Non-farm payroll data reinforces tightening expectations; Macquarie predicts the Fed may raise interest rates sooner than expected.

2026-06-08 14:53:57

As the US job market continues to demonstrate resilience, global financial markets' expectations for the Federal Reserve's future policy path are undergoing a significant shift. Following last week's US non-farm payroll data, which far exceeded market expectations, several institutions have begun to reassess future interest rate trends. Macquarie Group's latest view indicates that the institution continues to adhere to its core judgment on the Fed's policy direction: the next policy adjustment is more likely to be a rate hike than a rate cut.

David Doyle, head of economics at Macquarie Group, said that although the market has been focused on the timing of future interest rate cuts for some time, given the current economic and inflationary environment, the Federal Reserve's ultimate action is still likely to be a further increase in interest rates. This view contrasts sharply with some current market expectations.

Previously, the market generally believed that with inflation gradually declining, the Federal Reserve was likely to enter a rate-cutting cycle in the coming years. However, recent strong US economic data has led the market to reconsider this assessment. Data released by the US Bureau of Labor Statistics showed that US non-farm payrolls increased by 172,000 in May, far exceeding market expectations of 85,000. At the same time, the previous figure was also significantly revised upward to 179,000.

Furthermore, the US unemployment rate remained at 4.3% in May, indicating that the labor market remains robust. Continued expansion in the job market means that household spending power remains supported, and as a key engine of US economic growth, the resilience of consumption further reduces the risk of a rapid economic slowdown.

The market believes that with stable economic growth, the Federal Reserve has no urgent reason to quickly shift to an easing policy. More importantly, international energy prices have risen significantly recently. Continued tensions in the Middle East have driven a sharp rebound in international crude oil prices, and the market is beginning to worry that rising energy costs could push up inflation again. If inflation resurfaces, the likelihood of the Federal Reserve maintaining high interest rates or even raising them further will increase significantly.

Market expectations for future policy paths have shifted significantly. Interest rate futures markets show that investors are gradually pricing in future rate hike scenarios. Some trades are already incorporating the possibility of a rate hike in the fourth quarter of 2026, implying that the market believes a rate hike may occur earlier than Macquarie's previous baseline forecast of the first quarter of 2027.

From a policy communication perspective, recent statements by Federal Reserve officials have also shown some changes. For a considerable period, the Fed's discussions primarily revolved around when to initiate easing policies and the pace of future interest rate cuts. However, with continued strong economic data and increased inflation risks from rising energy prices, the market has begun to focus on whether the focus of policy discussions is shifting.

Some analysts believe that in the coming weeks, speeches by Federal Reserve officials may further reduce discussions about interest rate cuts and instead emphasize the necessity of controlling inflation and maintaining policy restraint. While this change in wording does not necessarily mean an immediate rate hike in the short term, it will send a stronger hawkish signal to the market.

From a capital flow perspective, US Treasury yields have been consistently supported recently, and the US dollar index has remained at a relatively high level. Investors' expectations for a prolonged period of high interest rates are strengthening. At the same time, global capital allocation logic is also shifting. Some funds are flowing back into US dollar assets to obtain relatively higher returns, further strengthening the dollar's performance.

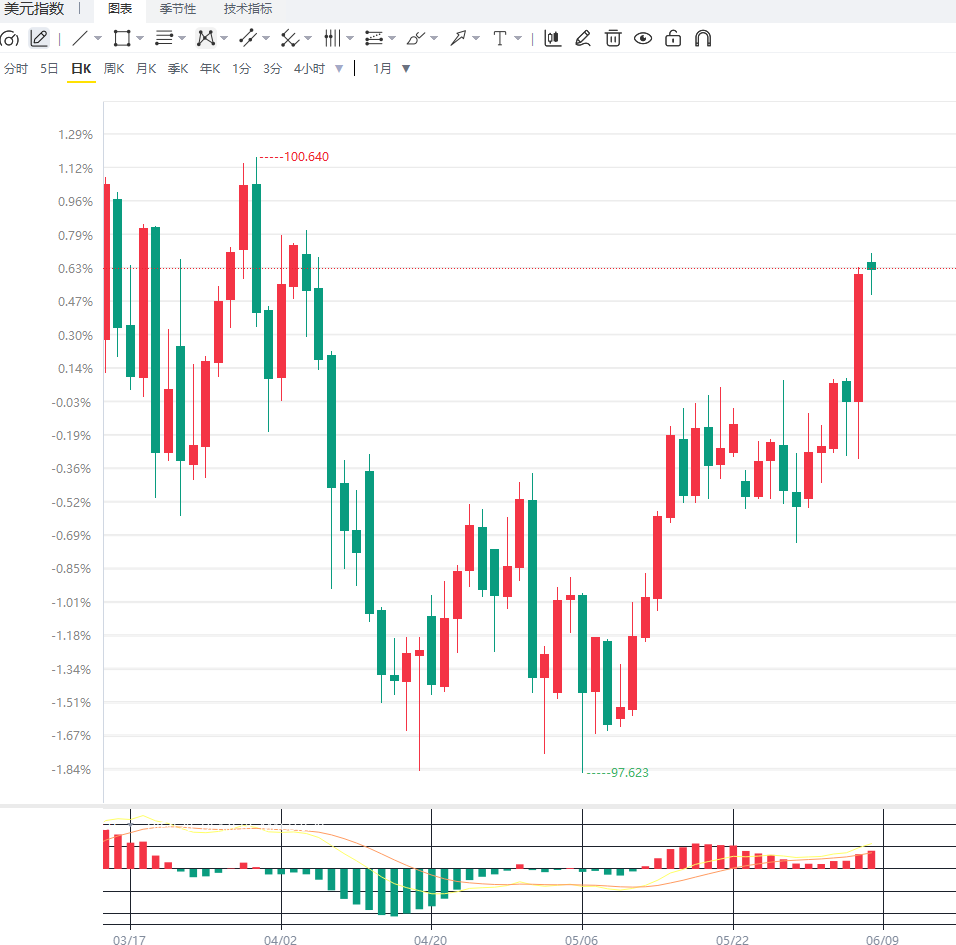

From a technical perspective, the US dollar index continues to trade above the 100 level on the daily chart, maintaining an overall upward trend. The price has stabilized above major moving averages, indicating a continued strong medium- to long-term trend. The MACD indicator remains in a golden cross state, with the red bars continuing to expand, reflecting that upward momentum still dominates the market. The RSI indicator is hovering around 65, approaching overbought territory, but has not yet shown any clear signs of weakening.

From a 4-hour chart perspective, the US dollar index is maintaining an upward channel, with short-term moving averages showing a bullish alignment. If the Federal Reserve releases further hawkish signals, the dollar index is expected to continue challenging previous highs; conversely, if subsequent inflation data shows a significant cooling, market expectations for interest rate hikes may be readjusted, potentially triggering a period of correction.

Editor's Summary : Macquarie Group maintains its core assessment that the Federal Reserve's next move will be a rate hike, reflecting a market reassessment of the resilience of the US economy and inflation risks. Strong employment data and rising energy prices are weakening market expectations for a future rate-cutting cycle and pushing interest rate pricing towards a longer-term higher-interest-rate environment. Going forward, market focus will be on US inflation data, the Fed's meeting minutes, and speeches by officials. If the job market continues to be strong and inflationary pressures resurface, rate hike expectations may be brought forward further, continuing to support the dollar and US Treasury yields. However, if economic growth shows signs of slowing, market bets on prolonged tightening policies may be revised.

David Doyle, head of economics at Macquarie Group, said that although the market has been focused on the timing of future interest rate cuts for some time, given the current economic and inflationary environment, the Federal Reserve's ultimate action is still likely to be a further increase in interest rates. This view contrasts sharply with some current market expectations.

Previously, the market generally believed that with inflation gradually declining, the Federal Reserve was likely to enter a rate-cutting cycle in the coming years. However, recent strong US economic data has led the market to reconsider this assessment. Data released by the US Bureau of Labor Statistics showed that US non-farm payrolls increased by 172,000 in May, far exceeding market expectations of 85,000. At the same time, the previous figure was also significantly revised upward to 179,000.

Furthermore, the US unemployment rate remained at 4.3% in May, indicating that the labor market remains robust. Continued expansion in the job market means that household spending power remains supported, and as a key engine of US economic growth, the resilience of consumption further reduces the risk of a rapid economic slowdown.

The market believes that with stable economic growth, the Federal Reserve has no urgent reason to quickly shift to an easing policy. More importantly, international energy prices have risen significantly recently. Continued tensions in the Middle East have driven a sharp rebound in international crude oil prices, and the market is beginning to worry that rising energy costs could push up inflation again. If inflation resurfaces, the likelihood of the Federal Reserve maintaining high interest rates or even raising them further will increase significantly.

Market expectations for future policy paths have shifted significantly. Interest rate futures markets show that investors are gradually pricing in future rate hike scenarios. Some trades are already incorporating the possibility of a rate hike in the fourth quarter of 2026, implying that the market believes a rate hike may occur earlier than Macquarie's previous baseline forecast of the first quarter of 2027.

From a policy communication perspective, recent statements by Federal Reserve officials have also shown some changes. For a considerable period, the Fed's discussions primarily revolved around when to initiate easing policies and the pace of future interest rate cuts. However, with continued strong economic data and increased inflation risks from rising energy prices, the market has begun to focus on whether the focus of policy discussions is shifting.

Some analysts believe that in the coming weeks, speeches by Federal Reserve officials may further reduce discussions about interest rate cuts and instead emphasize the necessity of controlling inflation and maintaining policy restraint. While this change in wording does not necessarily mean an immediate rate hike in the short term, it will send a stronger hawkish signal to the market.

From a capital flow perspective, US Treasury yields have been consistently supported recently, and the US dollar index has remained at a relatively high level. Investors' expectations for a prolonged period of high interest rates are strengthening. At the same time, global capital allocation logic is also shifting. Some funds are flowing back into US dollar assets to obtain relatively higher returns, further strengthening the dollar's performance.

From a technical perspective, the US dollar index continues to trade above the 100 level on the daily chart, maintaining an overall upward trend. The price has stabilized above major moving averages, indicating a continued strong medium- to long-term trend. The MACD indicator remains in a golden cross state, with the red bars continuing to expand, reflecting that upward momentum still dominates the market. The RSI indicator is hovering around 65, approaching overbought territory, but has not yet shown any clear signs of weakening.

From a 4-hour chart perspective, the US dollar index is maintaining an upward channel, with short-term moving averages showing a bullish alignment. If the Federal Reserve releases further hawkish signals, the dollar index is expected to continue challenging previous highs; conversely, if subsequent inflation data shows a significant cooling, market expectations for interest rate hikes may be readjusted, potentially triggering a period of correction.

Editor's Summary : Macquarie Group maintains its core assessment that the Federal Reserve's next move will be a rate hike, reflecting a market reassessment of the resilience of the US economy and inflation risks. Strong employment data and rising energy prices are weakening market expectations for a future rate-cutting cycle and pushing interest rate pricing towards a longer-term higher-interest-rate environment. Going forward, market focus will be on US inflation data, the Fed's meeting minutes, and speeches by officials. If the job market continues to be strong and inflationary pressures resurface, rate hike expectations may be brought forward further, continuing to support the dollar and US Treasury yields. However, if economic growth shows signs of slowing, market bets on prolonged tightening policies may be revised.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.