The yield on 10-year Japanese government bonds has broken a 40-year record! Why is the market not buying into Japan's promise of "expanding spending without increasing debt"?

2026-06-01 15:29:52

Faced with multiple pressures including high energy prices, a continuously depreciating yen, and rising living costs, the Japanese government has launched a new round of supplementary budgets to alleviate the burden on households. This fiscal adjustment breaks with Japan's previous policy stance, and coupled with the official adjustment of statistical methods, it has triggered deep skepticism in the capital markets.

Japanese government bond yields have surged, fiscal and inflation risks are escalating simultaneously, and the yen exchange rate remains under pressure. Although there are some bright spots in Japan's economic fundamentals, the negative signals in the bond and foreign exchange markets indicate that Japan's subsequent macroeconomic control will face enormous challenges.

Japanese Prime Minister Sanae Takaichi spearheaded the drafting of a new round of supplementary fiscal budget, with the core objective of offsetting inflationary and energy price pressures and providing a safety net for ordinary families.

The supplementary budget amounts to approximately 3 trillion yen, equivalent to US$19 billion , which is in line with previous market expectations. The core background for this policy is the persistently high international commodity and fuel prices due to the Middle East situation, leading to a continuous increase in Japan's fuel subsidy expenditures. This, coupled with the weak yen, has exacerbated domestic pressures on people's livelihoods.

It is noteworthy that this additional fiscal expenditure marks a significant shift in Kaohsiung City's policy stance, which had previously consistently maintained that no additional fiscal spending was needed. Simultaneously, the official statement indicated that the total issuance of government bonds for the 2026 calendar year will remain unchanged from the original budget plan, and that the city intends to cover the increased budget expenditures through government bonds, attempting to stabilize capital market expectations.

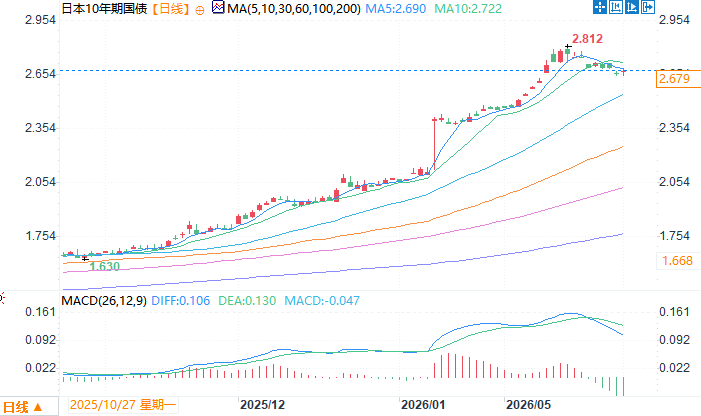

Market skepticism regarding Japan's fiscal policy was quickly reflected in the bond market. On May 20, the yield on Japan's 10-year government bonds surged to 2.812%, closing at 2.772%, a more than 40-year high since 1996. This significant volatility in the bond market fully reflects the market's dual concerns about Japan's fiscal vulnerabilities and rising inflation.

Jesper Koll, a professional director at Monax Group, said that the bond market has a strong ability to identify risks, and that the expansion of fiscal spending will inevitably correspond to an increase in debt. Therefore, the Japanese government's statement of "expanding spending without increasing debt" is untenable .

The core of the market's doubts lies in Sanae Takashi's unusual method of using the calendar year to calculate the scale of bond issuance. Japan has long used March 31st as the end point of the fiscal year and has never used the calendar year to formulate fiscal policies . This unconventional adjustment is regarded by the market as a major risk signal.

Louis Chua, an Asia equity research analyst at Julius Baer, stated that multiple factors, including uncertainty in the Middle East, high commodity prices, and a surge in fuel subsidy spending, continue to amplify market concerns about the sustainability of Japan's fiscal policy, leading to a persistent pessimistic sentiment in the bond market. Jasper Cole further analyzed that the Japanese government's policy statements this time were vague and lacked sincerity. Compared to statements of a small budget coupled with zero new debt, a more candid approach to increasing debt and spending would likely gain market trust.

However, some institutions remain optimistic. Krishna Bhimavarapu, an economist for Asia Pacific at State Street Global Advisors, said that this supplementary budget is not a large-scale economic stimulus tool, but a targeted policy to support people's livelihoods, specifically to offset the energy price pressure caused by the conflict with Iran. It is in line with Japan's current policy pace and will not excessively disrupt the macroeconomic landscape.

Japan's economic fundamentals have recently shown some resilience, with annualized economic growth reaching 2.1% in the first quarter and GDP increasing by 0.5% quarter-on-quarter. Demand related to semiconductors and artificial intelligence drove a 14.8% year-on-year increase in exports in April. Supported by corporate reforms, mergers and acquisitions, and private equity investment, the Japanese stock market still has room for growth.

Compared to the stock market, the bond and foreign exchange markets continued to weaken. The yen-dollar exchange rate has been hovering around the key level of 160 yen, within a sensitive range for potential currency intervention. Jasper Cole stated that the current bond market performance has fully priced in expectations of rising inflation, interest rate hikes by the Bank of Japan, and an expansion of government bond supply; the risk of further volatility in Japan's financial markets is expected to continue to rise.

Overall, Japan's current relief budget, while seemingly alleviating short-term cost-of-living pressures, has exposed deep-seated problems in its fiscal system. Abnormal policy pronouncements, accumulating debt risks, and rising inflationary pressures are collectively suppressing market confidence.

Looking ahead, Japan will likely exhibit a divergent pattern: a resilient stock market and pressure on its bond and currency markets. Balancing fiscal and monetary policies will become increasingly challenging.

10-year Japanese government bond yield daily chart. Source: EasyTrade.

At 15:17 Beijing time on June 1st, the yield on 10-year Japanese government bonds was 2.679%.

Japanese government bond yields have surged, fiscal and inflation risks are escalating simultaneously, and the yen exchange rate remains under pressure. Although there are some bright spots in Japan's economic fundamentals, the negative signals in the bond and foreign exchange markets indicate that Japan's subsequent macroeconomic control will face enormous challenges.

Japan introduces supplementary budget for people's livelihood, marking a major shift in its policy stance.

Japanese Prime Minister Sanae Takaichi spearheaded the drafting of a new round of supplementary fiscal budget, with the core objective of offsetting inflationary and energy price pressures and providing a safety net for ordinary families.

The supplementary budget amounts to approximately 3 trillion yen, equivalent to US$19 billion , which is in line with previous market expectations. The core background for this policy is the persistently high international commodity and fuel prices due to the Middle East situation, leading to a continuous increase in Japan's fuel subsidy expenditures. This, coupled with the weak yen, has exacerbated domestic pressures on people's livelihoods.

It is noteworthy that this additional fiscal expenditure marks a significant shift in Kaohsiung City's policy stance, which had previously consistently maintained that no additional fiscal spending was needed. Simultaneously, the official statement indicated that the total issuance of government bonds for the 2026 calendar year will remain unchanged from the original budget plan, and that the city intends to cover the increased budget expenditures through government bonds, attempting to stabilize capital market expectations.

The bond market experienced dramatic fluctuations, with a forty-year record being broken once again.

Market skepticism regarding Japan's fiscal policy was quickly reflected in the bond market. On May 20, the yield on Japan's 10-year government bonds surged to 2.812%, closing at 2.772%, a more than 40-year high since 1996. This significant volatility in the bond market fully reflects the market's dual concerns about Japan's fiscal vulnerabilities and rising inflation.

Jesper Koll, a professional director at Monax Group, said that the bond market has a strong ability to identify risks, and that the expansion of fiscal spending will inevitably correspond to an increase in debt. Therefore, the Japanese government's statement of "expanding spending without increasing debt" is untenable .

The core of the market's doubts lies in Sanae Takashi's unusual method of using the calendar year to calculate the scale of bond issuance. Japan has long used March 31st as the end point of the fiscal year and has never used the calendar year to formulate fiscal policies . This unconventional adjustment is regarded by the market as a major risk signal.

Divergent opinions among institutions have led to widespread debate over the effectiveness of the policy.

Louis Chua, an Asia equity research analyst at Julius Baer, stated that multiple factors, including uncertainty in the Middle East, high commodity prices, and a surge in fuel subsidy spending, continue to amplify market concerns about the sustainability of Japan's fiscal policy, leading to a persistent pessimistic sentiment in the bond market. Jasper Cole further analyzed that the Japanese government's policy statements this time were vague and lacked sincerity. Compared to statements of a small budget coupled with zero new debt, a more candid approach to increasing debt and spending would likely gain market trust.

However, some institutions remain optimistic. Krishna Bhimavarapu, an economist for Asia Pacific at State Street Global Advisors, said that this supplementary budget is not a large-scale economic stimulus tool, but a targeted policy to support people's livelihoods, specifically to offset the energy price pressure caused by the conflict with Iran. It is in line with Japan's current policy pace and will not excessively disrupt the macroeconomic landscape.

Economic conditions are diverging, and the stock, bond, and currency markets are moving in opposite directions.

Japan's economic fundamentals have recently shown some resilience, with annualized economic growth reaching 2.1% in the first quarter and GDP increasing by 0.5% quarter-on-quarter. Demand related to semiconductors and artificial intelligence drove a 14.8% year-on-year increase in exports in April. Supported by corporate reforms, mergers and acquisitions, and private equity investment, the Japanese stock market still has room for growth.

Compared to the stock market, the bond and foreign exchange markets continued to weaken. The yen-dollar exchange rate has been hovering around the key level of 160 yen, within a sensitive range for potential currency intervention. Jasper Cole stated that the current bond market performance has fully priced in expectations of rising inflation, interest rate hikes by the Bank of Japan, and an expansion of government bond supply; the risk of further volatility in Japan's financial markets is expected to continue to rise.

Summarize

Overall, Japan's current relief budget, while seemingly alleviating short-term cost-of-living pressures, has exposed deep-seated problems in its fiscal system. Abnormal policy pronouncements, accumulating debt risks, and rising inflationary pressures are collectively suppressing market confidence.

Looking ahead, Japan will likely exhibit a divergent pattern: a resilient stock market and pressure on its bond and currency markets. Balancing fiscal and monetary policies will become increasingly challenging.

10-year Japanese government bond yield daily chart. Source: EasyTrade.

At 15:17 Beijing time on June 1st, the yield on 10-year Japanese government bonds was 2.679%.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.