The continued closure of the strait has triggered a disruption in energy supply, and a global crude oil shortage is gradually becoming a reality.

2026-05-18 12:18:20

In just a few months, the market situation has completely reversed. The previously unimaginable global crude oil supply shortage is gradually becoming a reality as the Strait of Hormuz is almost completely shut down.

Industry institutions and market analysts are no longer optimistic about a quick resolution to the related conflicts, but are instead wary of the chain reaction caused by prolonged disruptions to energy transportation routes. With significant reductions in crude oil production capacity in many Middle Eastern countries and accelerated depletion of global crude oil inventories, the previous logic of oversupply has been completely overturned. The energy market has officially entered a period of tight supply and demand, and upward pressure on oil prices continues to increase.

Since the unrest escalated, the production and transportation of crude oil in the Middle East has been severely disrupted.

According to data from energy analysis firm Kepler, from February 28 to May 8, the cumulative reduction in crude oil supply in the Middle East reached 782 million barrels. At the current pace of reduction, the cumulative reduction will exceed one billion barrels by the end of May. In terms of daily production, the scale of production cuts by oil-producing countries is enormous. Saudi Arabia's daily crude oil production has decreased by more than three million barrels, and Iraq, Iran, and Kuwait have also experienced large-scale daily production cuts, resulting in a significant decline in the region's crude oil supply capacity.

With large-scale production halts, utilizing crude oil inventories has become the market's primary response. Previously, the International Energy Agency (IEA), based on high inventory data, predicted a significant oversupply in the market; however, this assessment has now become completely ineffective. The agency's latest monthly report explicitly warns that the global crude oil market will shift to a supply-demand imbalance this year, with global daily crude oil supply expected to decrease by 3.9 million barrels, while the actual daily supply gap in the Middle East is as high as 10.5 million barrels. In contrast, the decline in demand has been negligible, exacerbating the supply-demand imbalance.

Ellen Wald, a senior fellow at the Atlantic Council's Global Energy Center, stated that there is very limited room for further declines in global crude oil consumption. Once commercial and strategic inventories are depleted, the market will face the risk of crude oil supply disruptions, at which point international oil prices will surge. This view is echoed by senior executives at Saudi Aramco, who stated that global onshore fuel oil inventories are currently being depleted at an unprecedented rate, and that these inventories, currently the only market buffer, have already seen a substantial reduction in size.

JPMorgan Chase's commodities team also issued a risk warning, predicting that commercial crude oil inventories in developed economies will reach critical levels of operational pressure next month, significantly increasing the difficulty of market allocation of crude oil and filling supply gaps. Natasha Kaneva, the bank's global head of commodities strategy, said that the best way to resolve this energy crisis is to restore normal navigation in the Strait of Hormuz in June. If the situation does not improve, the energy shock will gradually spread from simply rising oil prices to the refining industry and end-user fuel consumption, triggering a comprehensive energy shortage.

The market had previously overestimated the actual available size of crude oil inventories. A Saudi Aramco official stated that not all of the reported crude oil inventory is available for market use. A significant amount of crude oil is constrained by pipeline capacity, minimum safe storage levels in tanks, and daily operational rules, preventing its arbitrary release. Mature markets in Europe and the US have a hard limit on the total amount of crude oil that can be released from inventory daily, with a maximum daily release of only two million barrels. This inventory release capacity is insufficient to match the massive supply gap.

Currently, the decline in global onshore crude oil inventories is relatively gradual, with a cumulative reduction of approximately 60 million barrels since late March. While the overall inventory base remains large, the available resources for flexible allocation are very limited. If the disruption to the export of Middle Eastern crude oil continues, the market will have no choice but to increase inventory withdrawals, and if new crude oil supply cannot replenish the shortfall in time, the previously ample inventory buffer will shrink rapidly.

As tensions persist, industry participants have gradually adapted to the current tight supply situation. The previous panic buying of spot crude oil has subsided, and the market as a whole has shifted from panic and risk aversion to a rational response to the current scarcity of resources.

Hamad Hussain, a commodities economist at Capital Economics, said that after the emergency buying frenzy subsided, global crude oil inventories continued to be depleted at a relatively fast pace. With the fundamental support of continuously decreasing inventories, a steady rise in international oil prices is inevitable.

Overall, the obstruction of passage through the Strait of Hormuz has fundamentally reshaped the global oil supply and demand landscape. Large-scale production cuts in the Middle East have ushered in a period of supply shortages. Previously ample oil inventories are being continuously depleted, and with numerous rigid restrictions on their use, the market's ability to withstand energy risks continues to weaken. The situation is unlikely to ease quickly in the short term, and the global oil supply shortage will persist. Once the inventory buffer is exhausted, energy market volatility will further intensify, providing solid upward support for oil prices in the medium to long term.

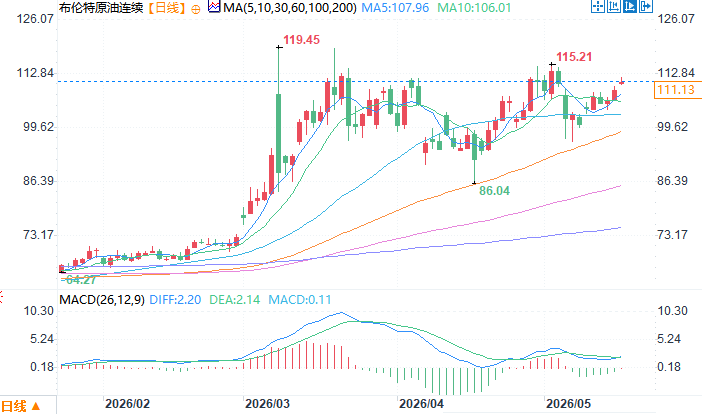

Brent crude oil daily chart source: EasyForex

At 12:17 Beijing time on May 18, Brent crude oil futures were trading at $111.23 per barrel.

Industry institutions and market analysts are no longer optimistic about a quick resolution to the related conflicts, but are instead wary of the chain reaction caused by prolonged disruptions to energy transportation routes. With significant reductions in crude oil production capacity in many Middle Eastern countries and accelerated depletion of global crude oil inventories, the previous logic of oversupply has been completely overturned. The energy market has officially entered a period of tight supply and demand, and upward pressure on oil prices continues to increase.

Middle Eastern production capacity has plummeted, and the crude oil supply gap continues to widen.

Since the unrest escalated, the production and transportation of crude oil in the Middle East has been severely disrupted.

According to data from energy analysis firm Kepler, from February 28 to May 8, the cumulative reduction in crude oil supply in the Middle East reached 782 million barrels. At the current pace of reduction, the cumulative reduction will exceed one billion barrels by the end of May. In terms of daily production, the scale of production cuts by oil-producing countries is enormous. Saudi Arabia's daily crude oil production has decreased by more than three million barrels, and Iraq, Iran, and Kuwait have also experienced large-scale daily production cuts, resulting in a significant decline in the region's crude oil supply capacity.

With large-scale production halts, utilizing crude oil inventories has become the market's primary response. Previously, the International Energy Agency (IEA), based on high inventory data, predicted a significant oversupply in the market; however, this assessment has now become completely ineffective. The agency's latest monthly report explicitly warns that the global crude oil market will shift to a supply-demand imbalance this year, with global daily crude oil supply expected to decrease by 3.9 million barrels, while the actual daily supply gap in the Middle East is as high as 10.5 million barrels. In contrast, the decline in demand has been negligible, exacerbating the supply-demand imbalance.

With inventory buffers nearing depletion, energy security risks are becoming increasingly apparent.

Ellen Wald, a senior fellow at the Atlantic Council's Global Energy Center, stated that there is very limited room for further declines in global crude oil consumption. Once commercial and strategic inventories are depleted, the market will face the risk of crude oil supply disruptions, at which point international oil prices will surge. This view is echoed by senior executives at Saudi Aramco, who stated that global onshore fuel oil inventories are currently being depleted at an unprecedented rate, and that these inventories, currently the only market buffer, have already seen a substantial reduction in size.

JPMorgan Chase's commodities team also issued a risk warning, predicting that commercial crude oil inventories in developed economies will reach critical levels of operational pressure next month, significantly increasing the difficulty of market allocation of crude oil and filling supply gaps. Natasha Kaneva, the bank's global head of commodities strategy, said that the best way to resolve this energy crisis is to restore normal navigation in the Strait of Hormuz in June. If the situation does not improve, the energy shock will gradually spread from simply rising oil prices to the refining industry and end-user fuel consumption, triggering a comprehensive energy shortage.

Inventory utilization is limited and market buffer capacity is far lower than expected.

The market had previously overestimated the actual available size of crude oil inventories. A Saudi Aramco official stated that not all of the reported crude oil inventory is available for market use. A significant amount of crude oil is constrained by pipeline capacity, minimum safe storage levels in tanks, and daily operational rules, preventing its arbitrary release. Mature markets in Europe and the US have a hard limit on the total amount of crude oil that can be released from inventory daily, with a maximum daily release of only two million barrels. This inventory release capacity is insufficient to match the massive supply gap.

Currently, the decline in global onshore crude oil inventories is relatively gradual, with a cumulative reduction of approximately 60 million barrels since late March. While the overall inventory base remains large, the available resources for flexible allocation are very limited. If the disruption to the export of Middle Eastern crude oil continues, the market will have no choice but to increase inventory withdrawals, and if new crude oil supply cannot replenish the shortfall in time, the previously ample inventory buffer will shrink rapidly.

Market sentiment is stabilizing, and a steady upward trend in oil prices is becoming the norm.

As tensions persist, industry participants have gradually adapted to the current tight supply situation. The previous panic buying of spot crude oil has subsided, and the market as a whole has shifted from panic and risk aversion to a rational response to the current scarcity of resources.

Hamad Hussain, a commodities economist at Capital Economics, said that after the emergency buying frenzy subsided, global crude oil inventories continued to be depleted at a relatively fast pace. With the fundamental support of continuously decreasing inventories, a steady rise in international oil prices is inevitable.

Summarize

Overall, the obstruction of passage through the Strait of Hormuz has fundamentally reshaped the global oil supply and demand landscape. Large-scale production cuts in the Middle East have ushered in a period of supply shortages. Previously ample oil inventories are being continuously depleted, and with numerous rigid restrictions on their use, the market's ability to withstand energy risks continues to weaken. The situation is unlikely to ease quickly in the short term, and the global oil supply shortage will persist. Once the inventory buffer is exhausted, energy market volatility will further intensify, providing solid upward support for oil prices in the medium to long term.

Brent crude oil daily chart source: EasyForex

At 12:17 Beijing time on May 18, Brent crude oil futures were trading at $111.23 per barrel.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.