A chart shows that the Baltic Dry Index has fallen to a near two-week low, with freight rates weakening across all vessel types.

2026-03-25 01:11:56

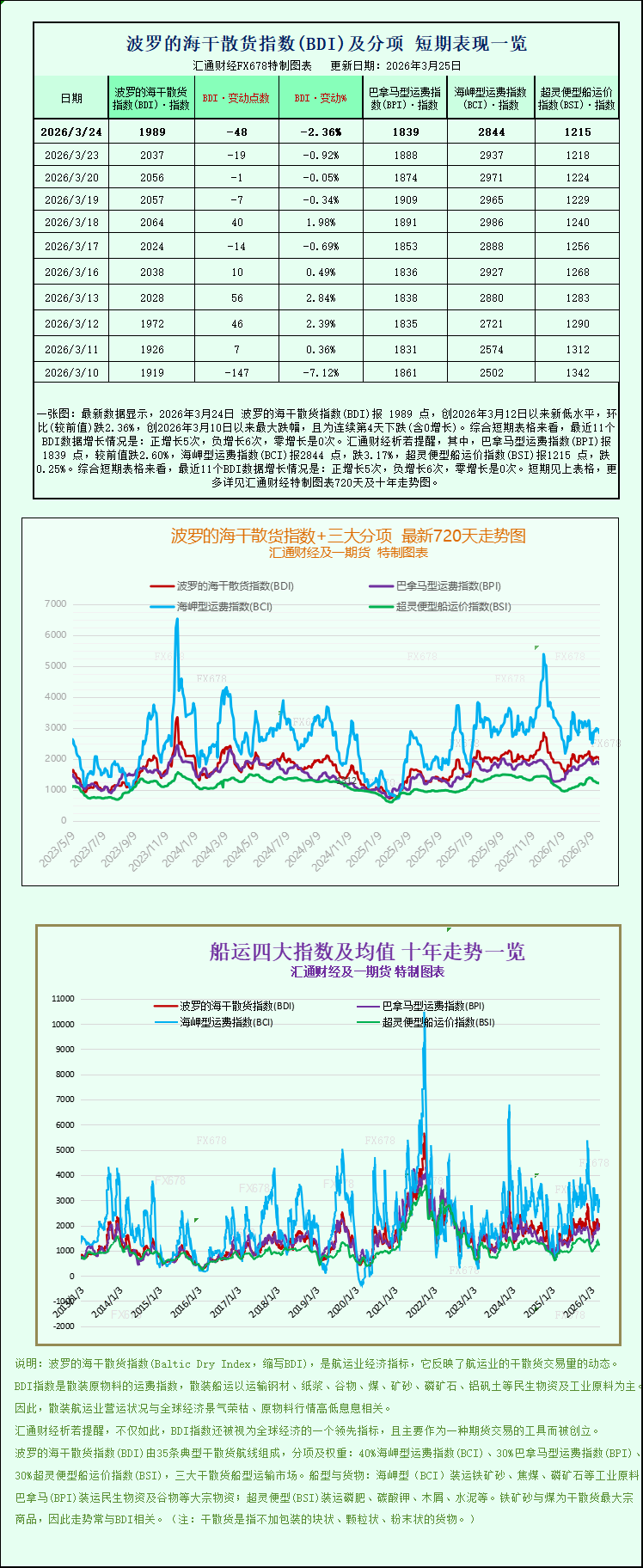

Latest data shows that the Baltic Dry Index (BDI) was at 1989 points on March 24, 2026, a new low since March 12, 2026, down 2.36% month-on-month, the largest drop since March 10, 2026, and the fourth consecutive day of decline (including zero growth). Looking at the short-term charts, the recent 11 BDI data points show: 5 positive increases, 6 negative increases, and 0 zero increases. Specifically, the Panamax Freight Index (BPI) was at 1839 points, down 2.60% from the previous value; the Capesize Freight Index (BCI) was at 2844 points, down 3.17%; and the Supramax Freight Index (BSI) was at 1215 points, down 0.25%. For detailed 720-day and 10-year trend charts of the Baltic Dry Index and its three main sub-indices, please refer to the specially designed charts.

As a core indicator of the global dry bulk shipping market, the Baltic Dry Index (BDI) fell sharply on Tuesday, hitting its lowest point in nearly two weeks. This decline was mainly dragged down by a slight decrease in freight rates across all vessel types. The market's short-term supply and demand dynamics are weak, coupled with indirect disturbances from geopolitical situations, leading to a general correction in dry bulk shipping freight rates.

The Baltic Dry Index (BDI), a leading indicator for monitoring global dry bulk shipping costs, comprehensively covers the three major dry bulk vessel types: Capesize, Panamax, and Supramax, accurately reflecting the health of global commodity maritime trade. On Tuesday, the core index fell 48 points, a drop of 2.4%, closing at 1989 points. This figure represents a new low since March 12th, highlighting the current pressure on freight rates in the dry bulk shipping market.

Looking at specific vessel types, the Capesize index, which has the largest capacity and is primarily used for transporting large dry bulk cargoes, saw the most significant decline, plunging 93 points in a single day, a drop of 3.2%, closing at 2844 points. This decline has continued for two consecutive trading days, making it the main driver of the overall index's downward trend. As the main vessel type for transporting ultra-large dry bulk cargoes such as iron ore and coal, Capesize vessels typically have a single-trip cargo capacity of up to 150,000 tons. Their profitability has also declined sharply, with average daily freight revenue decreasing by $839 to $23,292, indicating a continued narrowing of profit margins.

In response to the external factors influencing current market volatility, Filipe Gouveia, Shipping Analysis Manager at the Baltic International Shipping Council (BIMCO), released a special analysis report on Tuesday, interpreting the transmission effect of geopolitical conflicts on dry bulk trade. Gouveia clearly pointed out that the geopolitical friction triggered by the situation in Iran has a relatively limited direct negative impact on global iron ore trade. Dry bulk shipments via the Strait of Hormuz account for only 2% of global ton-mile demand, and the Oman route also accounts for only 2%. The impact of disruptions to direct logistics channels is manageable.

However, he also emphasized that the indirect impact of this geopolitical conflict cannot be ignored: on the one hand, the conflict directly leads to a tightening of global diesel supply, and core global mineral exporting countries such as Australia and South Africa are highly dependent on diesel imports. Diesel shortages may directly restrict the progress of local mining operations, thereby reducing the shipment volume of dry bulk commodities such as iron ore and coal, and suppressing shipping demand from the source of goods; on the other hand, the chain economic effect triggered by rising energy prices may further weaken domestic steel consumption demand in China. As the world's largest importer of dry bulk commodities, China's demand trend directly affects the lifeline of the global dry bulk shipping market, and the expectation of weak demand in the future will further depress freight rates.

The Panamax market, particularly for medium-capacity vessels, also experienced a downturn, with the index falling 49 points, or 2.6%, to close at 1839. Panamax vessels primarily transport 60,000 to 70,000 tons of bulk cargo such as coal and grain, and are crucial for global food and energy shipping. Their average daily freight revenue decreased by $442 to $16,552, resulting in a corresponding decline in profitability.

In addition, the Supramax bulk carrier index, which mainly focuses on small and medium-sized bulk cargo transportation, was also not spared. Although the decline was relatively mild, it only fell slightly by 3 points, a drop of 0.3%, but still closed down at 1215 points. Thus, the freight rates of the three major ship types have all weakened, further confirming the overall downward trend of the dry bulk shipping market in this round.

As a core indicator of the global dry bulk shipping market, the Baltic Dry Index (BDI) fell sharply on Tuesday, hitting its lowest point in nearly two weeks. This decline was mainly dragged down by a slight decrease in freight rates across all vessel types. The market's short-term supply and demand dynamics are weak, coupled with indirect disturbances from geopolitical situations, leading to a general correction in dry bulk shipping freight rates.

The Baltic Dry Index (BDI), a leading indicator for monitoring global dry bulk shipping costs, comprehensively covers the three major dry bulk vessel types: Capesize, Panamax, and Supramax, accurately reflecting the health of global commodity maritime trade. On Tuesday, the core index fell 48 points, a drop of 2.4%, closing at 1989 points. This figure represents a new low since March 12th, highlighting the current pressure on freight rates in the dry bulk shipping market.

Looking at specific vessel types, the Capesize index, which has the largest capacity and is primarily used for transporting large dry bulk cargoes, saw the most significant decline, plunging 93 points in a single day, a drop of 3.2%, closing at 2844 points. This decline has continued for two consecutive trading days, making it the main driver of the overall index's downward trend. As the main vessel type for transporting ultra-large dry bulk cargoes such as iron ore and coal, Capesize vessels typically have a single-trip cargo capacity of up to 150,000 tons. Their profitability has also declined sharply, with average daily freight revenue decreasing by $839 to $23,292, indicating a continued narrowing of profit margins.

In response to the external factors influencing current market volatility, Filipe Gouveia, Shipping Analysis Manager at the Baltic International Shipping Council (BIMCO), released a special analysis report on Tuesday, interpreting the transmission effect of geopolitical conflicts on dry bulk trade. Gouveia clearly pointed out that the geopolitical friction triggered by the situation in Iran has a relatively limited direct negative impact on global iron ore trade. Dry bulk shipments via the Strait of Hormuz account for only 2% of global ton-mile demand, and the Oman route also accounts for only 2%. The impact of disruptions to direct logistics channels is manageable.

However, he also emphasized that the indirect impact of this geopolitical conflict cannot be ignored: on the one hand, the conflict directly leads to a tightening of global diesel supply, and core global mineral exporting countries such as Australia and South Africa are highly dependent on diesel imports. Diesel shortages may directly restrict the progress of local mining operations, thereby reducing the shipment volume of dry bulk commodities such as iron ore and coal, and suppressing shipping demand from the source of goods; on the other hand, the chain economic effect triggered by rising energy prices may further weaken domestic steel consumption demand in China. As the world's largest importer of dry bulk commodities, China's demand trend directly affects the lifeline of the global dry bulk shipping market, and the expectation of weak demand in the future will further depress freight rates.

The Panamax market, particularly for medium-capacity vessels, also experienced a downturn, with the index falling 49 points, or 2.6%, to close at 1839. Panamax vessels primarily transport 60,000 to 70,000 tons of bulk cargo such as coal and grain, and are crucial for global food and energy shipping. Their average daily freight revenue decreased by $442 to $16,552, resulting in a corresponding decline in profitability.

In addition, the Supramax bulk carrier index, which mainly focuses on small and medium-sized bulk cargo transportation, was also not spared. Although the decline was relatively mild, it only fell slightly by 3 points, a drop of 0.3%, but still closed down at 1215 points. Thus, the freight rates of the three major ship types have all weakened, further confirming the overall downward trend of the dry bulk shipping market in this round.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.