oriented growth is relatively mild. Citi emphasizes that this asymmetric effect will prompt central banks to take a tough stance, especially since historically, under loose monetary conditions, inflation transmission has been much faster than growth suppression, directly driving a policy shift.

Q3: How does the Bank of Korea's approach differ from the Federal Reserve's strategy of higher and longer interest rates?

A: The Federal Reserve is currently maintaining a rate of 3.50%-3.75% and focusing on labor market and dot plot divergences, while South Korea, due to its import dependence, will act earlier, raising rates twice by 25 basis points to 3%. Citi's comparison shows that oil prices have a more direct impact on South Korean inflation, and the policy pace is faster, but both are trending towards tightening due to geopolitical shocks, creating a cross-market linkage effect.

Q4: If the conflict with Iran eases in mid-to-late April, will the forecast for South Korea's interest rate hike be adjusted?

A: Easing will push oil prices down, easing imported pressures and potentially delaying the October rate hike. However, Citigroup believes that the persistence of inflation has proven, and the first rate hike in July is highly likely to continue. The overall tightening cycle will restart, but the magnitude and timing will be more flexible.

The latest market data shows that as of March 2026, the Bank of Korea's benchmark interest rate will remain stable at 2.50%, the latest level since the pause in rate hikes at the end of 2024. This forecast will bring the interest rate up by a cumulative 50 basis points to 3.00% within the year, which is in stark contrast to the Federal Reserve's current path of maintaining a higher and longer range of 3.50%-3.75%.

To clearly compare the policy paths and their multi-dimensional impacts, the following table presents key indicators (including interest rate levels, oil price scenarios, asymmetric shocks to inflation and growth, timing of policy shifts, comparison with the Federal Reserve's strategy, and key expert assessments):

From an in-depth analysis perspective, the Iranian conflict, through disruptions to channels like the Strait of Hormuz, directly pushed up Brent crude oil prices. Jin-Wook Kim explicitly contrasted this with the Federal Reserve's strategy of "higher and longer": the Fed delayed interest rate cuts due to similar oil price shocks, while South Korea, as an import-dependent economy, faces more direct and asymmetrical imported inflationary pressures. A 20% increase in oil prices significantly boosts CPI more than it drags down GDP. It's reasonable to speculate that if crude oil prices remain in the $110-$120 range until the second quarter, South Korea's annual inflation may exceed 3.5%, forcing the central bank to precisely raise interest rates in July and October to anchor expectations. Conversely, if the conflict eases in mid-to-late April, a drop in oil prices will buffer growth pressure, but the policy shift will be irreversible. This comparison with the Fed's path highlights the vulnerability of major Asian economies to global energy shocks. Historically, loose monetary conditions have further amplified the necessity of interest rate hikes to avoid an inflationary spiral. Coupled with an export-oriented growth model, while high oil prices are a short-term negative for consumption and investment, they provide relative support for the Korean won, creating a linkage effect with the Fed's strong dollar.

On the other hand, the resilience of the US economy raises the bar for the Federal Reserve to cut interest rates, while South Korea needs to be more proactive in addressing imported risks. Citigroup's assessment indicates that the asymmetric impact of oil prices on inflation will become a core policy variable. A hawkish stance from the central bank will help stabilize financial conditions, but caution is needed regarding the potential for excessive tightening to have a secondary impact on exports. Traders generally believe that this forecast will drive a short-term strengthening of the Korean won, a slight steepening of the yield curve, and create a cross-market resonance with the signals from the Federal Reserve meeting.

Editor's Summary : While the surge in oil prices due to the Iranian conflict has amplified global inflation uncertainty, Citi's forecast of two rate hikes by the Bank of Korea to 3%, compared to the Federal Reserve's higher and longer-term path, highlights the accelerating transmission of geopolitical risks to the policies of Asian importing countries. The future pace of interest rates depends on the speed of oil price declines and inflation confirmation; the market needs to continue monitoring the July meeting and crude oil developments.

Frequently Asked Questions

Q1: Why does Citi predict that the Bank of Korea will raise interest rates twice to 3% in 2026 instead of keeping them unchanged?

A: Jin-Wook Kim points out that the Iranian conflict has pushed Brent crude oil prices to $110-120, equivalent to a 20% increase in oil prices over the next 12 months. Imported inflationary pressures are far greater than previously expected and are more persistent. The resumption of tightening after a long pause is precisely to offset this asymmetric impact, contrasting with the Federal Reserve's strategy of delaying rate cuts for a longer period due to similar oil prices, thus preventing inflation from spiraling out of control.

Q2: Where exactly does the asymmetric impact of rising oil prices on South Korea's inflation and economic growth manifest itself?

A: Soaring oil prices directly increase energy, transportation, and import costs, amplifying the risk of CPI increases, while the drag on export-oriented growth is relatively mild. Citi emphasizes that this asymmetric effect will prompt central banks to take a tough stance, especially since historically, under loose monetary conditions, inflation transmission has been much faster than growth suppression, directly driving a policy shift.

Q3: How does the Bank of Korea's approach differ from the Federal Reserve's strategy of higher and longer interest rates?

A: The Federal Reserve is currently maintaining a rate of 3.50%-3.75% and focusing on labor market and dot plot divergences, while South Korea, due to its import dependence, will act earlier, raising rates twice by 25 basis points to 3%. Citi's comparison shows that oil prices have a more direct impact on South Korean inflation, and the policy pace is faster, but both are trending towards tightening due to geopolitical shocks, creating a cross-market linkage effect.

Q4: If the conflict with Iran eases in mid-to-late April, will the forecast for South Korea's interest rate hike be adjusted?

A: Easing will push oil prices down, easing imported pressures and potentially delaying the October rate hike. However, Citigroup believes that the persistence of inflation has proven, and the first rate hike in July is highly likely to continue. The overall tightening cycle will restart, but the magnitude and timing will be more flexible.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.