Non-farm payrolls preview! Unemployment rate hits critical 4.4% – will the US economy plunge off a cliff?

2026-02-10 16:01:18

Last fall, a volatile and weak job market was a core concern for the Federal Reserve. To hedge against the risks of rising unemployment and a sharp slowdown in hiring, the Fed cut benchmark interest rates three times by the end of 2025 to stabilize the job market.

Today, market attention has shifted back to the persistently high inflation problem.

The U.S. Bureau of Labor Statistics (BLS) releases the Annual Benchmark Revision along with its January Employment Situation Report (usually released in February).

In September 2025, BLS had already released a "preliminary estimate," which showed a downward revision of 911,000 people. The final figure released this Wednesday is widely expected to remain between 800,000 and 900,000, but some institutions believe the downward revision may exceed 1 million.

The US experienced a contraction in job creation during the summer of 2025, followed by a period of recovery in hiring in the last two months of the year. After hitting a four-year high, the unemployment rate fell slightly to 4.4% in December.

Analysts predict that the U.S. will add 55,000 jobs in January, with the unemployment rate remaining at 4.4%. The current unemployment rate is a key indicator, and the economy only needs to add about 50,000 jobs to maintain the low unemployment rate. As long as employment remains resilient, the U.S. economy can avoid the risk of recession.

However, there is a clear divergence in the market regarding the employment outlook: the Federal Reserve believes that the job market has stabilized, but some Wall Street institutions point out that job openings have fallen sharply and the employment fundamentals are still deteriorating.

Based on confidence in the job market, the Federal Reserve paused interest rate cuts at the end of January by a 10-2 vote, marking the first time in nearly four meetings that it held rates steady. Most officials believed that inflation had not met targets and that there were no plans to cut rates in the short term.

Regarding inflation, January data is expected to show a slight slowdown, with institutions predicting that both overall and core CPI will rise by 0.3% month-on-month and fall back to 2.5% year-on-year.

The prevailing view is that the impact of tariffs will gradually subside by 2026, and the slowdown in the growth of housing and labor costs will push inflation towards the 2% target.

However, concerns about inflation remain. Some Federal Reserve officials have stated that inflation is stubbornly above the target, coupled with the "January effect" of companies raising prices in January and the passing on of tariff costs to consumers, there is a possibility that inflation could rise more than expected.

Recent important data includes the ADP January private sector employment data, which showed an increase of only 22,000 jobs (far below the market expectation of 48,000). The December data was also revised down from 41,000 to 37,000, which briefly triggered market concerns about the labor market. In addition, the Challenger report showed that the US job market in January was in a severe situation of "surge in layoffs and a hiring freeze".

Local employers announced 108,435 layoffs that month, a surge of 118% year-on-year and 205% month-on-month, setting a record high for the same period since January 2009, and also the highest monthly peak since October 2025.

Meanwhile, the University of Michigan's consumer confidence index shows that inflation expectations are slowing. These data create a scenario of weak employment but slowing inflation, which is conducive to raising expectations of interest rate cuts.

Taking the US dollar index, one of the top three most influential currencies in the market, as an example, the delayed non-farm payroll data will be released at the same time as the revision of the non-farm payroll data for the whole of 2025. However, the BLS had already disclosed information last September that the data might be revised down by 900,000. If the revision exceeds expectations, it will lead to a weak dollar and strong gold. At the same time, if the revision meets expectations and causes a short-term downward shock to the dollar, it will be a buying opportunity for the dollar, because the Fed still chose not to cut interest rates in January when it knew the data, which represents an affirmation of the resilience of the labor market.

The most important point to observe in this non-farm payroll data is the unemployment rate. According to the SAM rule, when the three-month moving average of the US unemployment rate is 0.5 percentage points higher than the lowest point in the past 12 months, the economy officially enters a recession. The 0.5 percentage point higher is 4.4%. Economists also believe that the inflection point of the Beveridge curve is also at 4.4%. Exceeding the inflection point means that the labor market is not cooling but in recession. From an empirical perspective, in July 2024, the unemployment rate once touched 4.3%, which triggered Black Monday in global markets.

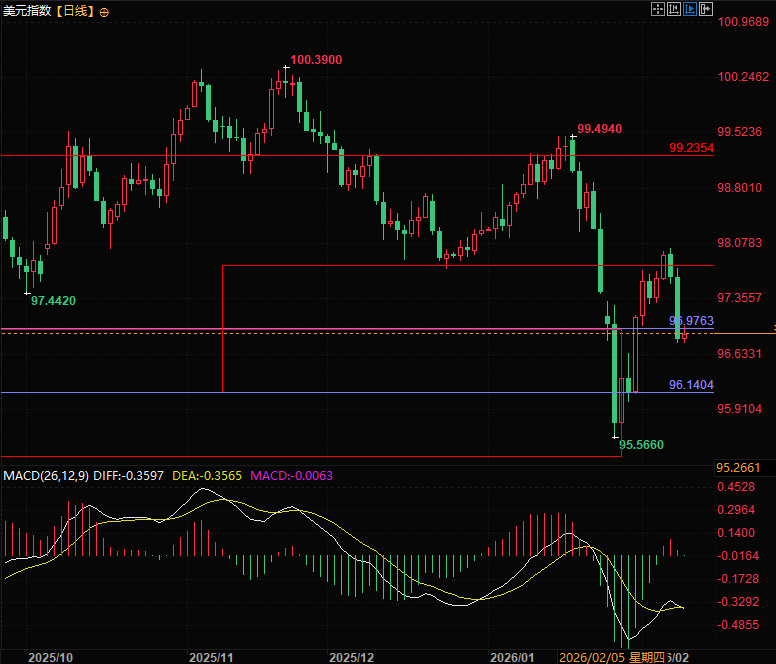

From a technical perspective, the US dollar index fell on Monday, most likely in response to the downward revision of non-farm payroll data and weak labor data . If the non-farm payroll data is significantly lower than expected, the dollar index may fall further, with support around 96.15. However, if the non-farm payroll data meets or slightly falls short of expectations, the dollar index will likely reach a low point for the day.

(US Dollar Index Daily Chart, Source: FX678)

At 15:57 Beijing time, the US dollar index is currently at 96.91.

Today, market attention has shifted back to the persistently high inflation problem.

The U.S. Bureau of Labor Statistics (BLS) releases the Annual Benchmark Revision along with its January Employment Situation Report (usually released in February).

In September 2025, BLS had already released a "preliminary estimate," which showed a downward revision of 911,000 people. The final figure released this Wednesday is widely expected to remain between 800,000 and 900,000, but some institutions believe the downward revision may exceed 1 million.

Job Market: Stabilization and Divergence Coexist, Supporting a Pause in Interest Rate Cuts

The US experienced a contraction in job creation during the summer of 2025, followed by a period of recovery in hiring in the last two months of the year. After hitting a four-year high, the unemployment rate fell slightly to 4.4% in December.

Analysts predict that the U.S. will add 55,000 jobs in January, with the unemployment rate remaining at 4.4%. The current unemployment rate is a key indicator, and the economy only needs to add about 50,000 jobs to maintain the low unemployment rate. As long as employment remains resilient, the U.S. economy can avoid the risk of recession.

However, there is a clear divergence in the market regarding the employment outlook: the Federal Reserve believes that the job market has stabilized, but some Wall Street institutions point out that job openings have fallen sharply and the employment fundamentals are still deteriorating.

Based on confidence in the job market, the Federal Reserve paused interest rate cuts at the end of January by a 10-2 vote, marking the first time in nearly four meetings that it held rates steady. Most officials believed that inflation had not met targets and that there were no plans to cut rates in the short term.

Inflation Trends: Short-term slowdown but upward risks remain.

Regarding inflation, January data is expected to show a slight slowdown, with institutions predicting that both overall and core CPI will rise by 0.3% month-on-month and fall back to 2.5% year-on-year.

The prevailing view is that the impact of tariffs will gradually subside by 2026, and the slowdown in the growth of housing and labor costs will push inflation towards the 2% target.

However, concerns about inflation remain. Some Federal Reserve officials have stated that inflation is stubbornly above the target, coupled with the "January effect" of companies raising prices in January and the passing on of tariff costs to consumers, there is a possibility that inflation could rise more than expected.

Policy Impact: Data Results Determine the Pace of Interest Rate Cuts and Market Trends

Recent important data includes the ADP January private sector employment data, which showed an increase of only 22,000 jobs (far below the market expectation of 48,000). The December data was also revised down from 41,000 to 37,000, which briefly triggered market concerns about the labor market. In addition, the Challenger report showed that the US job market in January was in a severe situation of "surge in layoffs and a hiring freeze".

Local employers announced 108,435 layoffs that month, a surge of 118% year-on-year and 205% month-on-month, setting a record high for the same period since January 2009, and also the highest monthly peak since October 2025.

Meanwhile, the University of Michigan's consumer confidence index shows that inflation expectations are slowing. These data create a scenario of weak employment but slowing inflation, which is conducive to raising expectations of interest rate cuts.

Summary and Technical Analysis:

Taking the US dollar index, one of the top three most influential currencies in the market, as an example, the delayed non-farm payroll data will be released at the same time as the revision of the non-farm payroll data for the whole of 2025. However, the BLS had already disclosed information last September that the data might be revised down by 900,000. If the revision exceeds expectations, it will lead to a weak dollar and strong gold. At the same time, if the revision meets expectations and causes a short-term downward shock to the dollar, it will be a buying opportunity for the dollar, because the Fed still chose not to cut interest rates in January when it knew the data, which represents an affirmation of the resilience of the labor market.

The most important point to observe in this non-farm payroll data is the unemployment rate. According to the SAM rule, when the three-month moving average of the US unemployment rate is 0.5 percentage points higher than the lowest point in the past 12 months, the economy officially enters a recession. The 0.5 percentage point higher is 4.4%. Economists also believe that the inflection point of the Beveridge curve is also at 4.4%. Exceeding the inflection point means that the labor market is not cooling but in recession. From an empirical perspective, in July 2024, the unemployment rate once touched 4.3%, which triggered Black Monday in global markets.

From a technical perspective, the US dollar index fell on Monday, most likely in response to the downward revision of non-farm payroll data and weak labor data . If the non-farm payroll data is significantly lower than expected, the dollar index may fall further, with support around 96.15. However, if the non-farm payroll data meets or slightly falls short of expectations, the dollar index will likely reach a low point for the day.

(US Dollar Index Daily Chart, Source: FX678)

At 15:57 Beijing time, the US dollar index is currently at 96.91.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.