Why are US CPI and PCE inflation data diverging?

2026-06-10 19:15:07

In recent months, U.S. Personal Consumption Expenditures (PCE) inflation data has defied historical norms, consistently outpacing the Consumer Price Index (CPI) inflation data. This divergence is particularly pronounced in the core inflation dimension, excluding volatility, completely overturning the long-established market pattern for comparing inflation data. The core reason for this significant divergence lies in the fundamental difference in the weighting of various goods and services in their respective statistical baskets.

The CPI focuses on consumer spending directly paid by individuals, thus categories such as housing and motor vehicles, which are paid for outright by residents, have a very high weight in the CPI basket. The PCE, on the other hand, has a broader scope, covering all goods and services actually consumed by consumers but not necessarily paid for directly by individuals. Its scope includes categories paid for by businesses and the government, providing a more comprehensive reflection of the overall consumer price level. This results in significantly higher weightings for categories such as healthcare, financial services, and software services in the PCE. Recent upgrades in the global technology sector, particularly the sharp rise in software service prices, have become a key driver of PCE inflation. Looking ahead, rental inflation is likely to gradually cool and its rate of increase slow, while software service prices are expected to continue to accelerate. This structural trend of decline and rise will allow the divergence between core CPI and core PCE to continue.

There is no single answer to the question of where US inflation is located; the key factor is the inflation indicator used. Different market participants use vastly different statistical methods and have distinct roles in the market positioning of these two types of inflation data. Ordinary consumers and market participants typically use the Consumer Price Index (CPI) as a benchmark for inflation assessment. This indicator is a core indicator linking inflation to financial contract pricing, wage adjustments, and social security benefits—a core benchmark of market mechanisms and directly related to changes in the cost of living, deeply intertwined with the public's interests. For monetary policy-making institutions like the Federal Reserve, however, their policy anchor is the PCE inflation data. The Federal Reserve bears a dual policy mission, with the long-term core standard for its price stability goal being to keep the PCE inflation rate within a reasonable range of around 2%.

The core differences in statistical methods

The CPI and PCE, two major inflation indicators, differ in several key aspects, including statistical methods, scope, and update mechanisms. This is the underlying reason for the data divergence. The CPI only tracks the average price changes of goods and services directly paid for by urban residents, resulting in a relatively limited sample size. In contrast, the PCE covers all urban and rural residents, not just those directly paid for by individuals, but comprehensively tracks price fluctuations across all consumer goods and services consumed by residents. This core difference directly leads to a significant discrepancy in the category weights of the two indicators.

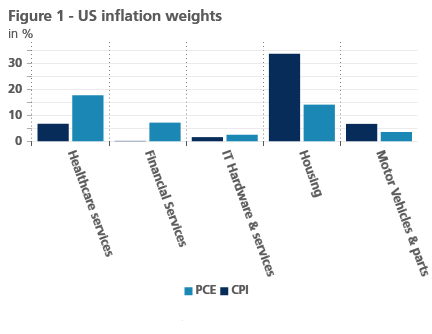

(A comparison of the weights of different consumer categories in the PCE and CPI inflation indices in the United States, with significant differences in key areas such as housing, healthcare services, and motor vehicles)

Healthcare services are mostly funded by employers or government funds, with individuals paying a very small percentage directly. Therefore, this category has a much higher weight in the PCE (Patent Product Index) basket than in the CPI (see Figure 1). Compared to the CPI, which focuses on out-of-pocket healthcare expenditures, the PCE fully incorporates price changes in public healthcare and employer-paid healthcare, better reflecting overall healthcare price trends. The same applies to financial services. The CPI only tracks out-of-pocket financial fees and commissions, while the PCE includes estimated implicit costs of financial intermediary services, covering the value of financial services that individuals actually receive without direct payment. Furthermore, software subscription services like Microsoft 365 are mostly purchased and paid for by companies for their employees, not directly consumed by individuals. Therefore, software services also have a higher weight in the PCE. In contrast, the CPI index is entirely focused on consumer goods directly paid for by individuals, with essential out-of-pocket items such as housing rent and vehicle purchases holding a dominant weight.

The data sources for the two types of indicators are also drastically different, further amplifying statistical bias. CPI data mainly relies on household consumption expenditure surveys and retail price sampling statistics, depending on residents' self-reported consumption data, which has a relatively large subjective error. In contrast, PCE data relies more on business operation surveys and official administrative statistical data, making the data more objective and complete. This also leads to the problem of underweighting some categories in the CPI statistical basket. When reporting their consumption expenditures, most residents tend to underestimate the amount spent on software subscriptions and hidden services, causing the CPI to underreflect price changes in these categories.

Another key difference lies in the weighting adjustment mechanism. The CPI's category weights are adjusted only annually, resulting in a long update cycle and poor flexibility, failing to adapt promptly to dynamic changes in household consumption patterns. In contrast, the PCE employs a dynamic weighting adjustment mechanism, relying on real-time updated household consumption expenditure data, optimizing weight allocations with each data release. Under market forces, when the price of a particular good or service rises rapidly, residents will proactively reduce related consumption expenditures, causing the category's share in their consumption basket to decrease. The PCE's dynamic adjustment model accurately captures this consumption substitution effect, and real-time weight updates ensure that inflation data more closely reflects changes in actual household consumption behavior.

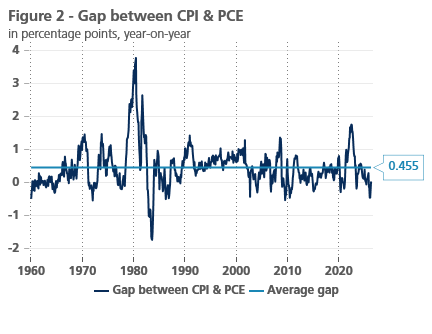

(The deviation between the U.S. Consumer Price Index (CPI) and the Personal Consumption Expenditures Price Index (PCE) at different times)

Influenced by the aforementioned multiple mechanisms, historically, the PCE inflation rate has typically remained consistently lower than the CPI inflation rate (see Figure 2). Over the past few decades, US housing costs have surged, far exceeding the overall inflation rate. Since housing has a very high weighting in the CPI, this has directly raised the long-term inflation center of the CPI, further widening the usual difference between the two data points.

The recent divergence between PCE inflation and CPI

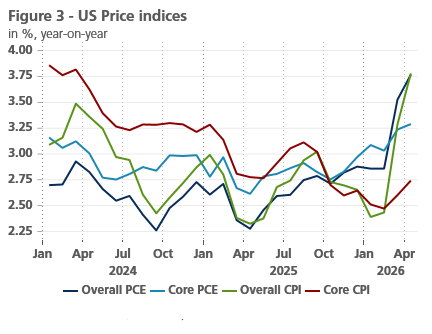

(Annual year-on-year price index trends of US overall PCE, core PCE, overall CPI, and core CPI from 2024 to 2026)

However, the market landscape has recently reversed dramatically, with the long-term low PCE inflation rate surging and surpassing the CPI inflation rate, creating a rare data divergence (see Figure 3). Data shows that in February, the US PCE inflation rate was 0.46 percentage points higher than the CPI inflation rate, a significant divergence. The gap gradually narrowed in the following two months, with both CPI and PCE inflation rates aligning at 3.8% in April. While the overall data appears to have converged, the divergence in core inflation persists, showing no substantial improvement. The core PCE inflation rate remained at 3.3% in April, far exceeding the core CPI inflation rate of 2.7%, indicating a continued clear divergence.

The reason why overall inflation data remained flat for a short period was primarily due to a sharp rise in energy inflation. Energy products have a higher weighting in the CPI basket, and the surge in energy prices directly drove a rapid increase in overall CPI inflation, erasing the overall difference between CPI and PCE. However, this is a short-term structural disturbance and cannot change the underlying divergence in core inflation.

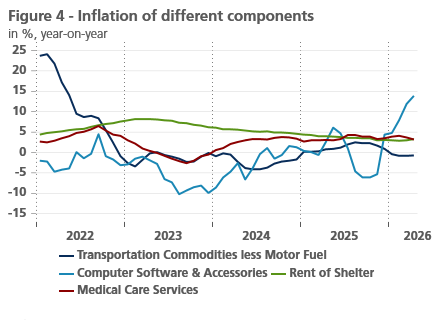

(The changing trends of annual inflation rates for four categories from 2022 to 2026: transportation goods (excluding fuel), computer software and accessories, housing rents, and healthcare services)

The core reason for the persistently high core PCE inflation rate remains the difference in the weighting structure of the two indicators. Recently, prices of several service categories with high weighting in the PCE have accelerated significantly. The explosive growth of the artificial intelligence industry has driven up prices for software services and smart technology services across the entire industry chain, becoming the main driver of core PCE. In contrast, the price increases of motor vehicles and housing rents, which have high weightings in the CPI, have slowed down and declined in recent years (see Figure 4). This structural divergence, with one rising and the other falling, directly causes the divergence between the trends of core PCE and core CPI.

Can the divergence in inflation data continue?

Whether the PCE inflation rate can continue to outpace the CPI in the future largely depends on the evolution of the situation in Iran, with geopolitical conflict being the biggest uncertainty factor in short-term inflation trends. Geopolitical conflict directly impacts the global oil supply structure, exerting a strong disruptive effect on energy prices. Looking at crude oil futures market pricing, the market expects the Iranian conflict to likely ease in the short term. If the situation cools down rapidly, international oil prices will see a decline. Since energy products have a greater impact on the CPI, a drop in oil prices will cause the CPI inflation rate to fall significantly faster than the PCE, further widening the divergence between the two data points. Conversely, if shipping in the Strait of Hormuz is restricted and the conflict continues to escalate, oil prices will rise against the trend, driving a short-term rebound in CPI inflation and slightly narrowing the gap between the two data points.

Excluding core inflation metrics such as energy and food, the divergence between CPI and PCE is likely to continue in the coming months. The artificial intelligence industry remains highly competitive, with no signs of slowing expansion, driving steady price increases in software, information technology, and smart services, providing long-term support for core PCE. Meanwhile, housing services inflation, the largest contributor to CPI, is expected to cool further and its rate of increase will steadily decline, based on current market rental trends. While motor vehicle prices are expected to see a slight rebound, providing some support to CPI, the recovery will be limited and insufficient to erase the difference between the two core inflation categories. Therefore, the structural divergence between CPI and PCE will persist in the long term.

The CPI focuses on consumer spending directly paid by individuals, thus categories such as housing and motor vehicles, which are paid for outright by residents, have a very high weight in the CPI basket. The PCE, on the other hand, has a broader scope, covering all goods and services actually consumed by consumers but not necessarily paid for directly by individuals. Its scope includes categories paid for by businesses and the government, providing a more comprehensive reflection of the overall consumer price level. This results in significantly higher weightings for categories such as healthcare, financial services, and software services in the PCE. Recent upgrades in the global technology sector, particularly the sharp rise in software service prices, have become a key driver of PCE inflation. Looking ahead, rental inflation is likely to gradually cool and its rate of increase slow, while software service prices are expected to continue to accelerate. This structural trend of decline and rise will allow the divergence between core CPI and core PCE to continue.

There is no single answer to the question of where US inflation is located; the key factor is the inflation indicator used. Different market participants use vastly different statistical methods and have distinct roles in the market positioning of these two types of inflation data. Ordinary consumers and market participants typically use the Consumer Price Index (CPI) as a benchmark for inflation assessment. This indicator is a core indicator linking inflation to financial contract pricing, wage adjustments, and social security benefits—a core benchmark of market mechanisms and directly related to changes in the cost of living, deeply intertwined with the public's interests. For monetary policy-making institutions like the Federal Reserve, however, their policy anchor is the PCE inflation data. The Federal Reserve bears a dual policy mission, with the long-term core standard for its price stability goal being to keep the PCE inflation rate within a reasonable range of around 2%.

The core differences in statistical methods

The CPI and PCE, two major inflation indicators, differ in several key aspects, including statistical methods, scope, and update mechanisms. This is the underlying reason for the data divergence. The CPI only tracks the average price changes of goods and services directly paid for by urban residents, resulting in a relatively limited sample size. In contrast, the PCE covers all urban and rural residents, not just those directly paid for by individuals, but comprehensively tracks price fluctuations across all consumer goods and services consumed by residents. This core difference directly leads to a significant discrepancy in the category weights of the two indicators.

(A comparison of the weights of different consumer categories in the PCE and CPI inflation indices in the United States, with significant differences in key areas such as housing, healthcare services, and motor vehicles)

Healthcare services are mostly funded by employers or government funds, with individuals paying a very small percentage directly. Therefore, this category has a much higher weight in the PCE (Patent Product Index) basket than in the CPI (see Figure 1). Compared to the CPI, which focuses on out-of-pocket healthcare expenditures, the PCE fully incorporates price changes in public healthcare and employer-paid healthcare, better reflecting overall healthcare price trends. The same applies to financial services. The CPI only tracks out-of-pocket financial fees and commissions, while the PCE includes estimated implicit costs of financial intermediary services, covering the value of financial services that individuals actually receive without direct payment. Furthermore, software subscription services like Microsoft 365 are mostly purchased and paid for by companies for their employees, not directly consumed by individuals. Therefore, software services also have a higher weight in the PCE. In contrast, the CPI index is entirely focused on consumer goods directly paid for by individuals, with essential out-of-pocket items such as housing rent and vehicle purchases holding a dominant weight.

The data sources for the two types of indicators are also drastically different, further amplifying statistical bias. CPI data mainly relies on household consumption expenditure surveys and retail price sampling statistics, depending on residents' self-reported consumption data, which has a relatively large subjective error. In contrast, PCE data relies more on business operation surveys and official administrative statistical data, making the data more objective and complete. This also leads to the problem of underweighting some categories in the CPI statistical basket. When reporting their consumption expenditures, most residents tend to underestimate the amount spent on software subscriptions and hidden services, causing the CPI to underreflect price changes in these categories.

Another key difference lies in the weighting adjustment mechanism. The CPI's category weights are adjusted only annually, resulting in a long update cycle and poor flexibility, failing to adapt promptly to dynamic changes in household consumption patterns. In contrast, the PCE employs a dynamic weighting adjustment mechanism, relying on real-time updated household consumption expenditure data, optimizing weight allocations with each data release. Under market forces, when the price of a particular good or service rises rapidly, residents will proactively reduce related consumption expenditures, causing the category's share in their consumption basket to decrease. The PCE's dynamic adjustment model accurately captures this consumption substitution effect, and real-time weight updates ensure that inflation data more closely reflects changes in actual household consumption behavior.

(The deviation between the U.S. Consumer Price Index (CPI) and the Personal Consumption Expenditures Price Index (PCE) at different times)

Influenced by the aforementioned multiple mechanisms, historically, the PCE inflation rate has typically remained consistently lower than the CPI inflation rate (see Figure 2). Over the past few decades, US housing costs have surged, far exceeding the overall inflation rate. Since housing has a very high weighting in the CPI, this has directly raised the long-term inflation center of the CPI, further widening the usual difference between the two data points.

The recent divergence between PCE inflation and CPI

(Annual year-on-year price index trends of US overall PCE, core PCE, overall CPI, and core CPI from 2024 to 2026)

However, the market landscape has recently reversed dramatically, with the long-term low PCE inflation rate surging and surpassing the CPI inflation rate, creating a rare data divergence (see Figure 3). Data shows that in February, the US PCE inflation rate was 0.46 percentage points higher than the CPI inflation rate, a significant divergence. The gap gradually narrowed in the following two months, with both CPI and PCE inflation rates aligning at 3.8% in April. While the overall data appears to have converged, the divergence in core inflation persists, showing no substantial improvement. The core PCE inflation rate remained at 3.3% in April, far exceeding the core CPI inflation rate of 2.7%, indicating a continued clear divergence.

The reason why overall inflation data remained flat for a short period was primarily due to a sharp rise in energy inflation. Energy products have a higher weighting in the CPI basket, and the surge in energy prices directly drove a rapid increase in overall CPI inflation, erasing the overall difference between CPI and PCE. However, this is a short-term structural disturbance and cannot change the underlying divergence in core inflation.

(The changing trends of annual inflation rates for four categories from 2022 to 2026: transportation goods (excluding fuel), computer software and accessories, housing rents, and healthcare services)

The core reason for the persistently high core PCE inflation rate remains the difference in the weighting structure of the two indicators. Recently, prices of several service categories with high weighting in the PCE have accelerated significantly. The explosive growth of the artificial intelligence industry has driven up prices for software services and smart technology services across the entire industry chain, becoming the main driver of core PCE. In contrast, the price increases of motor vehicles and housing rents, which have high weightings in the CPI, have slowed down and declined in recent years (see Figure 4). This structural divergence, with one rising and the other falling, directly causes the divergence between the trends of core PCE and core CPI.

Can the divergence in inflation data continue?

Whether the PCE inflation rate can continue to outpace the CPI in the future largely depends on the evolution of the situation in Iran, with geopolitical conflict being the biggest uncertainty factor in short-term inflation trends. Geopolitical conflict directly impacts the global oil supply structure, exerting a strong disruptive effect on energy prices. Looking at crude oil futures market pricing, the market expects the Iranian conflict to likely ease in the short term. If the situation cools down rapidly, international oil prices will see a decline. Since energy products have a greater impact on the CPI, a drop in oil prices will cause the CPI inflation rate to fall significantly faster than the PCE, further widening the divergence between the two data points. Conversely, if shipping in the Strait of Hormuz is restricted and the conflict continues to escalate, oil prices will rise against the trend, driving a short-term rebound in CPI inflation and slightly narrowing the gap between the two data points.

Excluding core inflation metrics such as energy and food, the divergence between CPI and PCE is likely to continue in the coming months. The artificial intelligence industry remains highly competitive, with no signs of slowing expansion, driving steady price increases in software, information technology, and smart services, providing long-term support for core PCE. Meanwhile, housing services inflation, the largest contributor to CPI, is expected to cool further and its rate of increase will steadily decline, based on current market rental trends. While motor vehicle prices are expected to see a slight rebound, providing some support to CPI, the recovery will be limited and insufficient to erase the difference between the two core inflation categories. Therefore, the structural divergence between CPI and PCE will persist in the long term.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.