Federal Reserve tightening expectations weigh on gold; institutions lower short-term targets but remain bullish in the long term.

2026-06-23 09:48:10

The Federal Reserve's current tightening monetary policy stance presents multiple obstacles to the gold market's development. As a result, Bank of America has temporarily lowered its optimistic forecast for short-term gold price increases. The bank's metals research team, led by Michael Widmer, has adjusted its short-term gold price predictions based on market changes. Previously, gold experienced a rare and sustained upward trend, and Bank of America was one of the institutions firmly bullish on gold prices. In January of this year, the bank predicted that the spot gold price could reach $6,000 per ounce this spring.

In their latest precious metals industry report, the research team stated that given the current market environment, it is highly unlikely that gold prices will reach the target of $6,000 per ounce in the short term. The core logic supporting institutions' long-term bullish view on gold remains unchanged: the United States' persistently high fiscal deficit and lack of effective fiscal balance control generate a continuous and substantial demand for financing. These macroeconomic fundamentals continue to provide support for the long-term rise in gold prices.

Widmer's analysis suggests that the core factor currently constraining gold price increases is the ongoing shift in market expectations regarding US monetary policy. At the beginning of the year, global markets generally anticipated that the Federal Reserve would begin a rate-cutting cycle this year. However, the US-Iran conflict triggered global energy supply fluctuations, pushing up inflation across the board. This completely reversed market trading logic, with investors beginning to price in the possibility of a Fed rate hike at the end of the year. Based on data from the CME FedWatch Tool, the market believes there is a greater than 70% probability that the Fed will implement a rate hike in September.

Widmer further explained that the market's pricing in a continued increase in the probability of the Federal Reserve raising interest rates until December 2026 is highly correlated with the downward trend in gold prices. Leaving aside other variables, the market's shift in expectations from interest rate cuts to monetary tightening directly reduces gold's upside potential by nearly half.

The Bank of America team also argued that even if all parties can reach a long-term binding peace agreement, market inflationary pressures will not be alleviated quickly.

The current global geopolitical environment is increasingly fragmented, with supply chain transportation costs and industrial raw material prices rising simultaneously, making the outlook for a decline in inflation less than optimistic. Historically, service price increases have consistently exceeded the Federal Reserve's target, and price stability has only been achieved by relying on lower commodity prices to offset overall inflation. Since the COVID-19 pandemic, core commodity inflation has risen rapidly, and after a slight decline, tariffs have further pushed prices up. Previously, cooling housing-related prices effectively suppressed core inflation, but with housing price trends reversing, this buffering effect will gradually disappear.

While persistently high inflation may force the Federal Reserve Chairman to maintain a hawkish and tight monetary policy, Bank of America points out that several long-term structural positive factors will continue to support the medium- to long-term strength of gold prices.

The US has consistently maintained a high fiscal deficit, hovering around 6% of GDP, while the total amount of US Treasury bonds held by foreign countries has been steadily decreasing. Global central bank gold survey data shows that 74% of surveyed central banks predict that the allocation of US dollar assets in global foreign exchange reserves will shrink to varying degrees over the next five years. Before a substantial change in macroeconomic fundamentals, short-term negative factors cannot alter the long-term upward potential of gold.

Widmer's team is also optimistic about the new gold allocation demand from ordinary investors . For gold prices to resume their upward trend, the market needs to gradually digest interest rate hike expectations, at which point investment buying will further push up gold prices. Currently, the investment volume of physical gold and gold financial derivatives accounts for approximately 5.5% of the total global stock and bond market size. The mainstream asset allocation strategy is shifting from 60% stocks and 40% bonds to 60% stocks, 20% bonds, and 20% alternative assets, indicating ample room for new gold allocations.

Overall, short-term interest rate hike expectations continue to suppress gold prices, with Bank of America significantly lowering its short-term gold price increase forecast and postponing its target of $6,000. However, the long-term logic of global geopolitics, US fiscal imbalances, declining dollar reserve share, and diversified household asset allocation remains unchanged, and gold still has a medium- to long-term upward foundation. The subsequent market trend will still depend on the pace of changes in the Fed's monetary policy expectations.

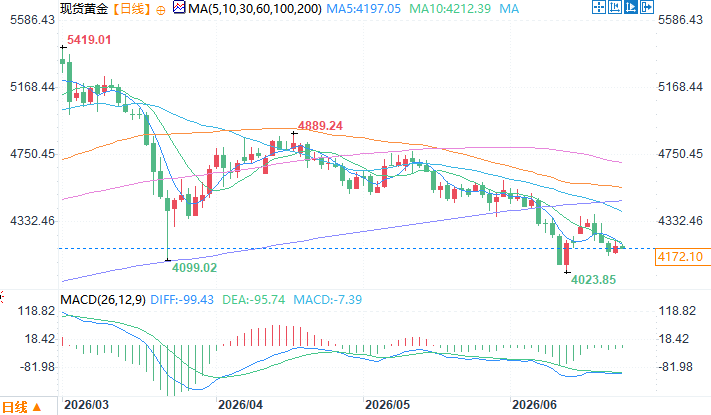

Spot gold daily chart source: EasyForex

At 9:47 AM Beijing time on June 23, spot gold was trading at $4154.10 per ounce.

A shift in Federal Reserve policy expectations has hampered gold's short-term upward movement.

In their latest precious metals industry report, the research team stated that given the current market environment, it is highly unlikely that gold prices will reach the target of $6,000 per ounce in the short term. The core logic supporting institutions' long-term bullish view on gold remains unchanged: the United States' persistently high fiscal deficit and lack of effective fiscal balance control generate a continuous and substantial demand for financing. These macroeconomic fundamentals continue to provide support for the long-term rise in gold prices.

Widmer's analysis suggests that the core factor currently constraining gold price increases is the ongoing shift in market expectations regarding US monetary policy. At the beginning of the year, global markets generally anticipated that the Federal Reserve would begin a rate-cutting cycle this year. However, the US-Iran conflict triggered global energy supply fluctuations, pushing up inflation across the board. This completely reversed market trading logic, with investors beginning to price in the possibility of a Fed rate hike at the end of the year. Based on data from the CME FedWatch Tool, the market believes there is a greater than 70% probability that the Fed will implement a rate hike in September.

Widmer further explained that the market's pricing in a continued increase in the probability of the Federal Reserve raising interest rates until December 2026 is highly correlated with the downward trend in gold prices. Leaving aside other variables, the market's shift in expectations from interest rate cuts to monetary tightening directly reduces gold's upside potential by nearly half.

Multiple factors are locking in inflation, and expectations of interest rate hikes are unlikely to subside quickly.

The Bank of America team also argued that even if all parties can reach a long-term binding peace agreement, market inflationary pressures will not be alleviated quickly.

The current global geopolitical environment is increasingly fragmented, with supply chain transportation costs and industrial raw material prices rising simultaneously, making the outlook for a decline in inflation less than optimistic. Historically, service price increases have consistently exceeded the Federal Reserve's target, and price stability has only been achieved by relying on lower commodity prices to offset overall inflation. Since the COVID-19 pandemic, core commodity inflation has risen rapidly, and after a slight decline, tariffs have further pushed prices up. Previously, cooling housing-related prices effectively suppressed core inflation, but with housing price trends reversing, this buffering effect will gradually disappear.

Long-term fundamentals support gold prices, and there is potential for increased demand for asset allocation.

While persistently high inflation may force the Federal Reserve Chairman to maintain a hawkish and tight monetary policy, Bank of America points out that several long-term structural positive factors will continue to support the medium- to long-term strength of gold prices.

The US has consistently maintained a high fiscal deficit, hovering around 6% of GDP, while the total amount of US Treasury bonds held by foreign countries has been steadily decreasing. Global central bank gold survey data shows that 74% of surveyed central banks predict that the allocation of US dollar assets in global foreign exchange reserves will shrink to varying degrees over the next five years. Before a substantial change in macroeconomic fundamentals, short-term negative factors cannot alter the long-term upward potential of gold.

Widmer's team is also optimistic about the new gold allocation demand from ordinary investors . For gold prices to resume their upward trend, the market needs to gradually digest interest rate hike expectations, at which point investment buying will further push up gold prices. Currently, the investment volume of physical gold and gold financial derivatives accounts for approximately 5.5% of the total global stock and bond market size. The mainstream asset allocation strategy is shifting from 60% stocks and 40% bonds to 60% stocks, 20% bonds, and 20% alternative assets, indicating ample room for new gold allocations.

Summarize

Overall, short-term interest rate hike expectations continue to suppress gold prices, with Bank of America significantly lowering its short-term gold price increase forecast and postponing its target of $6,000. However, the long-term logic of global geopolitics, US fiscal imbalances, declining dollar reserve share, and diversified household asset allocation remains unchanged, and gold still has a medium- to long-term upward foundation. The subsequent market trend will still depend on the pace of changes in the Fed's monetary policy expectations.

Spot gold daily chart source: EasyForex

At 9:47 AM Beijing time on June 23, spot gold was trading at $4154.10 per ounce.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.