The US-Iran ceasefire triggered a plunge in oil prices due to supply shortages, but it also carries the risk of a reversal.

2026-06-29 13:26:39

With the US and Iran reaching a 60-day ceasefire agreement, the international crude oil market has undergone dramatic changes, and oil prices have begun a rapid decline.

The market generally anticipates that the resumption of shipping in the Strait of Hormuz will release a massive supply of crude oil, causing stranded tankers to sail out of the Persian Gulf and directly suppressing oil prices. However, this round of easing is fraught with hidden risks: sudden attacks on merchant ships, insufficient shipping capacity, global restocking demand, and geopolitical uncertainties all lay the groundwork for a subsequent rebound in oil prices, and there is room for correction in the market's overly pessimistic trading sentiment.

Following the US-Iran ceasefire agreement, the efficiency of Persian Gulf oil transportation has significantly improved, leading to a rapid increase in market expectations for ample supply and a substantial discount in spot crude oil prices. Last week's market data showed that Angolan crude oil was trading at a discount of $10 per barrel to Brent crude, a discount rarely seen in nearly a decade. Simultaneously, weakening demand in Asian markets prompted some refineries in major Asian countries to begin selling off their crude oil cargoes, further exacerbating the short-term oversupply situation.

Daan Struyven, co-head of global commodities at Goldman Sachs, said: "Currently, demand for Middle Eastern crude oil in the Asian market is weak, resulting in a structure where forward oil prices are higher than spot prices, and the recovery speed and overall progress of shipping in the Persian Gulf have exceeded market expectations."

Multiple expectations of easing have combined to drive oil prices down, rapidly rewriting the previous high-price situation supported by geopolitical tensions.

The speed of this round of oil price decline far exceeded industry expectations, mainly because the market over-anticipated the positive impact of the resumption of air traffic.

JPMorgan's commodities analysis team stated that the core logic behind this round of oil price rebalancing is the combined effect of declining market demand and the release of global inventories, which is completely different from the supply contraction logic previously predicted by institutions. Most market participants simply focused on short-term crude oil supply, ignoring the structural risks behind the market trend.

ING's commodities research team advises the market to view this round of shipping recovery rationally. The team stated that the current increase in outbound shipping through the Strait of Hormuz is mainly due to the departure of existing tankers that were previously stranded due to geopolitical issues. The number of newly added tankers entering the Persian Gulf to conduct transportation business is extremely limited, and the long-term shipping capacity supply has not improved substantially.

Executives at Phillips 66, an industry player, estimate that approximately 90 to 100 million barrels of crude oil currently stranded will be shipped out of port, but issues such as tanker entry insurance and shipping safety remain unresolved, casting doubt on the ability to continue shipping.

Bart Melek, global head of commodities strategy at TD Securities, said the market is overly optimistic about the pace of crude oil supply and inventory recovery, and the short-term oversupply situation is unlikely to last.

Just as the market was betting on ample crude oil supply, Iran's attack on a civilian merchant ship in the Strait of Hormuz reignited geopolitical risk aversion and disrupted stable navigation expectations. As a result, the pace of decline in the crude oil market slowed significantly, and geopolitical risk premiums returned to the market.

IG analyst Tony Sycamore believes that the market will focus on monitoring the status of oil tanker traffic in the Strait of Hormuz. This sudden conflict is likely to constrain the pace of oil-producing countries' production and shipment, providing key support for oil prices.

During the previous Strait of Hormuz crisis, countries around the world mainly relied on releasing crude oil reserves to stabilize the market, while major Asian countries relied on their huge strategic reserves to reduce import purchases, effectively preventing a sharp rise in oil prices.

With the resumption of shipping, refineries in major Asian countries will restart regular crude oil purchases after completing the sale of existing cargoes. The need for replenishment in the United States is even more urgent. As of the week ending June 19, the U.S. Strategic Petroleum Reserve stood at only 331.2 million barrels, a 40-year low, and the industry has fixed minimum operating inventory limits, leaving very limited available reserve resources.

In summary, the increased supply resulting from the concentrated departure of stranded oil tankers in the short term has continued to suppress crude oil prices, leading to the recent sharp drop in oil prices. However, after the existing stockpiles are cleared, multiple positive factors, such as insufficient new shipping capacity, recurring geopolitical conflicts, and global restocking driven by essential needs, will gradually emerge.

The current excessively pessimistic sentiment in the market needs to be corrected, and the downside potential for oil prices is limited. The market will subsequently enter a period of consolidation and correction as risks and positive factors interact.

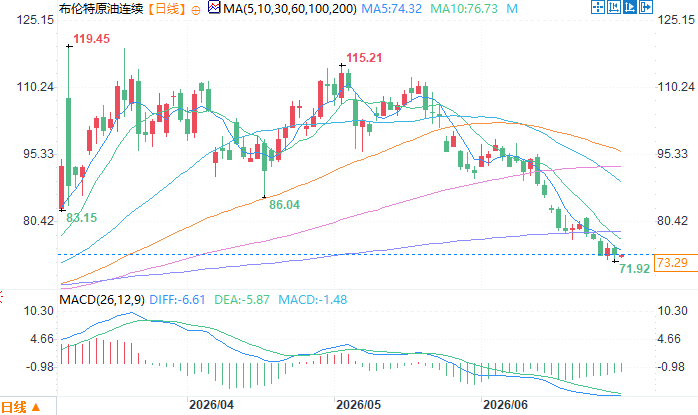

Brent crude oil daily chart source: EasyForex

At 11:10 AM Beijing time on June 29, Brent crude oil futures were trading at $73.20 per barrel.

The market generally anticipates that the resumption of shipping in the Strait of Hormuz will release a massive supply of crude oil, causing stranded tankers to sail out of the Persian Gulf and directly suppressing oil prices. However, this round of easing is fraught with hidden risks: sudden attacks on merchant ships, insufficient shipping capacity, global restocking demand, and geopolitical uncertainties all lay the groundwork for a subsequent rebound in oil prices, and there is room for correction in the market's overly pessimistic trading sentiment.

The ceasefire triggered supply expectations, leading to a significant discount in spot crude oil prices.

Following the US-Iran ceasefire agreement, the efficiency of Persian Gulf oil transportation has significantly improved, leading to a rapid increase in market expectations for ample supply and a substantial discount in spot crude oil prices. Last week's market data showed that Angolan crude oil was trading at a discount of $10 per barrel to Brent crude, a discount rarely seen in nearly a decade. Simultaneously, weakening demand in Asian markets prompted some refineries in major Asian countries to begin selling off their crude oil cargoes, further exacerbating the short-term oversupply situation.

Daan Struyven, co-head of global commodities at Goldman Sachs, said: "Currently, demand for Middle Eastern crude oil in the Asian market is weak, resulting in a structure where forward oil prices are higher than spot prices, and the recovery speed and overall progress of shipping in the Persian Gulf have exceeded market expectations."

Multiple expectations of easing have combined to drive oil prices down, rapidly rewriting the previous high-price situation supported by geopolitical tensions.

Market optimism is rampant, but institutions warn of the risk of a false supply situation.

The speed of this round of oil price decline far exceeded industry expectations, mainly because the market over-anticipated the positive impact of the resumption of air traffic.

JPMorgan's commodities analysis team stated that the core logic behind this round of oil price rebalancing is the combined effect of declining market demand and the release of global inventories, which is completely different from the supply contraction logic previously predicted by institutions. Most market participants simply focused on short-term crude oil supply, ignoring the structural risks behind the market trend.

ING's commodities research team advises the market to view this round of shipping recovery rationally. The team stated that the current increase in outbound shipping through the Strait of Hormuz is mainly due to the departure of existing tankers that were previously stranded due to geopolitical issues. The number of newly added tankers entering the Persian Gulf to conduct transportation business is extremely limited, and the long-term shipping capacity supply has not improved substantially.

Executives at Phillips 66, an industry player, estimate that approximately 90 to 100 million barrels of crude oil currently stranded will be shipped out of port, but issues such as tanker entry insurance and shipping safety remain unresolved, casting doubt on the ability to continue shipping.

Bart Melek, global head of commodities strategy at TD Securities, said the market is overly optimistic about the pace of crude oil supply and inventory recovery, and the short-term oversupply situation is unlikely to last.

Geopolitical risks have resurfaced, and the decline in oil prices has gradually slowed.

Just as the market was betting on ample crude oil supply, Iran's attack on a civilian merchant ship in the Strait of Hormuz reignited geopolitical risk aversion and disrupted stable navigation expectations. As a result, the pace of decline in the crude oil market slowed significantly, and geopolitical risk premiums returned to the market.

IG analyst Tony Sycamore believes that the market will focus on monitoring the status of oil tanker traffic in the Strait of Hormuz. This sudden conflict is likely to constrain the pace of oil-producing countries' production and shipment, providing key support for oil prices.

Global restocking demand provides a floor, limiting the downside potential for oil prices.

During the previous Strait of Hormuz crisis, countries around the world mainly relied on releasing crude oil reserves to stabilize the market, while major Asian countries relied on their huge strategic reserves to reduce import purchases, effectively preventing a sharp rise in oil prices.

With the resumption of shipping, refineries in major Asian countries will restart regular crude oil purchases after completing the sale of existing cargoes. The need for replenishment in the United States is even more urgent. As of the week ending June 19, the U.S. Strategic Petroleum Reserve stood at only 331.2 million barrels, a 40-year low, and the industry has fixed minimum operating inventory limits, leaving very limited available reserve resources.

Overall Market Summary

In summary, the increased supply resulting from the concentrated departure of stranded oil tankers in the short term has continued to suppress crude oil prices, leading to the recent sharp drop in oil prices. However, after the existing stockpiles are cleared, multiple positive factors, such as insufficient new shipping capacity, recurring geopolitical conflicts, and global restocking driven by essential needs, will gradually emerge.

The current excessively pessimistic sentiment in the market needs to be corrected, and the downside potential for oil prices is limited. The market will subsequently enter a period of consolidation and correction as risks and positive factors interact.

Brent crude oil daily chart source: EasyForex

At 11:10 AM Beijing time on June 29, Brent crude oil futures were trading at $73.20 per barrel.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.